@taobanker I hear ya. Haven't spent too much time, what's the bear thesis? Any pieces very prone to AI disruption?

English

Roaming Capital

63 posts

@RoamingCapital

Global value investor with drifting style and not afraid of odd geographies | Roaming Capital | Seeking asymmetry across borders | Tech/financial bias

Wild regulatory standoff for $CERT.V in Portugal! The Lagoa Salgada EIA saga just exploded: 1.Cerrado declared the project APPROVED by default (“Tacit Approval”) as the agency (APA) missed its legal deadline. 2.APA panicked & issued a REJECTION… after the deadline had passed

Even without taking a long-term view, the PSU market is going to grow massively starting next year. What’s really unfortunate is that most major PSU makers are Taiwanese companies. For me, investing in Taiwanese stocks is a bit tricky.

New position $NDO at 72.5c avg From the same guy who built and sold Think Childcare. The business model here is very strong, only buying centres from their incubator at 80%+ occupancy Huge growth pipeline - trading like a shitco - once a couple funds want it will be 15x EPS

Pretty incredible outcome for $TNK $TNK.AX holders Caught an initial bid of $1.35 in Nov 2020 Today seal a deal for $3.41 including franking credits 🔥🔥

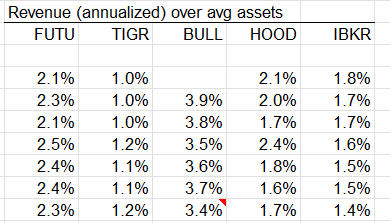

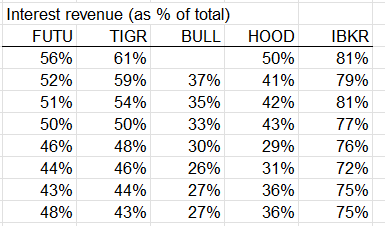

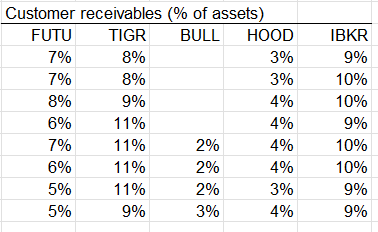

Checking out brokers, HOOD was 25% the revenue size of IBKR revenue two years ago, now almost 50%. Interesting thing is on non-interest revenue they have already surpased IBKR. And the last two quarters HOOD started to grow margin and securities lending aggressively, so the gap there will close too. All this probably well reflected on realtive valuations. Still a vastly different customer base for equities, but may now coming head to head on predictions, crypto etc. On the Asia side, FUTU remains 4-5x the size of TIGR and still growing at similar rates, maintaining share. 30% of FUTU customer trading volume is now in HK (from 20%) they prob have the most country-agnostic customers, which will go where things are moving (i dont have stats for HOOD or IBKR but I assume 90% is US trading). I'm long FUTU at 20x LTM (on record earnings, maybe 25x with a couple of avg trading quarters). Asia casino junket for the financialization of everything gambling gallore.

Speculative long in $ACMR today. Stop at 33, target somewhere in the 40s. Supplier of semiconductor cleaning materials, primarily to China. Name got slammed earlier this year on export controls, etc, now that China chips are hot I think its worth a look. They own most of 688082 CH in China, ACM Research Shanghai. Long 3,600 at $33, stop around there, think it could trade into the upper 40s if the China chips trade keeps going.

I wrote up the defense/aerospace systems integrator $ISSC on Substack. After a series of unusual and quite large financings, I thought the time was now: martinbradstreet.substack.com/p/innovative-s…. ISSC has a solid and stable business taking on work other companies don't want, but has grown its tentacles into seamingly every major player in the defense and aerospaces businesses. Exciting things are ahead. Disclosure: i am long. The substack is not a suggestion to buy $ISSC shares - you could lose all your money. Investing is risky. etc.