Sabitlenmiş Tweet

This is the portfolio I am taking into 2026.

Mega thread with a short pitch for every stock in my current portfolio 🧵

1. $247A.T AI Robotics

➢ Japanese company that uses a proprietary AI engine called "Sell" to develop and scale its own D2C consumer brands, mainly in the areas beauty and beauty devices. Thanks to "Sell" product development, advertising campaigns, and CRM processes are largely automated, while production is fully outsourced. This makes the company extremely asset-light and efficient. Annualized revenue per employee stands at 8.4m USD.

The company’s goal is a 100% revenue and earnings CAGR through 2029, driven by organic growth of existing brands (including international expansion) and the launch of one new brand per year (e.g. in the areas functional food, apparel or jewelry).

Personally, I consider a 50% earnings CAGR through 2029 to be realistic.

💵 FY 2026 (01.04.25 – 31.03.26): 28x PE

💵 FY 2027 (01.04.26 – 31.03.27): 14–18x PE

2. $SLYG.DE Shelly Group

➢ Bulgarian smart-home device company. Competitive advantages include compatibility with nearly all major connectivity standards, high programmability, a broad product portfolio and a European cloud. Future growth drivers could be Shelly X (a proprietary chip for other OEMs to smart-enable their devices) and growing cloud revenues. A stock I’ve held for a long time. Management execution has been first-class for many years.

💵 2026: 25x PE

💵 2027: 19x PE

Not cheap, but still enough for about 20% return CAGR from here, in my view.

3. $HROW Harrow

➢ Ophthalmology company that leverages a unique distribution network to ophthalmologists and surgical centers to acquire high-margin eye drugs neglected by Big Pharma at low prices and scale them rapidly.

Future growth drivers include further market share gains for blockbuster drug Vevye (dry eye treatment), scaling acquired biosimilars, and the innovative sedative MELT-300, which could open up a large market beyond ophthalmology starting in 2028.

Company target: 250m USD Q4/27 revenue at 30–40% operating margin.

💵 2026: 32x PE, 14x EV/EBITDA

💵 2027: 20x PE, 10x EV/EBITDA

Attractive IMO for a company with clear operating leverage and at least 30% topline growth through 2029.

4. $NURS.V Hydreight Technologies

➢ The “Uber for nurses” and “Shopify for telehealth companies” from Canada, riding trends like GLP-1, TRT, and peptides. With scaling of the VSDHOne segment (the Shopify equivalent), hockey-stick growth is expected in 2026.

Current analyst consensus sees ~196% growth next year to 105m CAD revenue. Given the recently reported placed order numbers for VSDHOne, this looks far too low to me.

There are risks, especially potential pricing pressure for GLP-1 drugs and uncertainty around achievable AOV levels, but even considering those, the upside is enormous in my view. My personal top pick for 2026.

💵 2026: 14x PE (as mentioned, estimates appear far too conservative)

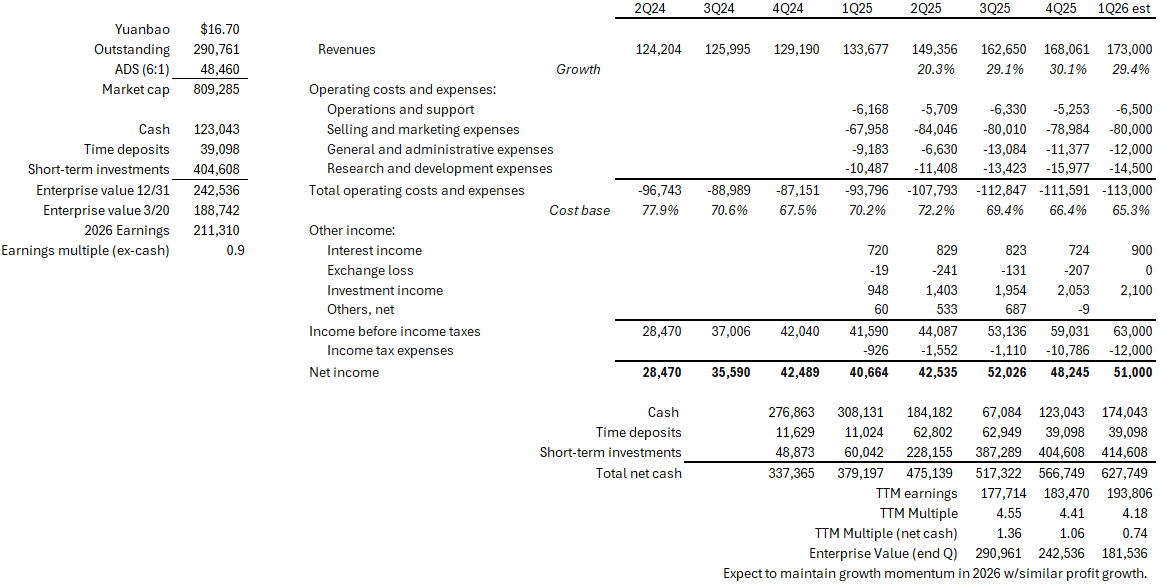

5. $YB Yuanbao

➢ Chinese online insurance broker for medical and critical illness insurance, led by an ex-NetEase C-suite team and powered by a strong AI engine enabling high automation in customer targeting, conversion, and after-sales services. Excellent financials with very high margins (96% GM, 30% OM), high capital returns (~40% ROCE), and a pristine balance sheet (debt-free, 88% of total assets in cash & equivalents).

Market cap is ~56% covered by balance-sheet cash. I believe ~20% topline growth is achievable over the next two years. If the company finally initiates dividends or buybacks, I expect a re-rating to around 10x PE (level of closest peer Waterdrop $WDH).

💵 2025: 5x PE and 1.8x EV/FCF – absurdly cheap, in my opinion.

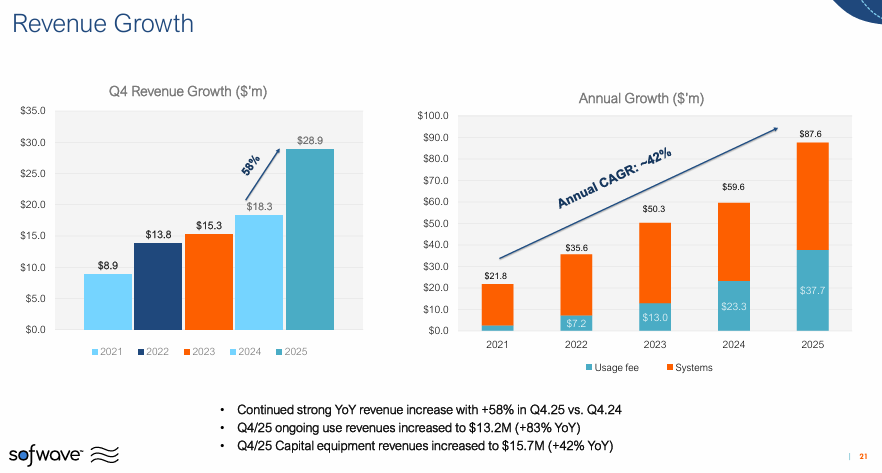

6. $SOFW.TA Sofwave

➢ Israeli MedTech company developing ultrasound-based devices primarily for skin tightening and wrinkle reduction. Competitive advantage versus peers like InMode lies in its non-invasive approach targeting the mid-layer of the skin rather than the deepest layer. Result: no downtime, no treatment damage.

Attractive business model with recurring revenues from ultrasound pulses sold as fully digital consumables with 100% gross margin. Unlike competitors focused on fat reduction, GLP-1 acts as a tailwind for Sofwave. Free marketing from global influencers such as the Kardashians drives strong demand. Recently delivered very strong numbers with >40% revenue growth and inflection to profitability.

💵 2026: ≈25x PE, 2.7x EV/Sales

💵 2027: ≈13x PE, 2.2x EV/Sales

Attractive to me for a company with a long runway for margin expansion and several more years of >20% revenue growth (at least that's what I think).

7. $ETON Eton Pharmaceuticals

➢ U.S. pharma company applying the Harrow playbook (cheap acquisition of Big Pharma–neglected products) to ultra-rare diseases. Portfolio includes treatments for IGF1 deficiency, pediatric adrenal insufficiency, and Wilson’s disease (a copper metabolism disorder). Based on its existing pipeline alone, Eton sees peak sales potential of 500m USD (vs. current 451m USD mcap).

The company aims to operate profitably from Q4/25 onwards and to rapidly increase its operating margins over the next few years. Analysts expect around 30% revenue growth in both 2026 and 2027.

💵 2026: 19x PE

💵 2027: 11x PE

In my view, the stock could double by the end of 2027.

8. $MLUAV.PA Embention

➢ Spanish company specializing in autopilots for drones and eVTOLs – essentially the “brains” of these aircraft, converting sensor data into flight control commands for semi- and fully autonomous flight. Key customer is $AMZN, where Embention supports the Prime Air drone program.

The company’s moat lies in its extensive certifications, including aerospace-grade manufacturing standards. Embention reports only once per year and communicates very little with capital markets, though a recent Q3 shareholder letter hints at improved communication ahead.

💵 56x PE on FY 2024 earnings

I expect exponential growth once drones and eVTOLs reach mass-market adoption for civilian use.

9. $ALLIX.PA Wallix

➢ French cybersecurity pure-play focused on PAM (Privileged Access Management). PAM manages access rights, password security, and session logging for highly privileged accounts like administrators. Many customers operate in critical infrastructure (airports, hospitals, research institutions).

Tailwinds from EU regulations such as NIS2 and NATO’s 5% GDP target (with 1.5% of that allocated to cybersecurity). Transitioning from on-premise to cloud with strong operating leverage (fixed costs flat despite around 20% revenue CAGR since H1/23). Analysts expect more or less 20% revenue growth p.a. over the next two years.

💵 2026: 28x PE, 20x EV/FCF, 2.8x EV/Sales

💵 2027: 13x PE, 9x EV/FCF, 2x EV/Sales

Far too cheap in my opinion. I see at least a 2x over the next 24 months.

10. $5314.TW Myson Century

➢ Taiwanese global leader and first mover in exosome-based nutritional supplements (with a patented plant-based production process), with nearly 400% revenue growth in 2025. Exosomes are nanoparticles released by plants and animals to enable cell communication, offering benefits such as improved regeneration, increased collagen production and reduced inflammation. Furthermore, they increase the bioavailability of added active ingredients many times over.

Company vision: build an AI smart healthcare ecosystem combining health devices, functional food, and health insurance. They also invest heavily in military and civilian drones, aiming to become Taiwan’s equivalent of DJI.

Excellent financials: 63% GM, 45% OM, 129% ROCE TTM.

💵 2025: ≈23x PE on annualized Q3

I expect them to trade at a fwd. PE below 20 for FY 2026.

11. $MOB Mobilicom

➢ Nasdaq-listed Israeli pick-and-shovel drone play producing datalinks for small drones and loitering munitions. Still speculative with low single-digit million USD revenues, but 2026 should be an inflection year as the company transitions from prototypes to serial production and long-term Programs of Record (POR) with Tier-1 defense customers like Teledyne.

According to the CEO, a single POR could generate 20m USD+ in revenue (vs. current 80m USD mcap). Break-even targeted for 2026. From 2027 onward, Mobilicom also aims to generate high-margin recurring software revenues from cybersecurity for AI-based autonomous drone systems – a billion-dollar market, per management.

💵 2026: ≈8x EV/Sales

💵 2027: ≈18x PE, 3x EV/Sales

Base case: ≥40m USD revenue in 2029 with high-30% EBIT margins. Bull case: triple-digit revenues. In that scenario, Mobilicom could become a tenbagger within 4–5 years.

12. $276A.T CCReB

➢ Japanese company focused on advisory- and technology-driven services for compact corporate real estate. Solutions segment includes consulting, fund structuring for real estate sales, project management, brokerage, and short-term holding or leasing of properties on balance sheet, while maintaining ≥50% equity ratio.

Tech segment offers a subscription-based data platform that automatically analyzes corporate reports, derives real estate needs, and generates leads. Major beneficiary of Tokyo Stock Exchange capital efficiency reforms.

Mid-term plan: 67% revenue and earnings CAGR over the next three fiscal years.

💵 FY 2026 (01.09.25 – 31.08.26): 24x PE

💵 FY 2027 (01.09.26 – 31.08.27): 14x PE

13. $0236.KL Ramssol Group Berhad

➢A Malaysian consulting firm that is increasingly evolving into a software and technology platform operator for the ASEAN region. Initially focused on the implementation and consulting of HCM and ERP software, the business now encompasses areas such as EduTech (largely self-developed learning and educational applications for companies and schools), MarketingTech (digital marketing services), AutoTech (operating a marketplace for vehicles including services like driver's license renewal), and AITech (development of project-related AI applications). Revenue growth exceeded 50% in the last quarter. The CEO aims for a 70% recurring revenue ratio in the future (currently around 30% of total revenue).

💵 2025: 18x PE, 4x EV/Sales

💵 2026: 12x PE, 3x EV/Sales

These analyst estimates look conservative vs. recent results and CEO guidance of 50–60m MYR profit in 2026 (this guide would imply a fwd. PE of 6–8).

14. $462A.T Fundinno

➢ Recent IPO. Market-leading platform for private, equity-based company investments (crowdfunding) in Japan with more than 90% market share. The company covers the full lifecycle of startup investments: fundraising (revenues from transaction-based commissions), software & services (recurring revenues for capital structure management, shareholder affairs, etc.), and a secondary market (trading fees for trading unlisted shares). Fundinno also plans to expand its product portfolio soon and offer its own funds. There is significant growth potential in Japan due to the country’s PE market being highly underdeveloped by international standards.

Particularly exciting is the company’s incredible operating leverage: for FY 2026 (01.11.2025 – 31.10.2026), management is planning for 56% revenue growth and an increase in EBIT margin from 8% in the prior year to 29%. The incremental EBIT margin on the revenue delta between FY 2025 and FY 2026 is 66% (!).

💵 FY 2026 (01.11.25 – 31.10.26): 27x PE

I think a revenue CAGR in the mid-30% range over the next 4–5 years, combined with an increase in EBIT margin to >50%, is realistic.

15. $LODE Comstock Inc.

➢ A cleantech company that has developed a technology allowing old solar panels to be recycled with a zero-landfill solution, leaving silver, aluminum, and glass as recovered materials, without harmful emissions. The company is currently pre-revenue / still in the technological testing phase. 2026 is expected to be the inflection year, as the first large-scale facility with capacity of 100,000 tons, i.e. 3 million panels per year, is scheduled to start operations.

Additional facilities are expected to follow in subsequent years. Comstock intends to generate revenue through (1) a tipping fee for accepting panels and (2) selling the raw materials recovered in the recycling process. Thus Comstock would strongly benefit from the currently surging silver price. Beyond this metals business, the company also has a biofuels segment called Bioleum (still far from commercial readiness), as well as currently idle gold and silver mines and various strategically well-located real estate.

💵 FY 2027: 6x PE

If Comstock actually meets these analyst expectations (86m USD revenue, 29m EBIT, 0.67 USD EPS at a current 180m mcap and 3.94 share price), the stock could multiply by then. Longer term, additional facilities, sales of idle assets, and reaching commercial readiness for Bioleum could enable materially higher revenues and profits.

16. $DCTH Delcath

➢ A US biotech that developed a drug-device combination called HEPZATO for the treatment of metastatic uveal melanoma (mUM), an ocular cancer that metastasizes to the liver. The process works as follows: the liver is first isolated from the bloodstream, then high-dose chemotherapy is administered, and the blood flowing out of the liver is filtered outside the body, cleansed of chemotherapy residues, and then returned to circulation.

A few months ago, Delcath released promising study results for treating mUM with HEPZATO + immunotherapy, which could open the door to additional cancer indications and expand the TAM from 500m USD to several billion USD. Mcap currently: 364m USD. Recently, a buyback program was initiated and there were multiple insider purchases by the CEO.

💵 2026: 30x PE, 3x EV/Sales

💵 2027: 12x PE, 2.4x EV/Sales

Very attractive IMO given the long-term growth opportunities.

17. $BXN.AX Bioxyne

➢ A GMP-certified B2B contract manufacturer for medical cannabis, medical cannabis products and psychedelics, essentially a kind of Foxconn of the cannabis industry. Bioxyne buys cannabis raw materials from licensed producers worldwide, processes them in its own facilities into flower, oils, gummies, etc., and delivers them on behalf of customers to wholesalers and pharmacies. The company is active primarily in Australia, Germany, and the UK. Advantage versus other cannabis stocks: no brand or marketing risks. Guidance for the current FY (01.07.25 – 30.06.26): 65–75m AUD revenue and 11.5–13.5m AUD EBITDA (implying 115–150% YoY growth).

💵 FY 2026: ≈9x PE, 6–7x EV/EBITDA

18. $4493.T Cyber Security Cloud

➢ Japanese cybersecurity pure-play offering various cloud-based software modules centered around Web Application Firewalls (WAF). Put simply, a WAF inspects traffic flowing to and from a web application and filters out potentially harmful requests. In addition to its own WAF module, the company also offers modules that allow customers to continuously tailor the pre-built WAFs from AWS, Azure, etc. to their specific needs and keep their configurations up to date. Cyber Security Cloud is one of the fastest-growing SaaS companies listed in Tokyo, with growth rates recently above 30%. As one of very few listed Japanese software companies, CSC also generates meaningful overseas revenue (around 10% of total revenue).

💵 2026: ≈16x PE, 2.3x EV/Sales

💵 2027: ≈12x PE, 1.8x EV/Sales

19. $PRPO Precipio

US diagnostics company for blood cancer detection. They have two proprietary technologies:

HemeScreen, a low-cost, easy-to-use PCR-based platform that reduces test times from 14 days to 2 days versus competing products, and IV-Cell, a culture medium that allows four cell lines to be cultured simultaneously, significantly reducing the risk of misdiagnosis.

The company has been growing at >30% for years despite very disciplined cost management (OPEX has grown only 4% p.a. over the last 5 years) and is close to break-even. OPEX is expected to remain flat going forward per management, while the company should grow topline 15–20% and gross margin should expand from 45% currently to >60% over the coming years due to a changing product mix (more test-kit sales and less lab diagnostics).

💵 2026: ≈42x PE, 1.47x EV/Sales

💵 2027: ≈11x PE, 1.2x EV/Sales

A stock that, in my view, could deliver >40% returns p.a. over the next 4–5 years if my estimates are accurate.

20. $DVYSR.ST Devyser

Swedish diagnostics company focused on hereditary diseases, oncology, and transplant medicine. The company’s Next-Generation Sequencing (NGS) technology enables reading the sequences of millions of DNA fragments simultaneously. The one-tube workflow (= almost all steps in a single tube) reduces error risk, saves time, and conserves resources.

Devyser has the potential to revolutionize the US transplant monitoring market by offering an FDA-approved IVD test kit, allowing clinics to run tests on-site and bill directly, bypassing the centralized CLIA labs. This would turn hospitals from a cost center into a profit center - a fundamental incentive shift - under which Devyser could, in an optimistic scenario, increase its own revenue by more than 20x compared to the current base.

💵 2026: ≈45x PE, 5.4x EV/Sales

💵 2027: ≈24x PE, 4.2x EV/Sales

21. $HIT Health In Tech

InsurTech enabling companies in the US to transition to self-funded health plans by digitizing planning, underwriting, and administration. Via the eDIYBS platform, brokers and TPAs can generate bindable quotes for health and stop-loss plans within minutes, instead of months as is standard in the industry (fee-model). Through Stone Mountain Risk, brokers or TPAs can structure self-funded health plans (recurring revenue per enrolled employee). Massive revenue potential in a huge, roughly 40b USD TAM with meaningful digital disruption potential.

💵 2026: ≈23x PE, 1.6x EV/Sales

💵 2027: ≈12x PE, 1.1x EV/Sales

Two additional stocks I can not publicly disclose for confidentiality reasons: a pick-and-shovel drone play, and a Japanese job-recruiting platform with software-like gross margins, 30% revenue growth p.a. targeted through 2029, and a valuation of >0.3x EV/Sales.

On my watchlist are, among others, SK Hynix and an Australian mining stock that could generate almost its entire current mcap in FCF next year (I can’t disclose this name either).

English