固定されたツイート

I’ve been trading for ~30 years.

First half: fully discretionary, living inside futures microstructure. It worked—until algos started exploiting the same patterns and reacting in microseconds. Edge decay was real.

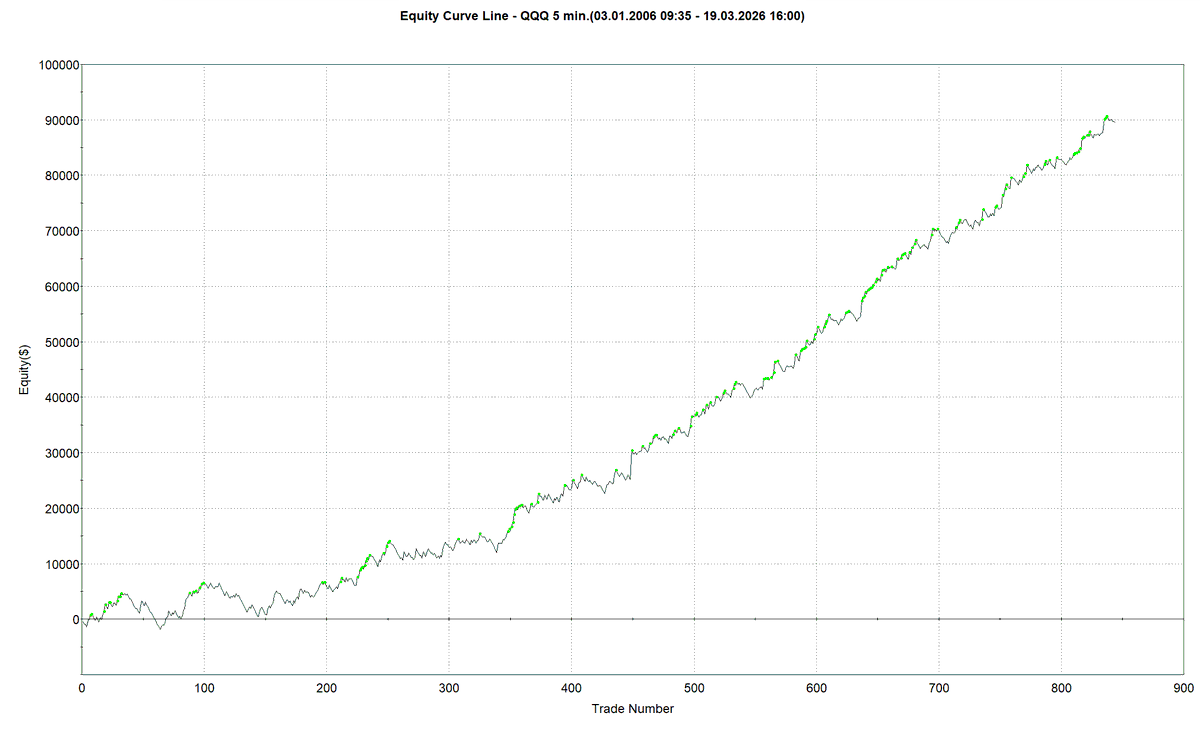

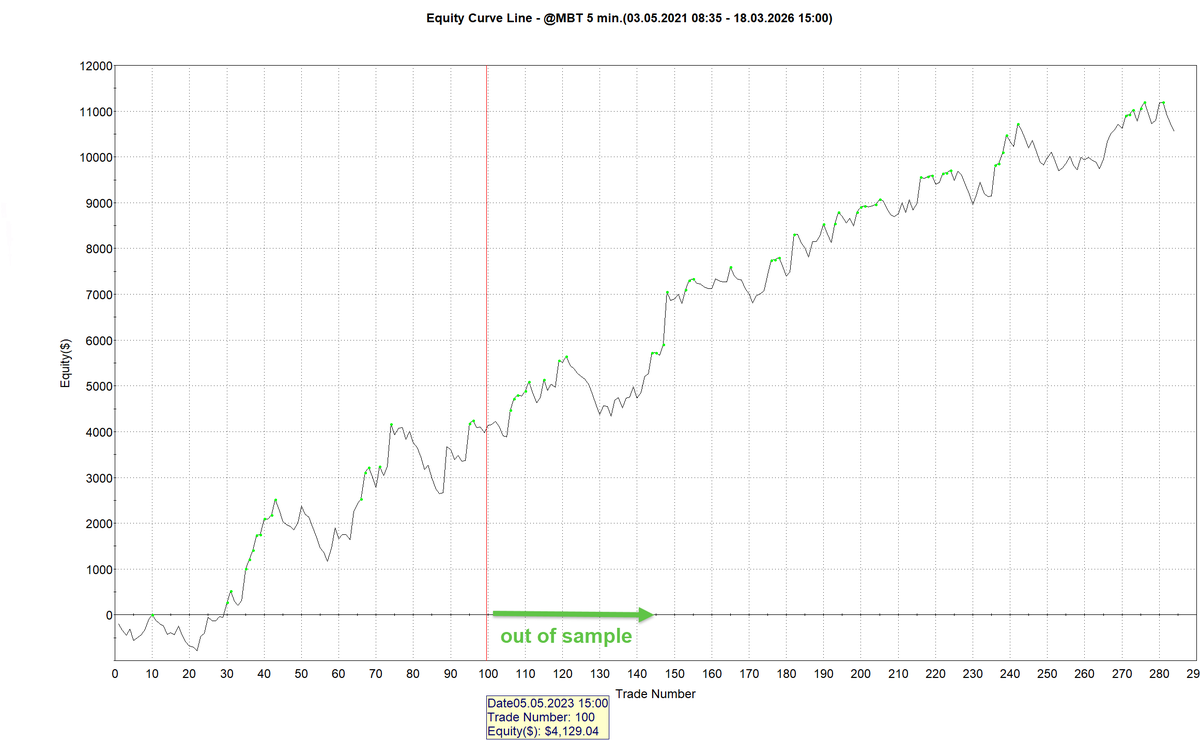

So ~10 years ago I switched to systematic.

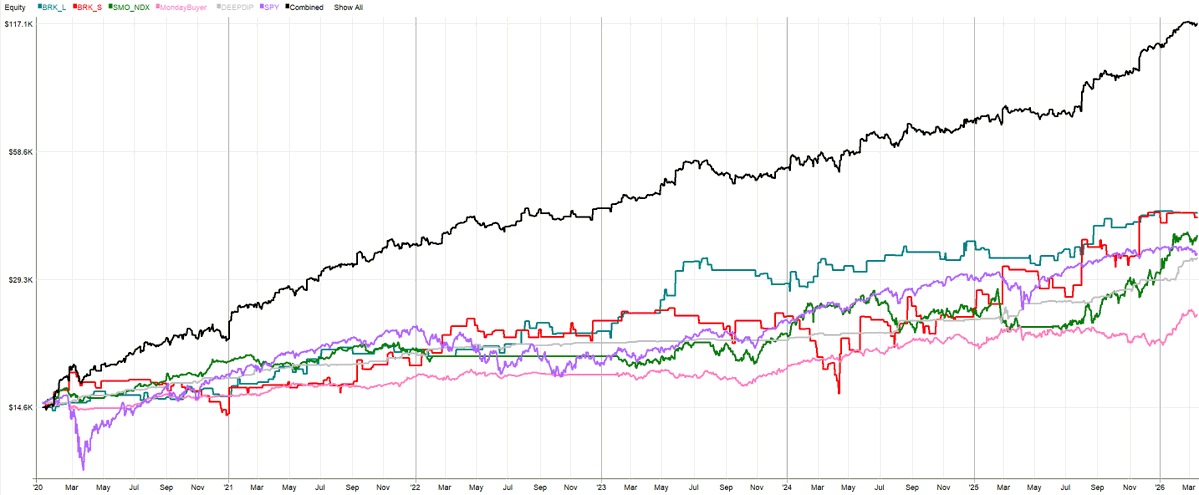

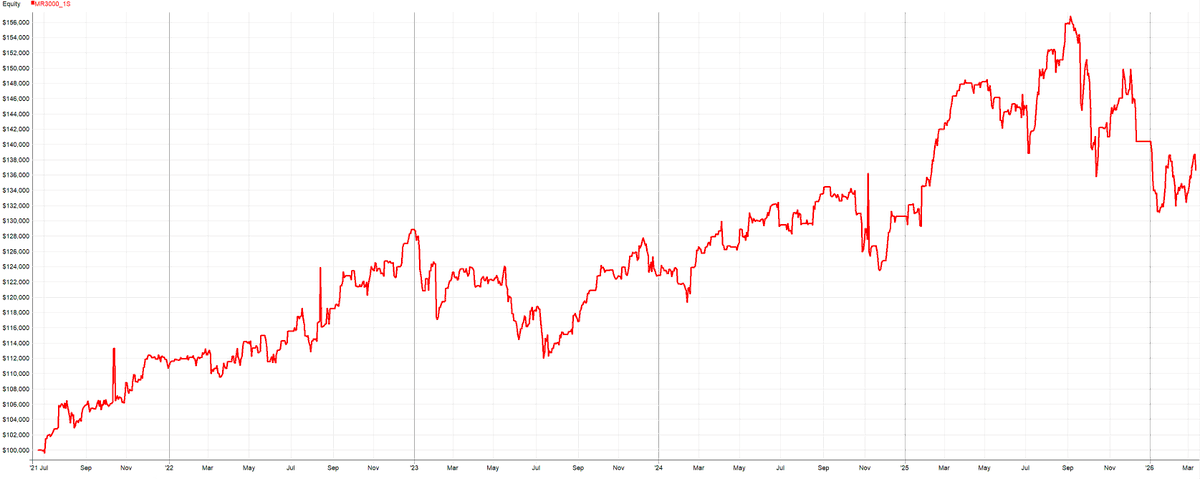

Now I run many uncorrelated strategies in parallel without babysitting screens all day. I wouldn’t go back.

My biggest unlock: reusability of know‐how.

When I finish a new system, I plug it into a ready workflow in minutes. It monitors itself; I move my brain to the next big thing.

Here’s the playbook I wish I had from day one:

- Framework (design once → reuse forever)

- Data → clean, feature, label.

- Hypothesis → simple, testable edges (breakouts, momentum, mean reversion).

- Validation → IS/OOS, realistic costs/slippage.

- Risk → position sizing, max heat, portfolio exposure caps.

- Deploy → automated orders, fail‐safes.

- Monitor → health dashboards, kill‐switch rules, mobile app.

- Iterate → new systems slot into the same pipeline.

Principles that compound:

- Many small, independent edges > one “genius” setup.

- Process beats prediction.

- Shipping beats perfecting.

Discretionary taught me markets. Systems gave me scale.

English