Sabitlenmiş Tweet

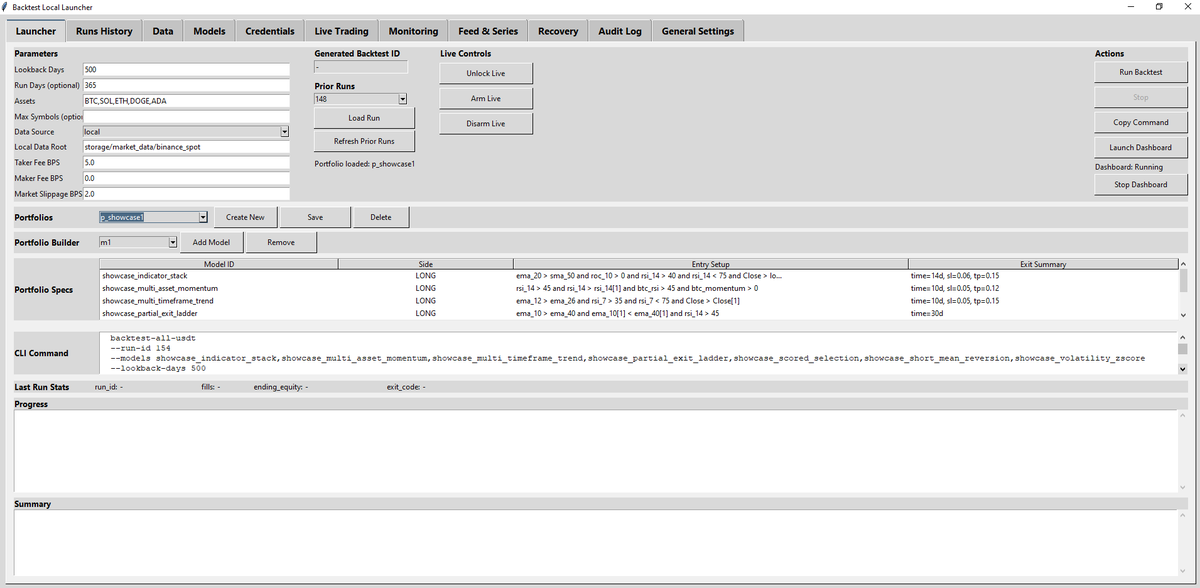

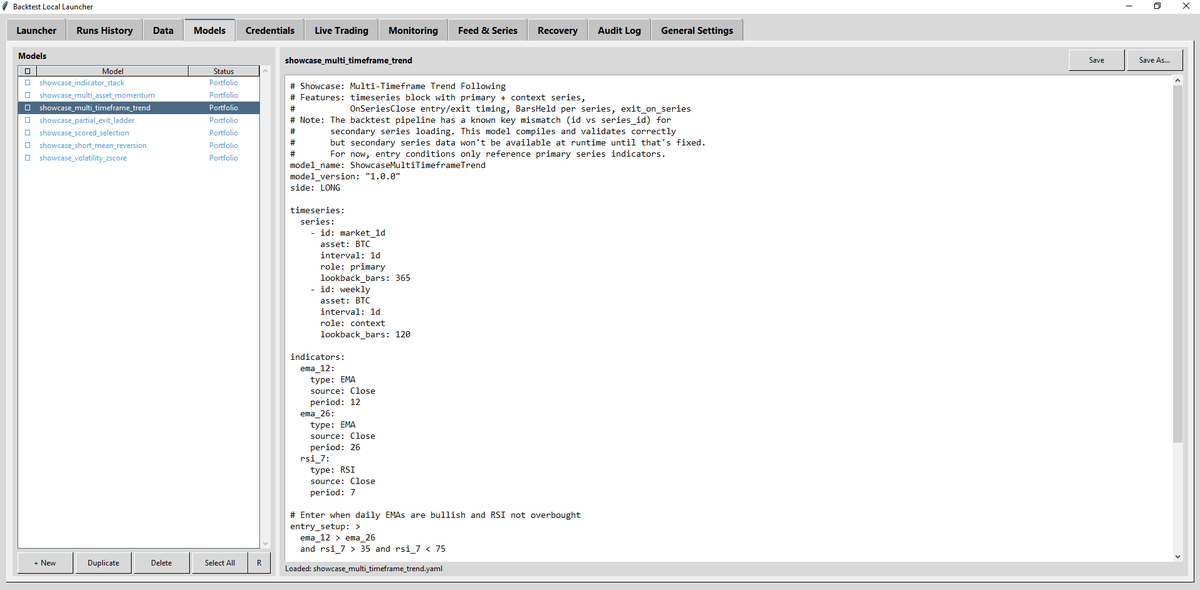

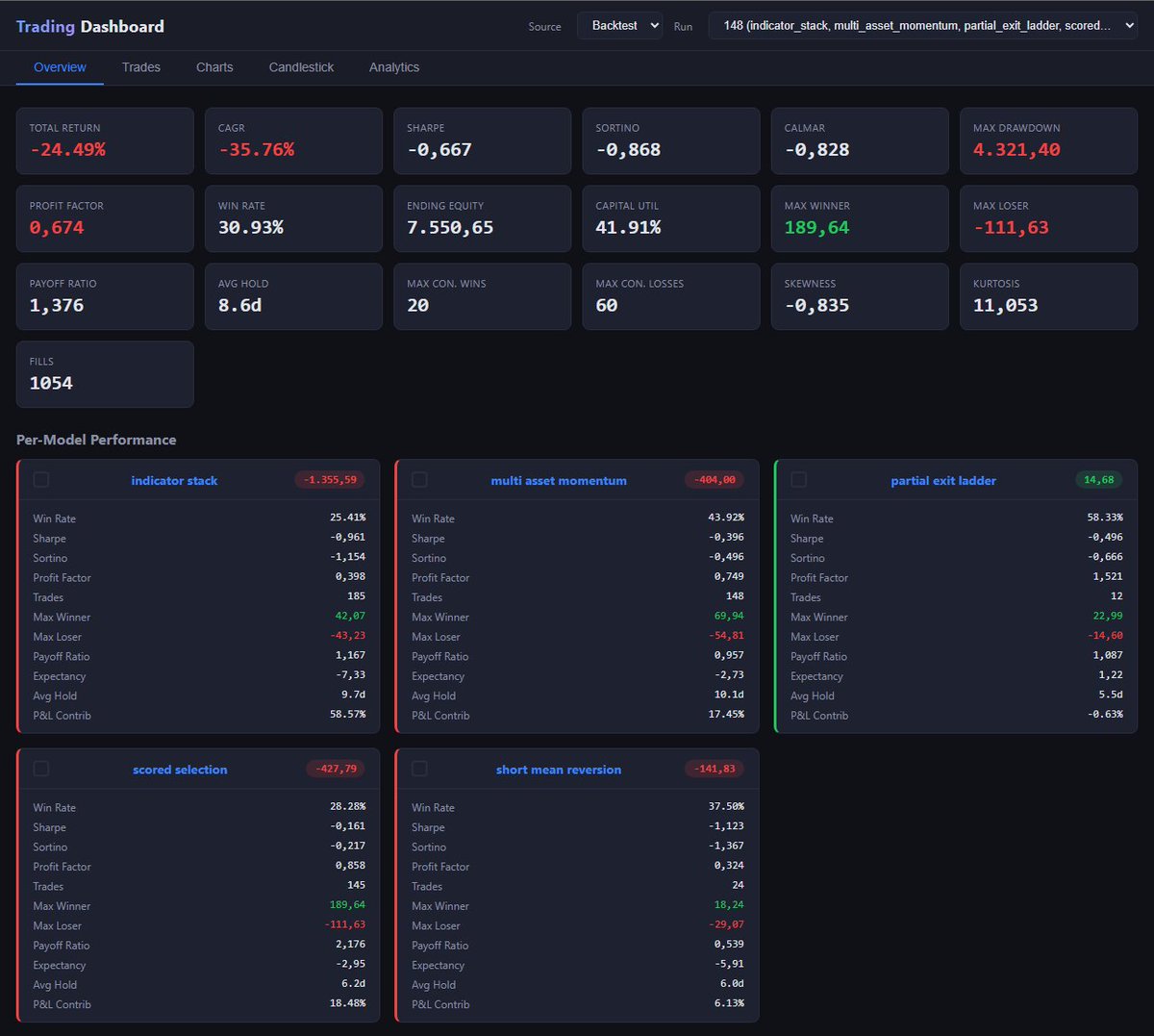

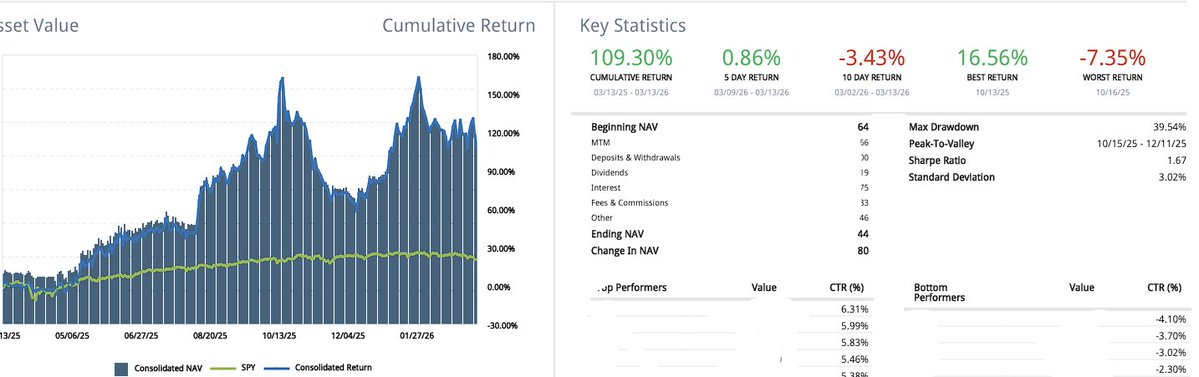

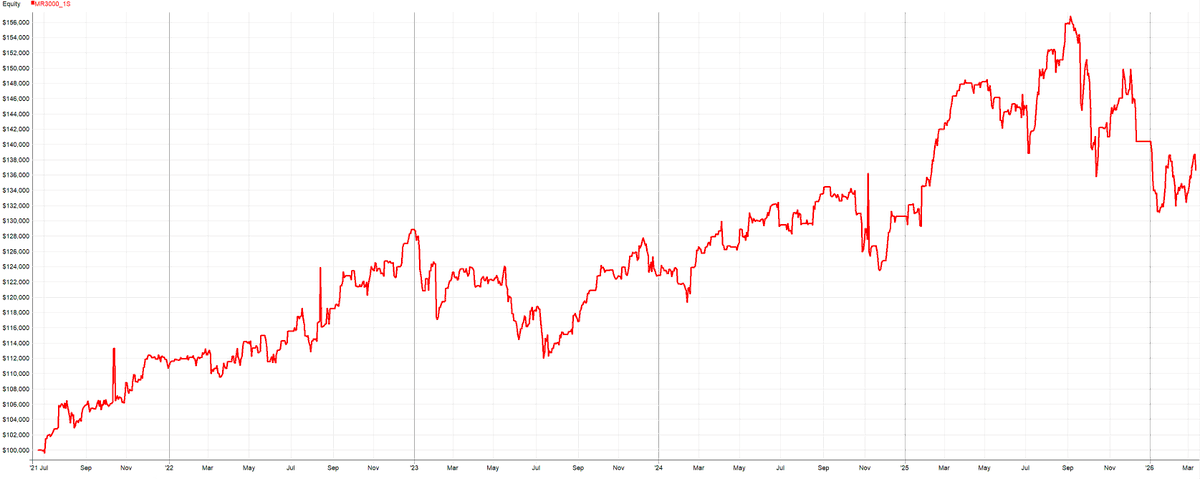

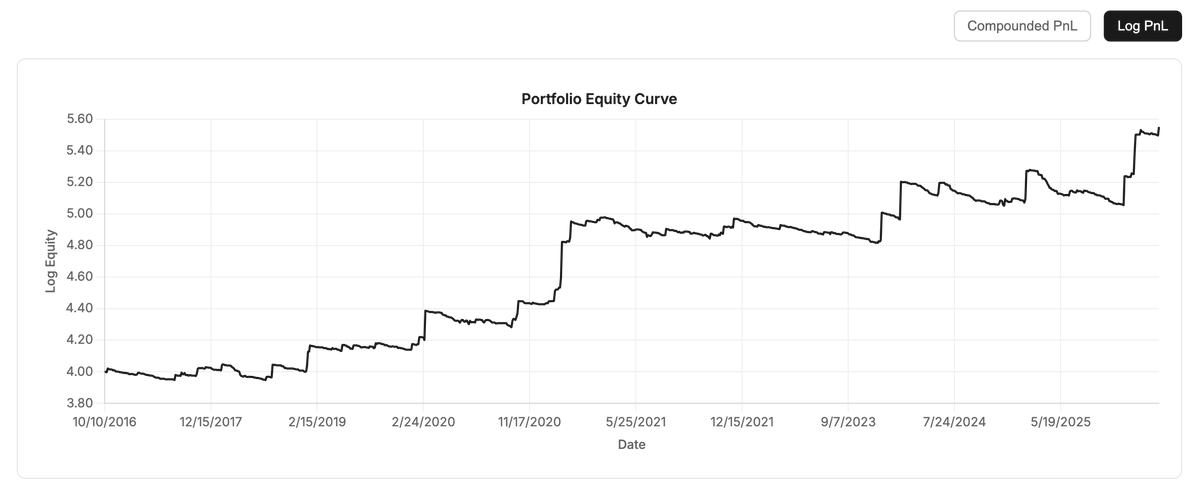

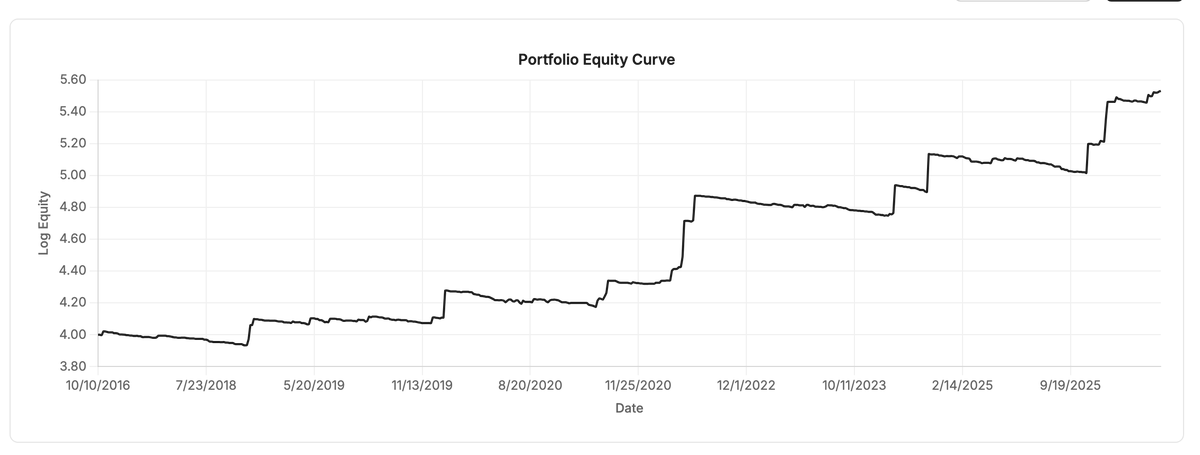

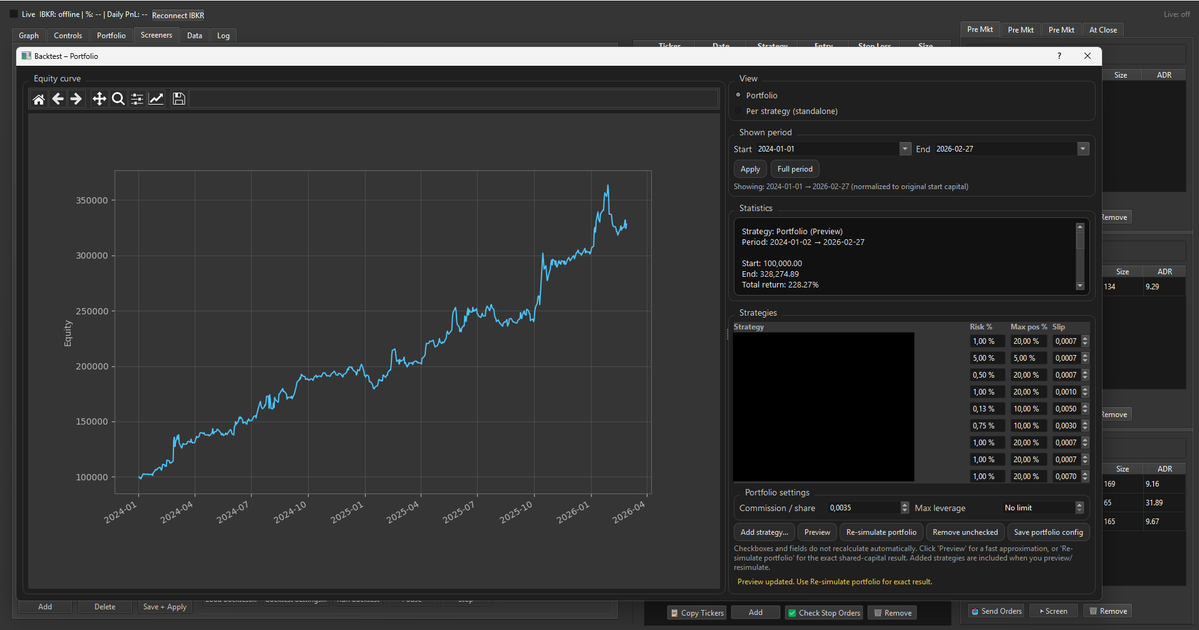

Finally done with the backtest part of my platform. Really happy with how it turned out! Easy to add a strategy and see how it changes the portfolio dynamic with different risk settings etc.

English

ATCOTrader

821 posts

@AtcoTrader

Discretionary trading done systematically.