Adu Subramanian@plainyogurt21

****2025 BioX Year in Review****

Not to be taken seriously: $XBI

A long time ago in a galaxy between San Diego and Boston, a traveler arrived at the gates of BioX on January 1st, 2025.

The feeling was uneasy. Against all common wisdom to jump on the next big AI startup, Bitcoin, or index in big tech, they'd felt a calling to biotech. One clinical trial readout sending a stock up 100% and now they’re hooked. But aimless.

"Welcome, young traveler," came a voice from the shadows, like a Jedi master who'd seen a thousand battles.

@sports_bios emerged, dressed in robes the color of tulips, his presence radiating the wisdom of the Old Republic.

"Fear not the names and pay attention to only the information," he said, his voice carrying the weight of many market cycles. "Charlatans and masters come in many forms. The dark side and the light are not always where you expect. You may learn something from the jedis such as @BiotechElmo @Vulpescap @Biopharmaddict @BayAreaBiotechI, @Biohazard3737 and others who walk these paths. Some analyze in the light, some retracted by compliance: both have their place with the Force."

Sports took the traveler to a Jedi temple where holographic cherry blossoms bloomed year-round, each petal inscribed with molecular structures.

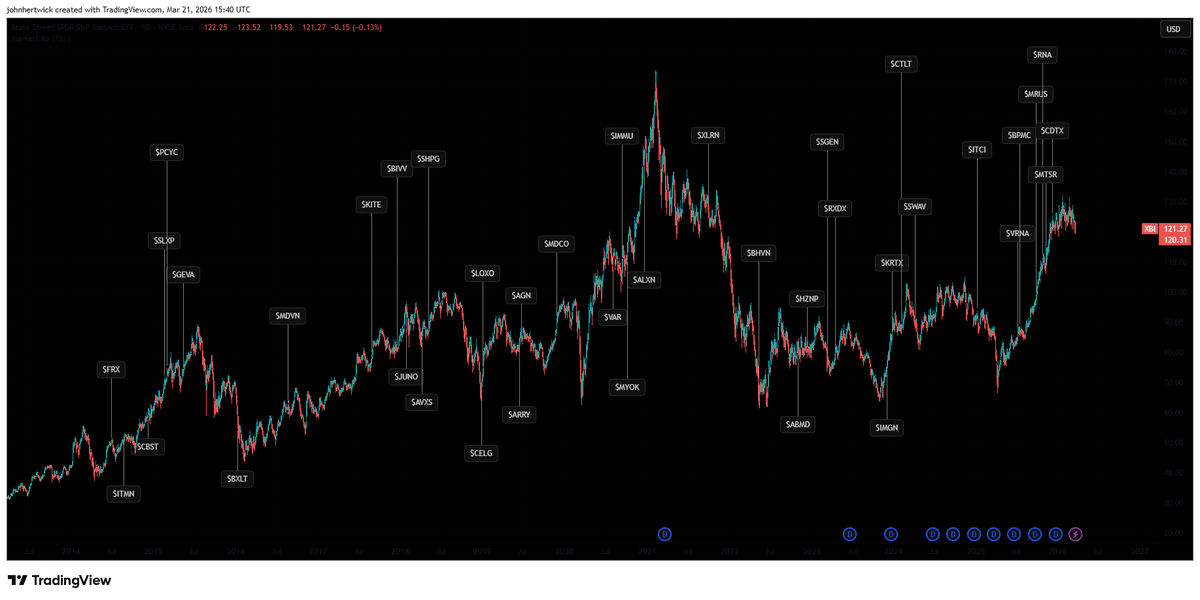

"The XBI has been flat for five years while NASDAQ has outperformed," he said. "Palantir investors who know nothing of the company make millions while Jedi PhDs toil day and night to predict clinical trials. This is the imbalance in the Force you've entered. But there is opportunity in the chaos, if you learn to see it."

As the year began, the FDA was under turmoil but biotech operated like usual. Some stocks went up, some went down. Overall, M&A had slowed. Capital flowed to tech. The traveler received transmissions from friends minting money with any startup containing ".ai" in their name.

The jedis shake their head: "The market rewards narrative over substance, until suddenly it doesn't. Trust in the Force, trust in the data. Our time will come."

But beneath the calm, something was stirring. A shadow growing. Foreboding a downturn in March, a patient died with $SRPT's gene therapy, Elevydis. (this wasn't the end of that saga)

Then as we entered March, $ARVN blew up down 50% in a single day. And sentiment took a turn for the worse in April.

The number of negative enterprise value companies peaked. At the bottom, XBI was flat over a 10-year period. The traveler read the threads on BioX and worse than despair was desolation. All the analysis was dried up. We used to analyze trials and now we congratulate CEOs for CLOSING their business $THRD @adamfeuerstein

Sarepta killed a patient in March, another in June. (Turns out it was actually two in June, but they didn't feel it necessary to announce it). The FDA places a hold on shipments as they wait to resolve it. Once a $200 stock now down 90%, iffy data came back to bite them, a recurring theme in biotech. Sadly, everyone lost a few IQ points listening to the company in the summer.

"The kind of drop I've had in the past two days has been extremely rare for my style, no leverage, the type of names I own, so we are definitely at some kind of liquidation extremes." It was April 1st. The date felt like a cruel joke from the Force itself.

$LXEO reported unprecedented data and raised money at all-time lows. $STOK partnered with a company for a deal worth more than the company itself and the stock dropped. Everyone on BioX was redacted by compliance or left the platform entirely. And worst of all: Sports_bios was gone in April.

The traveler stood alone in the empty temple, an ObiWan like presence gone from the force.

They had a choice: fold under the pressure or lean into the potential rally.

“The bear market killed biotech”. No Luke. The bear market IS biotech”

But in the depths of despair, in an almost poetic way, Sports' sacrifice flipped a switch in the market. It was one readout, a buyout, then another. The Rebellion was beginning.

$RGLS was bought out April 30th for 10x the stock price. $ALNY was starting to commercialize in ATTR-CM $INZY was bought out May 16th. $BBIO reported strong earnings in May 2025.

End of part 1

Before a noisy September approached, the traveler needed more training in the summer

They found @A_May_MD in his swamp, a corner of BioX where he'd been analyzing data for years. Fighting off trolls from $HIMS and $VKTX. Bold enough to take them on when no one else had the right combination of fire and intelligence.

"Rezpegged, you will be," Adam said in his peculiar way. "Nektarded, many become. Hmmm. Learn from this, you must."

The traveler didn't fully understand, but he listened. They joined @houndcl to learn med chem, @Prof_Oak_ to learn gene therapy, @Sanctuary_Bio to learn a steady hand and testing their skills with @bingbingbom @drug_smolecules @LY4101174. "understand their posts to be a true jedi".

Make sure you understand who is serious among the crowd: @MelvinRiskMgmt @TheBiotechBear @ESG_Biotech may say unserious things meant not to be taken seriously.

The most dangerous training was with the bounty hunters: @Biotenic @jesse_brodkin. The downturn didn’t phase them: "What if the company doesn't survive? He's worth a lot to me." - These bounty hunters seeked the frauds and charlatans to send them to 0. Beware them short your company.

And things started to break the right way in the summer $CDTX seemed too obvious but the stock was up 100% on the phase 2 results. The anti vaxx movement and a heavy flu season provided an opportunity for a flu prevention treatment to be huge.

The traveler trained in Adam's swamp, learning to see beyond the obvious, to trust in unexpected outcomes. $NKTR was a positive Risk Reward heading into phase 2b results in atopic dermatitis trading at cash. And boom it reads out positive. Better than dupi? Maybe not, but the phase 2b established proof of concept for the nobel prize winning TReg hypothesis.

And in July, Adam released a thesis on $ABVX. The next day, they released phase 3 results in Ulcerative Colitis. The stock was up 500%. As if that wasn't enough, $CELC released phase 3 breast cancer results that same month sending it up 300%.

A few readouts went right and was Biotech Back? @CloisterRes was finally able to order fries with his mcgriddle

And from ABVX and NKTR emerged @seedy19tron , not a jedi, but a rogue high risk pilot caught up in the ARVN blowup. Originally thought to be dead, he came back from the frozen carbonite. The rebellion needed a leader and h̶a̶n̶ ̶s̶o̶l̶o̶ ̶ Seedy started to step up with weekly reviews of his portfolios. Seedy would soon become the face of BioX even as a rogue, untrained risk seeking pilot. People sometimes look at him as like a shill but

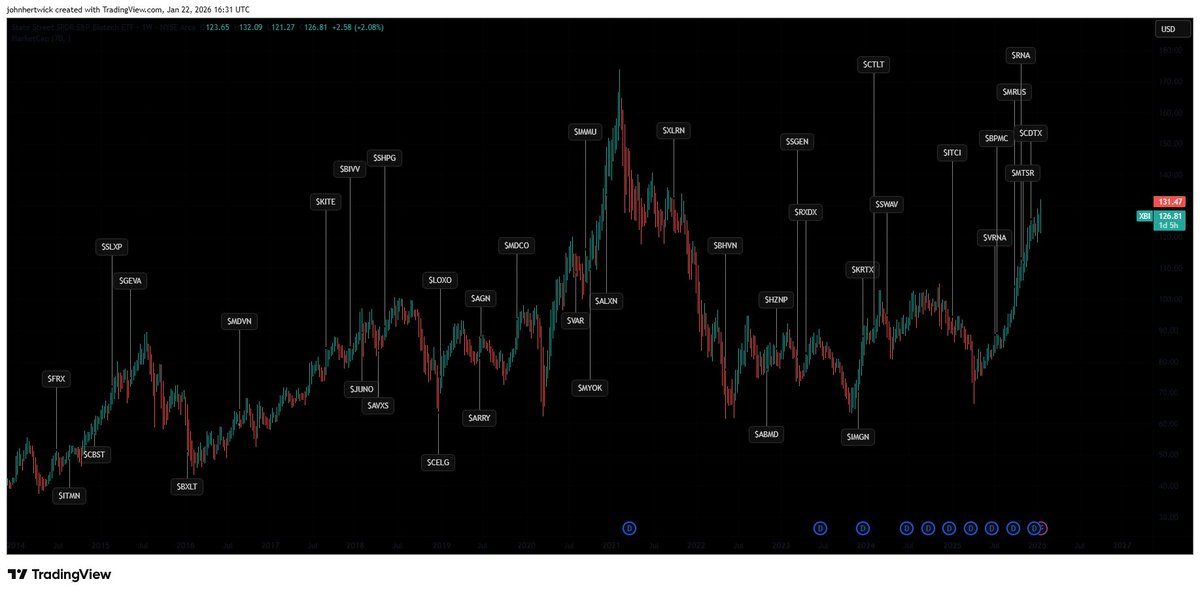

September rolled around. XBI was finally flat year-to-date. It was time for the epic September/October that would define the year.

Kicked off by an unexpected $UTHR win. Maybe FVC doesn’t measure just fibrosis…..

$RAPP somewhat positive data in FOS, up 100%

$DNTH somewhat positive data in gMG, up 100%

Everyone’s getting an FGF21 like Oprah ($ENTB, $AKRO). Overpay? Who cares?

$MBX disappoints with hypoPTH data? Doesn’t matter, $MTSR bought out and the stock is up (one of the last parting gifts from sports_bios).

$CYTK proves to use Beta blockers are Doodoo for oHCM

$TRML acquired

$SRRK CRL? Libtayo CRL? Catalent plants have rats? Doesn’t matter, stock is not down.

$QURE up 300% because they hit the bar set by the FDA in a 12 person externally controlled phase 1ish trial without biomarkers to demonstrate efficacy

IONS shows unprecedented efficacy in sHTG.

@bigpharmaguy drops in for a second “$PRAX didn’t actually fail an interim” and disappears into the shadows. That ET phase 3 is a success.

Do you have a UC drug? Sure, time to get funded $PALI $EQ. We’re looking for the next ABVX

$SPRB was 1 month from running out of fuel when the FDA gave them clearance to file and it pumped 20x in one day. @MSollender caught this early as it was happening

It’s not all wins for everyone.

$MLTX is a complete failure, wiping out some huge positions. Butit’s okay because we’ll just buy $Zura and $AVTX instead for HS.

Some clear shorts with their stock up 300% into a readout fail (oh no who could have predicted $ATYR $KALA). $NTLA kills a patient and gene therapy for ATTR is DoA.

And we round out the year with extreme bullishness: Do you have a drug in a clinical trial? Are you a complete dogshit company? If yes and no, your stock is up 100%.

Amidst all this, m̶o̶s̶ ̶e̶i̶s̶l̶e̶y̶ ̶c̶a̶n̶t̶i̶n̶a̶ the FDA is in turmoil Who shot first? Prasad, Makary, pazdur, or the FDA? We don't know but 90% of leadership is gone. Heads of CBER, CDER all leaving. $REPL kept their head on a swivel with a CRL, potential reversal, and a reversal again: where are they in the process? Vinay Prasad left and came back. Pazdur changed roles, took pictures with everyone and then departed. For Uniqure, a unique hope for Huntington’s disease, the FDA reverts prior guidance and asks for more than 12 patients with an external control on highly variable endpoints. In an act of virtue?desperation?greed? Quality investors and shitco CEOs band together to call out the flip flopping. "We're okay if you don't like the data (we don't either), but you can't keep flip flopping". Yet how short our memory is in the fog of war: we’re quickly onto the next. The FDA turmoil is put aside as biotech churns forward.

The buyout spree continues: $RNA $CDTX $FOLD $DVAX all billions for a buyout. If @JoseRestonVA is in a company, watch out it might be bought out tomorrow. Big pharma is feeling the pressure of Billions in loss of expiry. Ater October and September, The year returns back to a normal cadence: readouts from a predictable failure in $AGIO, success in $FULC in SCD, $DBVT in Allergies, $COGT in GIST, and unpredictable failure in $RZLT for cHI

Exiting 2025 and bioX has been through a lot. Sports Bios level headed takes ring in our Hero’s ears and he looks out at the landscape: “Are buying too much?”

Phase 0 companies worth 1̶.̶5̶B̶ ̶1̶.̶8̶B̶ 2.2B $GLTO. If you do a PIPE with crazy warrant coverage, you get bought.

Phase 1b Atopic dermatitis data rewarded with billion dollar valuations. The acquisition and data spree has catalyzed extreme bullishness. $KYMR Any biotech is up 100% in 6 months. $CAPR with a successful phase 3

The techbros have started to take aim at biology. “We’re going to solve biology”. Uh oh. Do they know what a clinical trial requires? Do they realize that $JSPR failed because the investigators didn’t enroll patients with the right disease? Retro Bio is now worth 5 Billion to target "aging"……What does that even mean? China is fast on the US tail and reg bros are pleading with the FDA to modernize their process.

Maybe it’s time to take a step back. We reflect on the year.Obesity is at the forefront but eerily, the king stays the king: Lilly and tirzepatide are taking over and a temporary blip in oral GLP1 data gives way to all time highs for $LLY. 2026 brings the first round of IRA negotiations, biosimilar competition, MFN pricing but will this truly impact us? A new wave of biotech IPOs is ready to mark the top.

Seedy found our hero overlooking the therapeutic landscape

"Poetic, wasn't it? The master falls, and in his falling, the market finds its floor."

"we are beyond back," the traveler said. "It's taken a toll, but we fought a battle with high highs and low lows.

"We've lost some truly valiable onesSports is gone. Michelle Solly is gone."

"and gained som quality new faces @idalopirdine @BalaBioResearch @3rdFloorCapital @mickeychiku @rezfszubagoly

"And now?"

"Now it's time to enter the new year and prepare for round two. Time to look at ASCVD, wAMD, HS, NSCLC, IPF readouts and start anew."

Seedy nodded. "You sound like you've learned something."

- Always understand the trial design

- Never invest in a "shitco"

- never become a single stock account

- Placebo controlled data is king. Phase 3 data is king.

- Admit when you're wrong.

- Most of all: Don't be an asshole.

Then they turned and walked back into the marketplace, ready for whatever 2026 would bring.

From the Chronicles of BioX, Year of Transformation Recorded by a Padawan.