Agrinfo

1.9K posts

80% HOUSEHOLDS MAY CUT TRAVEL, 50% MAY REDUCE LPG USE IF FUEL PRICES RISE: SURVEY A recent nationwide survey highlights a sharp demand-side shock risk if fuel prices are hiked in India: ~78–80% households say they will cut non-essential travel ~50% say they will reduce LPG usage ~35% may shift to public transport (bus/metro/train)

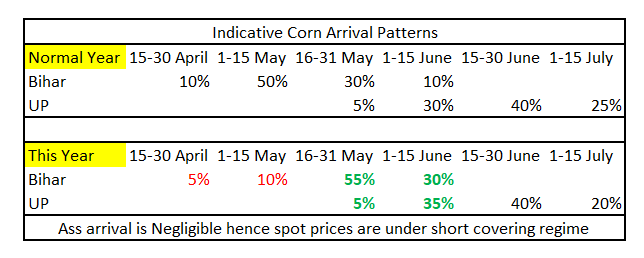

This year Bihar farmers will have to compete with UP crop around the same time. Normally there used be a 30-45 days gap between both crop arrival times. But this time both arrivals are going to be almost overlapped (If no weather concerns in UP) Going with this 15 May-15June shall see a good arrival pressure in north India. #Corn #Makka

Current rains may impact quality in Bihar #Corn but for sure these rains are quite good for Uttar Pradesh Crop. Further, we should keep an eye on the area switch in Punjab in the upcoming crop amid govt initiatives. Indian #Corn spiked in last week due to delayed arrival in Bihar but arrival is expected to start around 2nd week of the may. Time to stay cautious for sometime.

Recent rains in Bihar are going to destroy quality so less export and more ethanol quality supplies will be available. This may create a quality spread in corn in the coming days. The market is going to be volatile. Geared up for Corn 2026

How exports can happen? Indian market is almost closer to the parity of APW, how we can see some trade confirmation in coming days. 1) If Australia goes up – possible. 2) If India goes down – possible. 3) If INR moves to around 92/93 – less likely. Black Sea wheat is about USD 40 cheaper than Indian wheat, so Indian prices need to correct by at least ₹3,000–3,500 per MT for this trade to happen. Therefore, India can not compete against Black sea. How much can happen? Very limited quantities will be traded. APW will always be preferred by buyer, and if Indian exports happen, APW prices may come down to push India out of the export market. Indian prices will act as the ceiling for global wheat prices. What should domestic millers do? Consider ₹24,000–24,500 delivered at Kandla as the market bottom for some time.

URS Noise Fades in Data: Procurement Trends as on 28 April 2026 Concerns around URS (Under Relaxed Specifications) wheat appear overstated when seen against actual procurement data. Total wheat procurement has reached 212.09 lakh tonnes, of which only 10.85 lakh tonnes (~5%) is URS, while 201.2 lakh tonnes (~95%) is FAQ quality. Punjab–Haryana: Strong Quality, Negligible URS Punjab has procured 103.4 lakh tonnes (against a target of 122), with URS at just 1.68 lakh tonnes (~2%). Haryana has exceeded its target of 72 lakh tonnes by procuring 74.26 lakh tonnes, entirely FAQ, with zero URS. The data suggests no major quality concerns in the key procurement states. Uttar Pradesh–Madhya Pradesh: Procurement Lags Behind Targets Uttar Pradesh has procured only 6.1 lakh tonnes against a target of 25 lakh tonnes, with URS at 1.62 lakh tonnes (~32%). Madhya Pradesh has reached 19.3 lakh tonnes against a target of 100 lakh tonnes; all procurement is FAQ, with zero URS. Despite bonus incentives, procurement pace in MP remains slow. In these states, the issue is not quality, but weak procurement momentum. Rajasthan: Highest Impact of URS Out of a target of 23.5 lakh tonnes, procurement stands at 8.54 lakh tonnes, with 7.54 lakh tonnes (~88%) as URS and only 1 lakh tonnes as FAQ. URS impact is clearly concentrated in Rajasthan. Even with the highest MSP bonus, procurement remains limited. Year-on-Year Comparison (as on 28 April) Punjab: 95.15 → 103.4 lakh tonnes Haryana: 63.7 → 74.26 lakh tonnes Uttar Pradesh: 7 → 6.1 lakh tonnes Madhya Pradesh: 63.88 → 19.3 lakh tonnes (sharp decline) Rajasthan: 10.6 → 8.54 lakh tonnes Key Takeaways URS-related concerns have not materialized at the national level. The bigger concern now is weak procurement in several states, not grain quality. Procurement is currently in the mid-phase, likely to peak over the next 15 days and may taper after 15 May. Punjab and Haryana are expected to exceed procurement targets. Overall, URS procurement remains far below earlier expectations. Historical Context: URS Stocks As of 1 April 2021, central pool URS stocks stood at: 26.45 lakh tonnes (from 2019–20 season) 126 lakh tonnes (from 2020–21 season) This comparison further highlights that current URS inflows are significantly lower than past elevated levels. igrain.in/posts/urs-nois… @VIVEKJLV @sandeepbansal28 @JainPaharia @CheshtaE