RT @SimplyBitcoin: ARTHUR HAYES: "Since the war has started Bitcoin has outperformed the NASDAQ and Stocks and i think Bitcoin is now focus…

English

AhteR

737 posts

Strategy has acquired 13,927 BTC for ~$1.00 billion at ~$71,902 per bitcoin and has achieved BTC Yield of 5.6% YTD 2026. As of 4/12/2026, we hodl 780,897 $BTC acquired for ~$59.02 billion at ~$75,577 per bitcoin. $MSTR $STRC strategy.com/press/strategy…

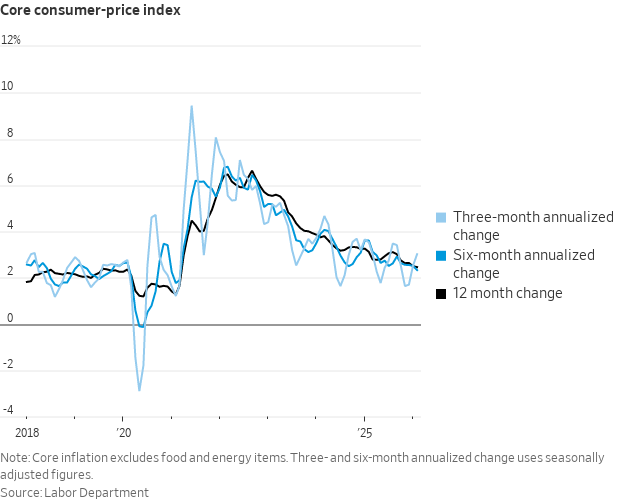

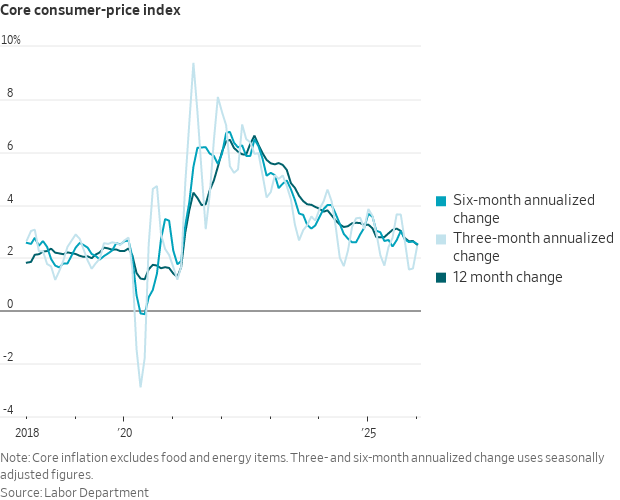

Wall Street has inflation as measured by the CPI running sideways in February and holding near the lowest 12-month rates in five years* *at least until April, when the data collection/imputation distortions from the Oct govt shutdown could fully unwind

Two different measures of business inflation expectations have essentially returned to pre-pandemic levels. The Atlanta Fed survey (dark line), which asks businesses how much they expect their own unit costs to change, is back at 2%—right where it was in 2019. The Cleveland Fed survey (teal line), which asks business executives where they expect CPI to run, is back around 3%—similar to 2018 readings. These suggest that price-setters don't see unusual inflation ahead (after a bump last spring). Both measures jumped in 2021 and have now fully round-tripped.

🚨 KEVIN WARSH IN FOCUS AS U.S. INFLATION FALLS TO 0.68% As of February 9, 2026, Truflation reports that U.S. real-time inflation has fallen to 0.68%, far below the official Consumer Price Index of about 2.7%. The sharp decline is raising pressure on the Federal Reserve to resume interest rate cuts. Analysts are watching nominee Kevin Warsh closely, with some predicting up to a 1% rate cut later this year. Market pricing suggests a high likelihood of one to two 0.25% cuts in the second half of 2026, with speculation about an earlier move if official data aligns with Truflation’s readings.

Wall Street expects a cooler month for headline inflation but a hotter month for core in January Headline CPI: 0.26% m/m, 2.5% y/y (down from 0.31% m/m and 2.7% y/y in December) Core CPI: 0.34% m/m, 2.5% y/y (core m/m accelerating from 0.24% in Dec, but y/y ticking down from 2.6%) Worth noting the atypically wide range on core CPI forecasts (from 0.25 to 0.42), suggesting more uncertainty about turn-of-the-year effects, with tariff passthru adding another layer of fog.