Alreits Research

1.3K posts

Alreits Research

@alreits

Your go-to platform for REIT-focused research, now supporting Stocks & ETFs. Expert insights to help you invest smarter in REITs, Stocks, and ETFs, globally

Katılım Mart 2021

91 Takip Edilen545 Takipçiler

Alreits Research retweetledi

REITs today are trading at 20–40% discounts to NAV.

That means:

You can buy $100 of real estate equity for $60-80.

With:

• Liquidity

• Diversification

• Professional management

This rarely happens.

English

Alreits Research retweetledi

📊 REIT Earnings Quick Take

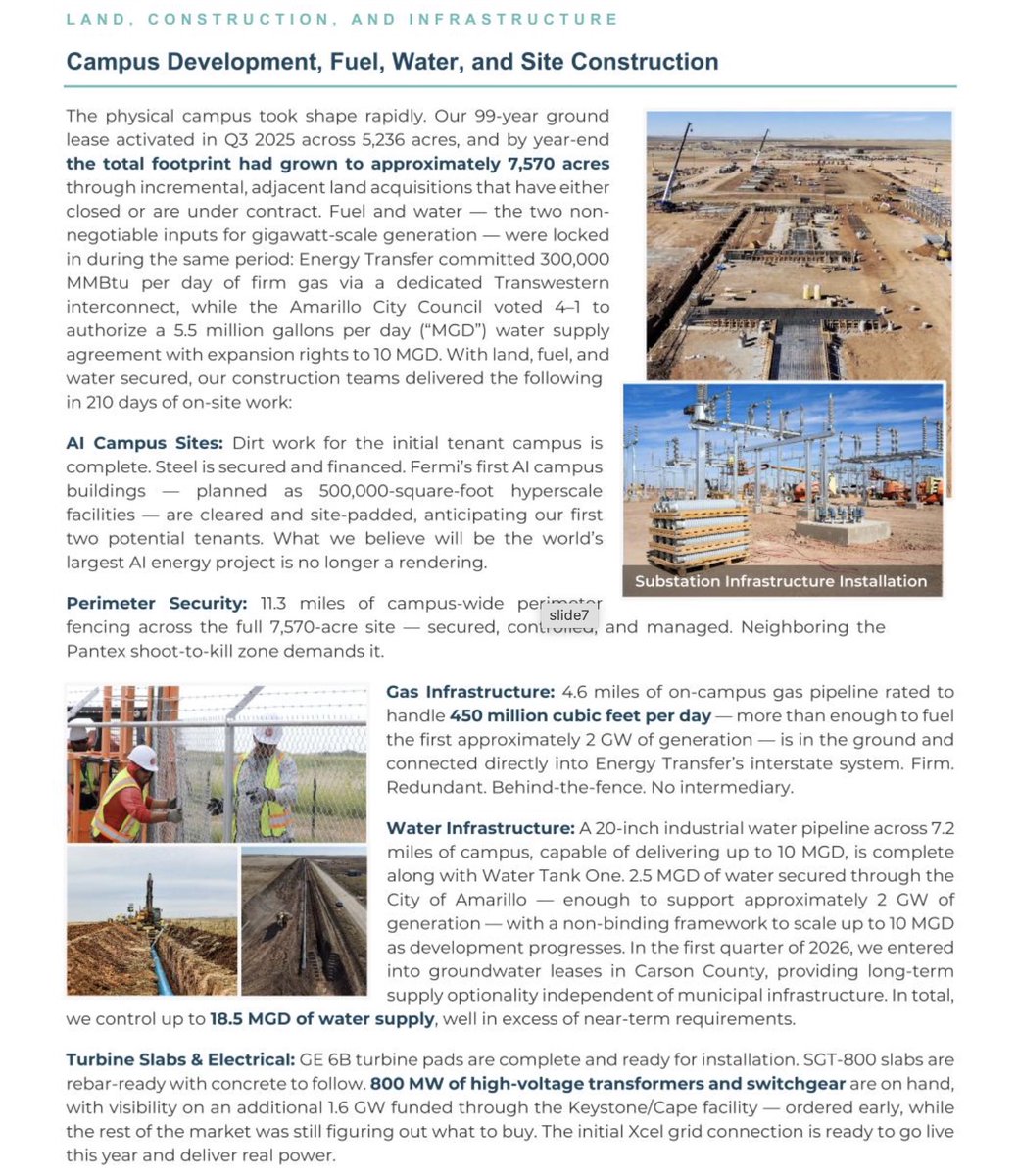

Data Center REIT Fermi (FRMI) – which went public last year in a highly anticipated IPO tied to the AI infrastructure boom – tumbled today after reporting its first full fiscal results while acknowledging that it has yet to sign a definitive tenant lease for its planned hyperscale data-center campus.

$FRMI declined more than 10% today following the release and are now dwn about 75% from their IPO price, reflecting mounting investor skepticism around the company’s timeline to secure an anchor customer.

The Amarillo, Texas–based company is developing Project Matador, an ambitious off-grid data-center campus powered by dedicated electricity generation intended to support AI workloads and hyperscale compute demand.

The concept centers on pairing massive compute facilities with private power generation—initially natural gas with longer-term plans for nuclear—allowing hyperscalers to secure large blocks of electricity without straining regional grids.

Ahead of its IPO last year, Fermi disclosed a Letter Of Intent with a prospective investment-grade partner and later announced a $150M commitment tied to infrastructure buildout ahead of potential occupancy. However, that prospective tenant backed out of the construction agreement in December, sending the stock sharply lower and raising questions about the project’s near-term viability.

The identity of the tenant was never disclosed, though speculation around the IPO most frequently pointed to hyperscale cloud providers—particularly Microsoft or Oracle—given their rapidly expanding AI infrastructure needs.

English

🇨🇦 If you want to know a bit more about the Canadian #REIT, make sure to check out this conversation.

youtu.be/xk8pfMvrraI?si…

$CSH.UN $HR.UN $REI.UN $AP.UN

@HoyaCapital @DailyREITBeat

YouTube

English

Alreits Research retweetledi

Big day for Hoya Capital!

$RIET hit a major growth milestone, surpassing $100 Million in AUM!

@AllTheREITNews | @DailyREITBeat | @ReitAcademy | @Alreits | @REITs_Nareit

English

Alreits Research retweetledi

⭐ 2025 Real Estate Sector Returns ⭐

🟢 S&P 500: +17.7%

🟢 Equity REIT Index: +3.3%

🟢 Housing Index: +0.1%

2025 Property Sector Winners:

🟢 Senior Housing: +44.3%

🟢 Industrial: +22.0%

🟢 Billboard: +17.3%

🟢 Net Lease: +11.6%

2025 Property Sector Losers:

🔴 Farmland: -12.4%

🔴 Data Center: -14.2%

🔴 Cannabis: -14.9%

🔴 Cold Storage: -36.7%

@AllTheREITNews | @DailyREITBeat | @ReitAcademy | @Alreits | @REITs_Nareit | #REITs #Dividends #Investing #Income #Yield #RealEstate #Housing

English

Alreits Research retweetledi

📦EastGroup Properties (EGP) | Hoya Hotseat

EastGroup is the second-largest industrial REIT, owning and operating a portfolio of over 60 million square feet with a focus on 'last-mile' properties: one-story, shallow-bay infill distribution facilities.

These close-to-customer logistics facilities enable the company to capture demand from a diverse base of more than 1,400 tenants that rely on proximity to dense population centers for efficient delivery.

President & CEO Marshall Loeb joins the Hoya Hotseat to discuss the evolution of EastGroup since its initial founding in 1969 and the strategy and factors behind its impressive growth trajectory.

Loeb emphasizes the advantages of EastGroup’s focus on the "last mile" and its industry-leading balance sheet. Loeb also details the secular forces - both positive and negative - shaping fundamentals in the industrial real estate sector.

Full Interview & Transcript Here: seekingalpha.com/mp/1026-ireit-…

@EastGroupProp | @AllTheREITNews | @DailyREITBeat | @ReitAcademy | @Alreits | @REITs_Nareit | $EGP

English

Alreits Research retweetledi

💸 REITs Present a Compelling Buying Opportunity for Value-Focused Investors

As shoppers hunt for Black Friday bargains, investors may find their own version of “on sale” pricing in today’s REIT market.

📊 REITs = Strong Operations + Attractive Pricing: Public REITs continue to maintain occupancy rates equal to or higher than private real estate across most major property types.

🏬 Biggest occupancy advantages:

* Retail: +4.7%

* Office: +4.5%

* Apartments: +1.4%

🏭 Industrial remains tight: REIT industrial occupancy is essentially in line with private market levels (both >95%).

💰 REIT Cap Rates Offer “On Sale” Pricing vs. Private Real Estate

REIT implied cap rates exceed ODCE appraisal cap rates across all four major sectors:

* Apartments: +191 bps

* Office: +121 bps

* Industrial: +94 bps

* Retail: +79 bps

* Translation: REITs are priced more attractively than comparable private real estate — offering better value for the same property types.

🧭 Why This Matters

* REITs give investors access to high-quality, institutional-grade real estate.

* Operated by best-in-class management teams with scale, discipline, and transparency.

* Provide instant, diversified exposure across sectors and geographies.

* Combine stronger occupancy + more attractive pricing = a compelling entry point.

📌 Bottom Line: If you’re an investor who appreciates good value — especially in today’s market — REITs are offering a rare combination of quality, stability, and discounted pricing.

reit.com/news/blog/mark…

English

It’s live! Redeem the coupon code BF2025 by November 30th and enjoy 40% off our Premium subscription.

#REITs #Stocks #ETFs #Dividends

English

Top 5 Owned #REITs across all Alreits Portfolios:

1. $O 60.8%

2. $VICI 28.2%

3. $PLD 22.7%

4. $STAG 19%

5. $ARE 16.5%

English

If you invest in Self Storage #REITs, you have to watch the @wendoverpro video overview of the sector.

youtu.be/uEVv8SOJ6Is

$PSA $EXR $CUBE $SELF $SMA $NSA

YouTube

English

🇿🇦 The 1y performance of South African #REITs is not bad.

$RES.JO $GRT.JO $VKE.JO $FFB.JO $EQU.JO

English

Thanks @MoneySense for mentioning us in your recent article about REIT Investing in Canada.

moneysense.ca/save/investing…

English

Alreits Research retweetledi

🏙️ When The Stimulus Stops

Real Estate Weekly Outlook: seekingalpha.com/article/484101…

U.S. equity markets stumbled this week as stretched tech valuations collided with weakening consumer and labor market data, while the economic drag and uncertainty mount from the ongoing government shutdown.

Now it's real? The shutdown has now halted fiscal flows into several sizable government benefits programs - a sudden onset of fiscal austerity that could have non-trivial disinflationary impacts.

Snapping a three-week winning streak, the S&P 500 dipped 1.7%. REITs led as earnings season wrapped up with a handful of surprisingly solid reports from some unlikely leaders.

Hotel REITs rallied nearly 9% after a surprisingly solid slate of results showed favorable expense controls and resilient demand trends, particularly in the upscale segment, offsetting lower-tier softness.

Also among the leaders this week, Billboard REITs surged after results showed a surprising rebound in ad spending among national advertisers - particularly in the transit and digital format - offsetting some emerging softness in local ad spending trends.

@DailyREITBeat | @ReitAcademy | @Alreits | #retwit

English

Alreits Research retweetledi

🏥 CareTrust REIT Sets Up SHOP, Eyes Long-Term Growth Through Senior Living and UK Expansion

💬 CareTrust $CTRE CEO Dave Sedgwick: “Our sights are set on where we will be in 10-plus years and how we can grow in the next decade like we did in our first.”

⚙️ Three core growth engines:

* Skilled Nursing Facilities (SNFs) – the REIT’s historic foundation and “bread and butter.”

* Senior Housing Operating Portfolio (SHOP) – newly launched, targeting higher upside through active operations.

* United Kingdom expansion – following the $817M acquisition of Care REIT earlier this year.

* Goal: Replicate CTRE’s strong historical shareholder returns through diversification and operational scale.

🏗️ New SHOP Platform Takes Shape

* First SHOP deal expected to close by year-end 2025.

* CTRE has built the operational infrastructure to “grow and scale” its managed housing business.

* Why now: Long-term demographics, limited new supply, and a favorable entry point in senior housing economics.

🔄 Investment Activity

* $495M in Q3 and subsequent closings, bringing 2025 YTD investments to $1.6B — a record high.

* $600M pipeline expected to close over the next 12 months

* CIO James McCallister: “We’re seeing sustained deal flow across skilled nursing and senior housing — both triple-net and SHOP.”

🏦 Senior Housing Strategy

* Initial focus: Stabilized or moderately repositionable assets; avoids high-capex turnaround projects.

* Considers both stand-alone and campus-style communities.

* Will seek to expand relationships with existing operating partners following acquisitions.

* Balanced approach between cash-flow stability and operational upside.

🌍 UK Expansion Momentum

* $817M acquisition of Care REIT closed earlier in 2025 — includes 137 care homes across England, Scotland & Northern Ireland.

* First follow-on U.K. transaction closed in September.

🔮 2026 Outlook

* Three engines aligned for multi-year growth: SNF stability, SHOP ramp-up, and UK diversification.

* Deal pipeline “robust and scalable” with steady transaction volume across both sides of the Atlantic.

* CEO Sedgwick: “We expect to begin 2026 hungry — aggressively pursuing deals in all three target areas.”

* Positioned for sustained growth amid favorable demographics and limited new senior living supply.

💡 Key Takeaways

* Strategic transformation: CTRE adds a new growth vertical (SHOP) while maintaining core SNF strength.

* Diversification advantage: U.K. investments provide currency and market balance.

* Record deployment: $1.6B invested in 2025; pipeline supports strong 2026 start.

* Demographic tailwinds: Aging population and healthcare needs underpin long-term demand.

* Positioned for another decade of compounding growth through operational, geographic, and asset diversification.

mcknightsseniorliving.com/news/caretrust…

English

⚠️ 2 #REITs have reached 100% payout ratio after the Q3 2025 update yesterday:

- $NSA • Self Storage • 100.8% payout

alreits.com/reits/NSA

- $IIPR • Cannabis Facilities • 100.2% payout

alreits.com/reits/IIPR

English

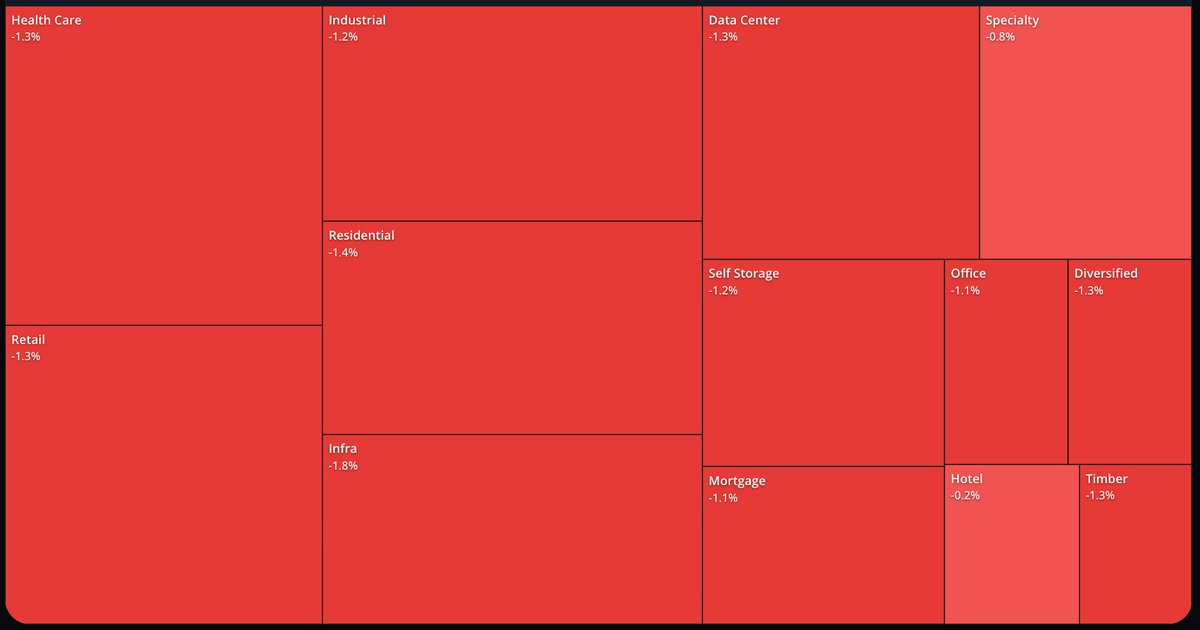

Performance Heatmap is coming 🟩🟥

Market cap-weighted heatmap for stocks, REITs, and ETFs integrated with our Screener - you control what to visualize and the timeframe.

@HoyaCapital @DivStockpile @DividendGrowth @ReitAcademy @askjussi

English

Alreits Research retweetledi

🏨 Sotherly Hotels Inc. (SOHO) to Be Acquired in $2.25/Share All-Cash Deal

Sotherly Hotels Inc. $SOHO entered a definitive merger agreement with a joint venture led by Kemmons Wilson Hospitality Partners (KWHP) and Ascendant Capital Partners. The JV entity, KW Kingfisher LLC, will acquire all outstanding Sotherly common shares for $2.25/share in cash.

🏆 Premium:

* +152.7% to SOHO’s Oct. 24 closing price

* +126.4% to the 30-day volume-weighted average price

* Valuation: Marks the highest premium paid for a public REIT in the past five years.

* Expected closing: Q1 2026, pending shareholder approval and customary conditions.

🔒 Financing:

* Debt commitments from Apollo (NYSE: APO) and Ascendant Capital Partners.

* Berkadia serving as sole financial advisor and financing arranger to KWHP.

🏨 Strategic Rationale & Leadership Commentary

* Andrew Sims, Chairman (SOHO): “This transaction delivers compelling, immediate, and certain cash value — the highest premium paid for any public REIT in five years.”

* David Folsom, CEO (SOHO): “It’s a testament to the high-quality portfolio we’ve built across the Southeast over the past 20 years.”

* Webb Wilson, CIO (KWHP): “Sotherly’s distinctive Southeastern portfolio aligns perfectly with our hospitality heritage and growth focus.”

* Alex Halpern, CIO (Ascendant): “We bring deep hotel operating expertise and hybrid financing solutions to support these irreplaceable assets.”

🧱 Portfolio Snapshot

* 10 full-service upscale and upper-upscale hotels

* Located across 7 states

* 2,786 total rooms, plus interests in two condo hotels

* Focus: Mid-Atlantic and Southeastern U.S.

📊 Preferred Stock Treatment

* Holders of Sotherly’s Series B, C, and D Preferred Shares may elect to convert into common shares and receive the $2.25/share cash consideration, subject to charter terms.

* If not converted, preferred shares will remain outstanding under current terms.

📈 Investor Takeaway

* Sotherly shareholders receive an immediate cash exit at a >150% premium, highlighting strong private-market demand for high-quality, Southeastern hotel portfolios.

* KWHP & Ascendant gain a strategically located hospitality platform amid a favorable post-pandemic recovery in leisure and business travel.

* SOHO will no longer host earnings calls or issue separate Q3 results as the merger process moves forward.

investors.sotherlyhotels.com/financial-info…

English