Life goes so fast if you spend all of it obsessing over numbers and money

You have to take time for you, your family and achieve things outside of just finances

Else you miss the whole point

Pompliano just posted the Bitcoin hedge thesis again.

Mark Cuban sold most of his BTC the same week.

Both of them are missing the more important question.

Here is what the data actually says.

The Pompliano thesis:

Dollar debasement drives asset inflation.

Asset inflation destroys savings.

Destroyed savings radicalizes the middle class.

Radicalized middle class elects socialist governments.

Socialist governments default.

Default destroys dollar-denominated assets.

Gold and Bitcoin survive.

It is a clean logical chain.

The problem is the evidence does not fully support it yet.

The Mark Cuban counter:

Cuban endorsed Bitcoin as an inflation hedge aggressively.

Then watched it underperform during the exact macro stress event it was supposed to protect against.

During tariff-induced dollar strength last year, Bitcoin fell harder than gold.

He sold.

And he is not entirely wrong to question the thesis.

Bitcoin underperformed gold when the dollar barely moved over the last 12 months.

The hedge narrative has a timing problem.

But here is what Cuban missed:

Since the Iran conflict began in late February, Bitcoin has outpaced gold.

Not slightly. Meaningfully.

The same asset that failed as a tariff hedge became the stronger performer during a genuine geopolitical crisis.

That inconsistency is not a bug in the Bitcoin thesis.

It is the most important data point in understanding what Bitcoin actually hedges against.

What Bitcoin actually protects against:

Bitcoin does not hedge inflation in the traditional sense.

It does not move inversely to CPI like gold historically has.

What it hedges is systemic trust collapse.

Tariffs are a policy tool. They are inflationary but they operate within the existing system.

Geopolitical conflict at scale — wars, sanctions, currency weaponization, sovereign debt stress — that is a systemic trust event.

Bitcoin outperforms gold in systemic stress because it is the only asset that is simultaneously:

Stateless. Cannot be frozen by a government.

Borderless. Moves across jurisdictions instantly.

Finite. 21 million hard cap with no committee vote required to change it.

Verifiable. Anyone with internet access can audit the full supply.

Gold has most of these properties but not all of them.

You cannot move $10 million in gold across a border in 10 minutes.

You can move $10 million in Bitcoin in under a minute for less than a dollar.

Now connect this to this week:

Russia is liquidating gold reserves and testing XRP for energy settlement.

Iran launched a Bitcoin-based maritime insurance platform to bypass sanctions.

Moody's just rated the first Bitcoin-backed bond in U.S. history.

These are not retail speculations.

These are nation-states and credit agencies treating Bitcoin and crypto infrastructure as operational financial tools under real systemic pressure.

Pompliano's thesis is not wrong.

It is just early.

The sequence he describes — debasement, inflation, radicalization, default — plays out over years, not quarters.

The signal that it is beginning is not a price move.

It is behavior.

Sanctioned nations moving to Bitcoin and XRP for settlement.

Governments filing crypto positions with the SEC.

Credit agencies rating Bitcoin-collateralized debt.

Institutional ETF inflows at record levels during a price drawdown.

That is the behavior of a world that is quietly beginning to price in exactly the scenario Pompliano described.

My read:

Cuban sold because Bitcoin failed the short-term inflation hedge test.

But Bitcoin was never designed for short-term inflation hedging.

It was designed for the scenario where the system itself stops being trustworthy.

Gold at $4,529 an ounce.

Bitcoin at $76,776.

Both are telling you something about the dollar.

The question is not which one to hold.

The question is whether you believe the system is structurally sound.

If you do, neither matters.

If you do not, both do.

Russia just sold 900,000 ounces of gold in four months.

The same country that spent a decade accumulating gold as a sanctions buffer is now liquidating it.

And simultaneously testing XRP as its settlement infrastructure.

That combination tells you everything about where global finance is heading.

Here is what is actually happening.

The gold drawdown:

The Bank of Russia reduced its gold holdings by roughly 900,000 ounces in the first four months of 2026.

Total reserves are now down to approximately 73.9 million ounces — the lowest level since early 2022.

This is not a routine portfolio adjustment.

Russia accumulated gold for years specifically because it is a liquid, non-sovereign asset that cannot be frozen, blocked, or sanctioned.

It was their financial backstop of last resort.

Selling it at this pace means one thing: the fiscal pressure from sustained military expenditure and sanctions is now larger than the insurance value of holding the reserve.

The gold is being spent. Not rotated. Spent.

The XRP pivot:

While gold reserves are being trimmed, the Moscow Exchange has been expanding its range of crypto-linked instruments — including XRP indices and futures products.

This is not coincidental timing.

The strategic problem Russia faces is not demand for its oil exports.

China and India are buying Russian crude.

The problem is settlement.

SWIFT is inaccessible. Correspondent banking networks are compromised. Dollar clearing mechanisms are a sanctions vector.

Every traditional payment route for high-volume energy trade runs through infrastructure that Western governments can switch off.

XRP was designed for exactly this problem.

Fast cross-border liquidity. Settlement in seconds. Minimal cost. No dependency on legacy banking intermediaries.

For a country moving billions in energy payments to BRICS partners every month, those are not ideological selling points.

They are operational requirements.

The layered strategy:

What Russia is building is not a single alternative. It is a stack.

Gold sales covering immediate fiscal gaps.

XRP-linked infrastructure testing for settlement rails.

Reduced exposure to sanction-prone financial systems.

Deepened trade channels with BRICS-aligned economies.

Each layer addresses a different vulnerability.

Russia is testing XRP for energy settlement outside SWIFT.

Two of the most heavily sanctioned nations on earth are independently converging on the same conclusion:

Blockchain infrastructure is the only settlement layer that cannot be politically frozen.

They are not doing this because they believe in decentralization.

They are doing this because they have no other option.

What this means for XRP specifically:

The XRP narrative has always been about cross-border payments and institutional settlement.

That narrative is now being tested in one of the highest-stakes real-world environments that exists — sanctioned commodity trade between major economies.

Italy's largest bank added XRP to its balance sheet this quarter.

The Moscow Exchange is expanding XRP instruments while the country restructures its reserve strategy.

Trump's executive order this week opened the door for XRP-linked infrastructure to access the U.S. Federal Reserve payment system.

My read:

Russia is not fully committing to XRP. This is an experiment, not a declaration.

But sanctioned economies experimenting with XRP for energy settlement is a more powerful real-world stress test than any institutional pilot program.

If it works at scale for Russian oil payments, every other sanctioned economy on earth takes notice.

Gold was the last century’s neutral reserve asset

The next one is being decided right now

Do me a favour and follow this we need 50 followers to go live

@blocksandbantershow?si=mVdGdNzX8EE-IYw6" target="_blank" rel="nofollow noopener">youtube.com/@blocksandbant…

Moody's just rated a Bitcoin-backed bond.

Let that sentence land for a second.

The same agency that rates sovereign debt, corporate bonds, and mortgage securities just assigned a formal credit rating to a structure where Bitcoin is the collateral.

This is not a crypto story. It is a credit markets story.

Here is exactly what happened and why it matters more than the headline suggests.

The structure:

The bonds are issued through the Business Finance Authority of the State of New Hampshire — a government authority — and backed by a loan secured with Bitcoin.

The deal is worth up to $100 million.

Moody's assigned it a Ba2 provisional rating.

Custody of the Bitcoin collateral is handled by BitGo.

A separate agent is responsible for selling the Bitcoin if needed to meet payments.

Investors are repaid from the value of the collateral — not from taxpayer funds.

That last part is critical. This is not government-backed. It is Bitcoin-backed.

The safety mechanism:

The initial collateral ratio is set at 1.6 times the loan value.

If it falls to 1.4, the bonds must be redeemed.

That means the structure forces liquidation before the collateral becomes insufficient.

It is not a bet that Bitcoin stays flat. It is a structure designed to survive Bitcoin's volatility while still functioning inside traditional credit markets.

One tranche also benefits if Bitcoin's price rises — adding upside on top of fixed returns.

A bond with Bitcoin downside protection and Bitcoin upside participation.

That is a new instrument class.

Why Moody's rating changes everything:

Most institutional capital cannot touch an asset without a credit rating.

Pension funds, insurance companies, endowments, and family offices all operate under mandates that require rated instruments.

Bitcoin itself cannot be rated. It has no cash flows, no issuer, no maturity.

But a structured product backed by Bitcoin — with defined collateral ratios, custody arrangements, and liquidation triggers — can be.

Moody's just opened the door for institutional capital that was previously locked out of Bitcoin exposure entirely.

Not through an ETF. Not through a futures product.

Through the oldest and most trusted instrument in traditional finance.

A bond.

The bigger pattern:

Italy's largest bank filed $235 million in ETH and XRP holdings with the SEC.

37 European banks are building a euro stablecoin through Qivalis.

BlackRock, Visa, and JPMorgan are building directly on Solana's infrastructure.

Strategy holds 818,869 BTC and is preparing another purchase.

And now Moody's has rated the first Bitcoin-backed bond in U.S. history.

These are not isolated events.

This is the traditional financial system methodically building the infrastructure to hold, settle, and finance Bitcoin at institutional scale.

The retail narrative is focused on price.

The institutional narrative is focused on structure.

Structure always precedes price.

My read:

The Ba2 rating reflects real risk — Bitcoin's volatility, reliance on market liquidity, and the speed required to liquidate collateral if conditions deteriorate.

Those risks are real and should not be dismissed.

But the fact that Moody's modeled those risks, stress-tested the structure, and assigned a rating at all is the signal.

Six years ago, no credit agency would touch a Bitcoin-backed instrument.

Today, one just did.

That process — once it starts — does not reverse.

SOL is down 72% from its peak.

BlackRock, Visa, and JPMorgan are all building on it anyway.

That disconnect is the most important signal in crypto right now.

Here is what the charts and the fundamentals are saying at the same time.

The institutional moves:

BlackRock — managing over $10 trillion in assets — has expanded its tokenized fund operations directly onto Solana's mainnet. The reason cited internally is sub-second finality and fees that cost fractions of a cent.

Visa has graduated its USDC settlement pilot on Solana from testing into production-grade infrastructure. That is not an experiment anymore. That is live payment rails.

JPMorgan's blockchain division has been stress-testing Solana's throughput for cross-border payment corridors — and has acknowledged that Solana's settlement efficiency exceeds what its own proprietary Onyx network can currently match.

Three of the largest financial institutions on earth looked at every option and chose Solana's infrastructure.

While the token was in a downtrend.

The chart structure right now:

SOL closed the week at $82.11 — down 72% from its $295 cycle peak.

The Parabolic SAR sits at $181.99. The weekly downtrend is structurally intact.

But the MACD histogram is compressing week over week. Selling momentum is exhausting itself.

The SOL/BTC pair is sitting at 0.00110 BTC — hugging the lower Bollinger Band.

The 14-period RSI on SOL/BTC is at 34.55.

That level has been touched exactly twice before in Solana's weekly history.

Both times preceded multi-hundred-percent recoveries.

The divergence that matters:

Solana's DeFi TVL has stabilized even as price has fallen.

The ecosystem now has over 400 active dApps.

This is the same setup as early 2023 — infrastructure holding, price lagging — just before SOL ran 900% off its bear market floor.

The institutions are not waiting for a price recovery.

They are building the infrastructure that makes one inevitable.

My read:

The market is pricing Solana like a token in decline.

Three of the largest capital allocators on earth are treating it like a settlement layer they cannot afford to ignore.

One of those views is going to be wrong.

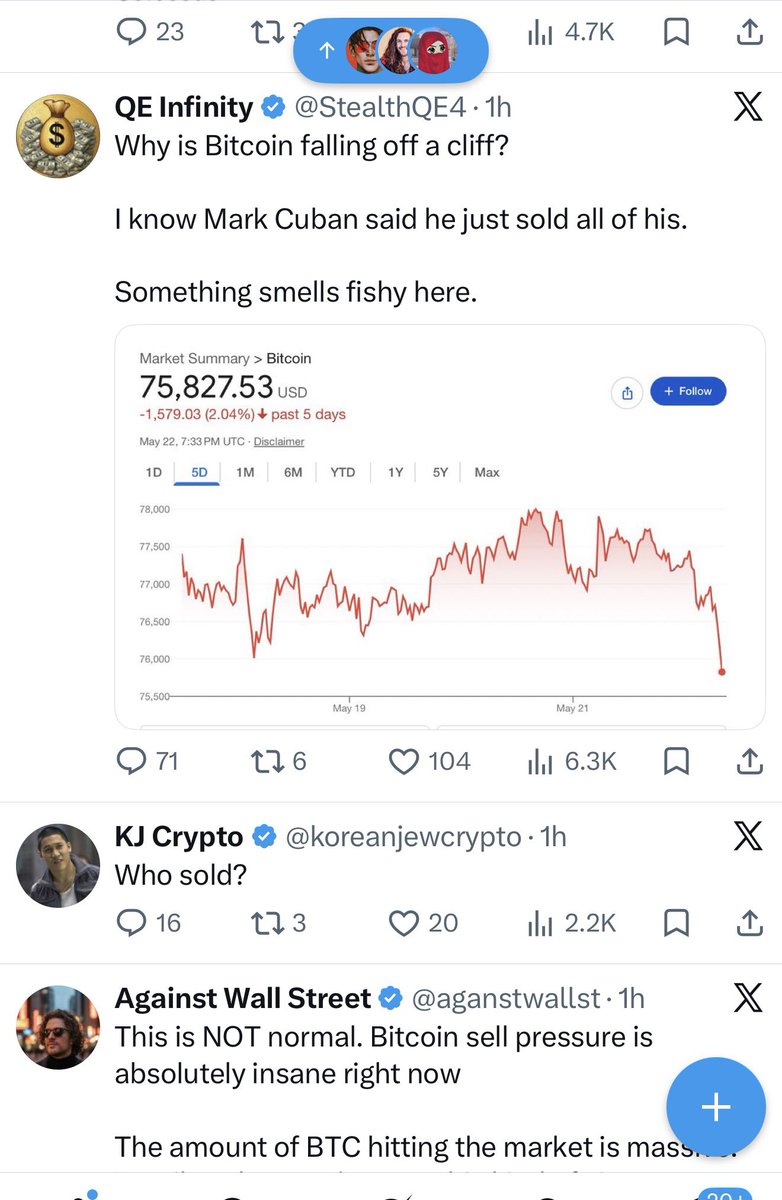

This is NOT normal. Bitcoin sell pressure is absolutely insane right now

The amount of BTC hitting the market is massive. Retail traders can’t move this kind of size

Only ETFs and large institutions are capable of selling this much Bitcoin

What’s going on?

bitcoin:native $MSTR

Seeing this all over the TL. If your favorite KOL doesn’t know what happened or is spinning conspiracy theories they don’t deserve your attention. Facts over fear.