Alexander

2.4K posts

Alexander

@ApolloPerforms

Fitness Business Owner. Accredited Investor. Detached from all ideologies. Connoisseur of emerging markets.

Illinois, USA Katılım Temmuz 2020

910 Takip Edilen582 Takipçiler

@joeroganhq This is accurate. In 2016, his total testosterone was measured in the mid 400s on exam. This is documented. It's pretty decent for a guy that is out of shape and sleeps 3 hours a night. You'd expect that level for a 40 y/o.

English

RFK Jr: "Oz looked at Trump's records and said Trump has the highest testosterone he's seen for someone over 70."

English

@HouseCracka @MisyDP No, this would only work in Florida, California or somewhere similar.

English

@ApolloPerforms @MisyDP Winter in Chicago and this business? 🤣

English

HK and ADR almost never have the same price, usually the HK listing is a few dollars lower.

$BABA retraced all the way to the $120 breakout that took years to get past and turned it into support. The chinese AI story is brewing in the background. The Iran situation made the dollar squeeze which put pressure on emerging markets. Give the technicals some time to play out. Likely back to accumulation - just have to wait for expansion.

I see very little downside risk at the $120 level from a technical and fundamental level.

English

@ApolloPerforms This isn’t hood overnight, it is tracking HK 9988 and it’s below US close. It’s only above HK close (for now anyways, give it time)

My point is that the HK session will sell any gains from the US session - stay away

English

$BABA wowee you’ll never guess what happened on HK open

Why would you buy this stuff

Dave@eose_bull

$BABA Again - why are you buying this stock when Asian investors will do this immediately when they start trading lmao KWEB new lows incoming

English

Alexander retweetledi

Alexander retweetledi

Alexander retweetledi

BRAZIL'S LULA SAYS "TODAY, MY TRADE WITH CHINA IS TWICE AS LARGE AS MY TRADE WITH THE UNITED STATES. AND THAT IS NOT BRAZIL’S PREFERENCE"

English

Alexander retweetledi

Alexander retweetledi

$MELI's CFO just brought even more clarity to the Q1 results on the investor relations podcast. This team is so honest and upfront about what they are doing. Really don't know any other team like them.

The market is likely worried over a drop in profit margins for the consumer credit business in Brazil for $MELI. To some this looks like a warning sign of bad debt. Mercado Libre is experiencing accounting effects from strategic growth. They accelerated loan originations by 25% QoQ in the first quarter. Accounting rules require them to record all estimated future losses on day one before the revenue arrives. They also extended loan terms from 5 to 8 months for their best borrowers. This is just for the consumer loans. This has nothing to do with the credit cards. They also lowered interest rates to activate safe users who had never used their credit lines. The actual bad debt levels, or non-performing loans, remain stable. The margin compression is a temporary accounting reality of rapid growth, not a fundamental credit problem. The key message from the perspectives is that MELI is not seeking out riskier folks to offer lower spreads. They are reaching out to folks they deemed worthy of credit in the past and did not bite. The lower spreads along with the high duration are there to entice those that did not bite in the past.

Investors often worry when a company lowers prices or gives away shipping. Mercado Libre lowered its free shipping minimum from 79 reais to 19 reais last year in Brazil. On the surface, this looks like a direct hit to profit margins. Instead, it created immense scale. The growth rate of items sold jumped from 26% to 56%. Because the company is shipping significantly more items, their cost to ship each individual unit dropped by 17%. The profitability of cheaper items actually improved. The company traded a small amount of short-term margin for massive volume, which permanently lowered their fixed fulfillment costs per item.

Traditional banks in Argentina are seeing high default rates. Mercado Libre is seeing the exact opposite. Their non-performing loans in Argentina are stable YoY and improved in the first quarter during a time of wide-spread credit stress. Their NIMAL improved by 6%. This happens because users treat Mercado Pago as their primary financial tool. People protect their Mercado Libre credit line and prioritize paying it back over other debts. The company also purposely slowed down loan growth in Argentina to 13% to maintain this high portfolio quality. They demonstrate a structural collection advantage over traditional banks in difficult macroeconomic environments.

MELI is also spending heavily to issue new credit cards in Brazil, Mexico, and Argentina. The market often views credit card expansion as an expensive, high-risk customer acquisition cost. But folks miss that it is an ecosystem multiplier. The oldest groups of credit card users in Brazil are already profitable. The credit card users in Mexico are performing even better than Brazil after two years! Once a user gets a Mercado Pago credit card, they buy more items on the e-commerce marketplace. They also use more fintech products. The initial investment to issue the card creates a much more permanent, highly engaged user across both the commerce and financial halves of the business.

Martin also confirmed that both the cross-border business and the 1P operations are currently unprofitable and acting as a drag on overall profit margins. The market may view these depressed margins as a permanent structural flaw or a sign of inefficiency. However, he noted they are seeing clear progress and explicitly stated both segments will eventually become profitable. As the 1P and cross-border divisions continue to scale and cross their break-even points, they will transition from actively hurting margins to potentially expanding them, creating a built-in catalyst for future profitability without requiring broader cost-cutting measures. The other aspect is that as cross-border operations and 1P operations scale they will have a very similar multiplier effect like the credit cards. In fact, they could likely remain a loss-leader forever and probably still have a net-positive effect on the entire ecosystem. That is largely MELI's biggest structural strength. It is optimizing the ecosystem rather than any particular segment of operations.

English

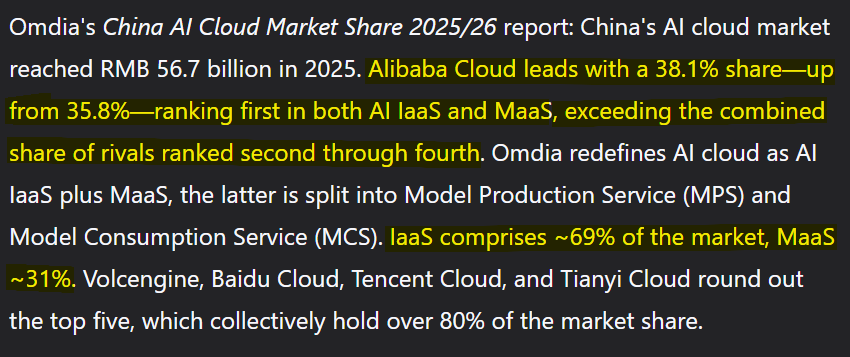

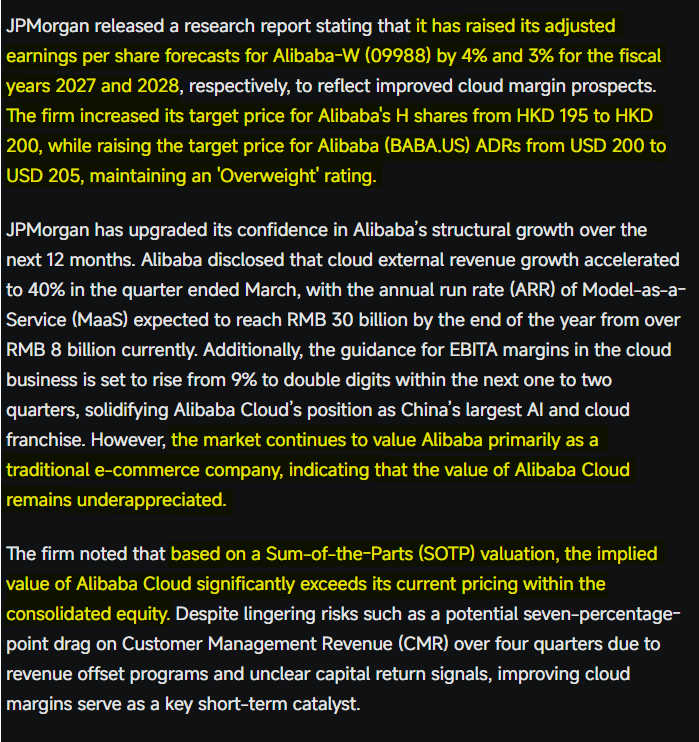

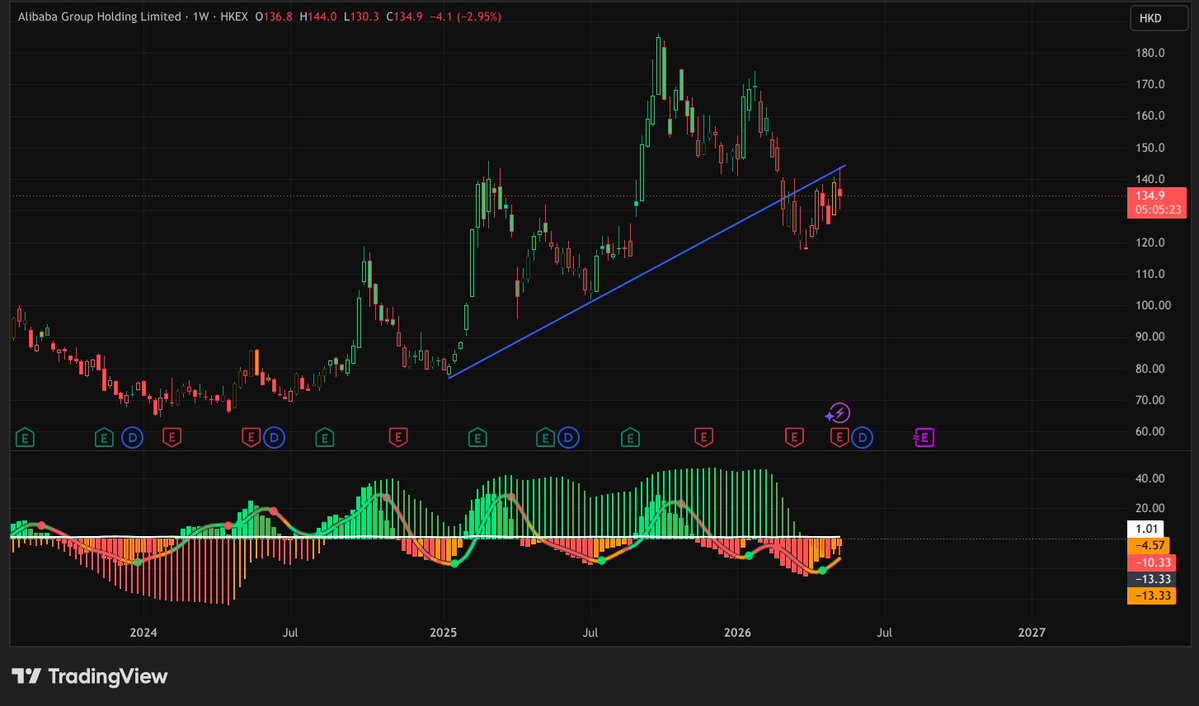

$BABA

Chart is of the 9988 HK listing.

Breakout hit resistance at that $147 level. May need a few attempts to breakthrough this overhead resistance line. Let's get through OPEX and see where we're at.

If we get past this level and reclaim the medium-term uptrend, it will be mega bullish. Longer term uptrend still remains intact when we retested the breakout at $120 and popped.

English