Sabitlenmiş Tweet

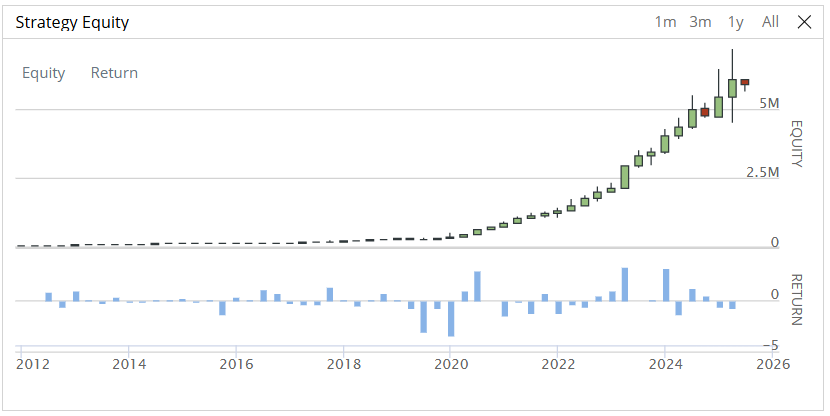

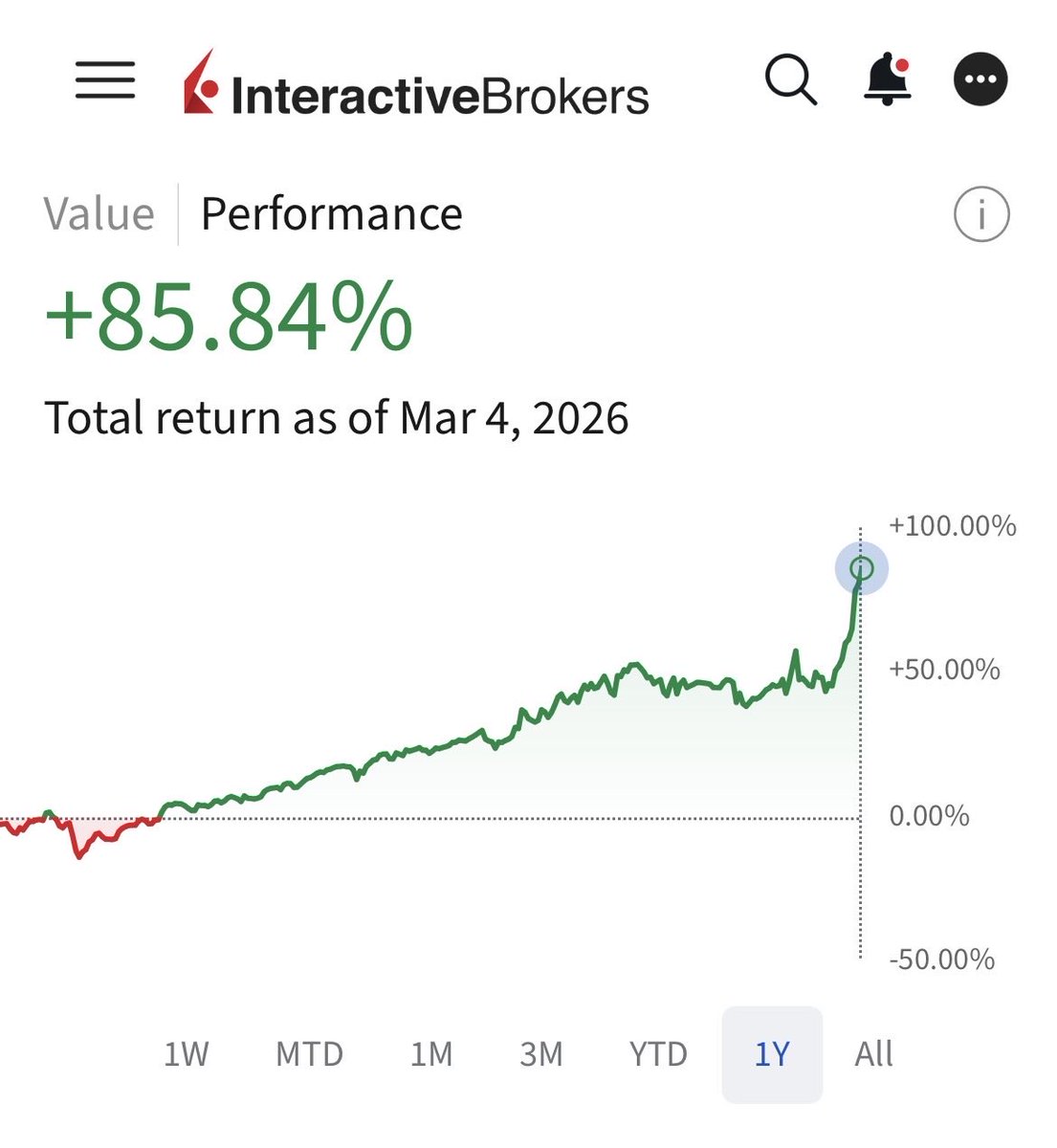

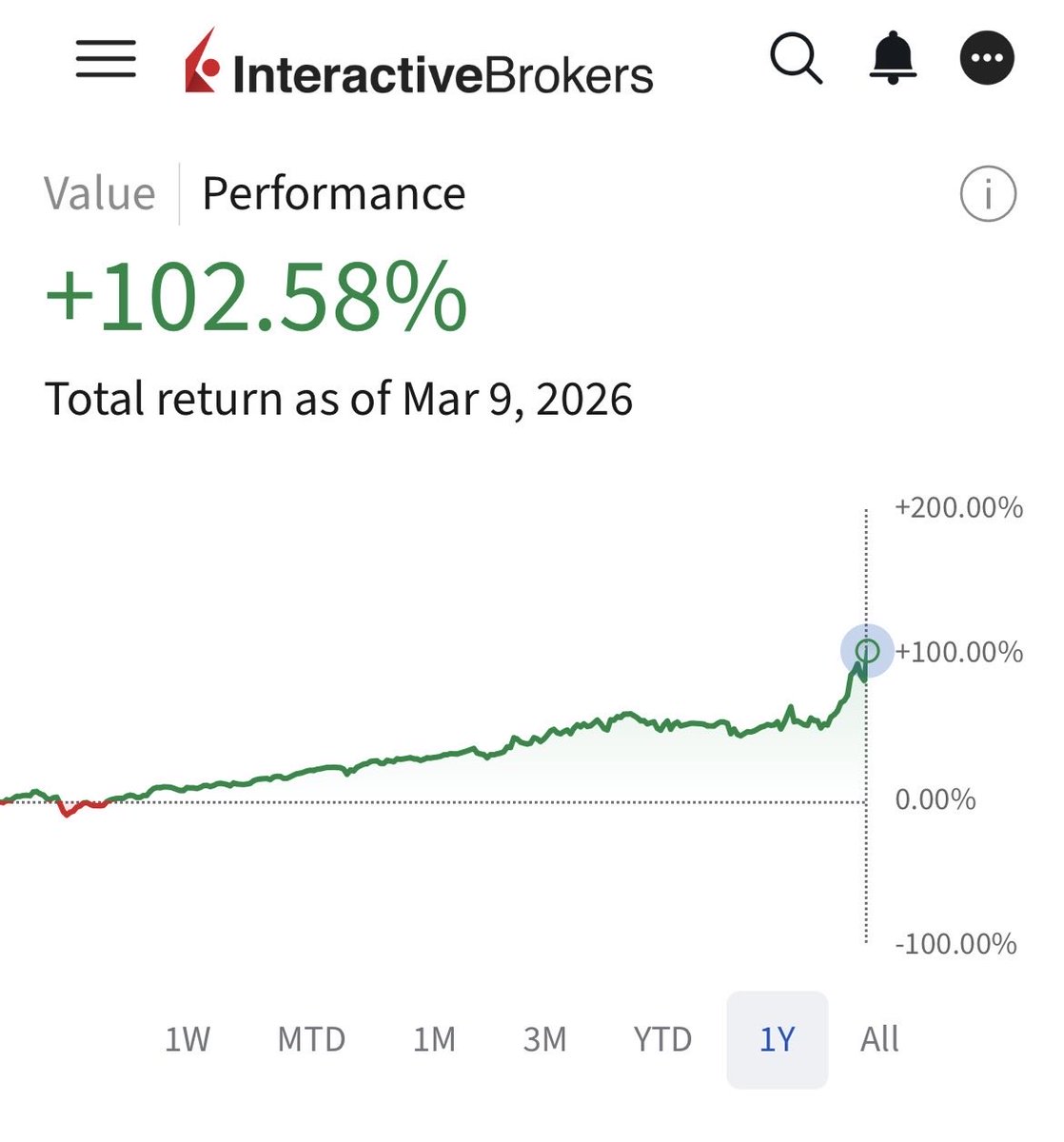

One more short thread while the equity keeps on climbing (so far 35% ytd). There seems to be this misconception that because big institutions can barely beat the market the same must be true for retail. After 16 years of trading I can comfortably disagree and here’s why..

English