BioDaddy76

88 posts

BioDaddy76

@BioDaddy76

Plan B is to just keep on givin’r

Houston, TX Katılım Ağustos 2021

72 Takip Edilen80 Takipçiler

Probably my last #RollCall as I’m taking a new position at JPMorgan Chase’s Leveraged Finance division….#IYKYK

#45z #RenewableDiesel #Biodiesel #Soybeans #SoybeanOil #Canola #CanolaOil #Rins #LCFS #Ethanol #RFS #OATT #OOAT #RFS

English

There is two kinds of traders in this market

The ones that own RINs

And the ones who are sad

English

@BioDaddy76 noooo... I would never be cynical especially about the Taco man

English

Friday: Trump announced "completely open for business

24 ships headed toward the strait. Most turned around.

Saturday: Iran closed it Said the US blockade violated the ceasefire

Sunday: US Navy seized an Iranian ship

This is not a negotiation. It's a traffic light nobody controls

English

RIN buyers do not like to have to pay the new highs

Dog bites boy

RIN goes up

Better get used to it 2026 is the new 2013!

English

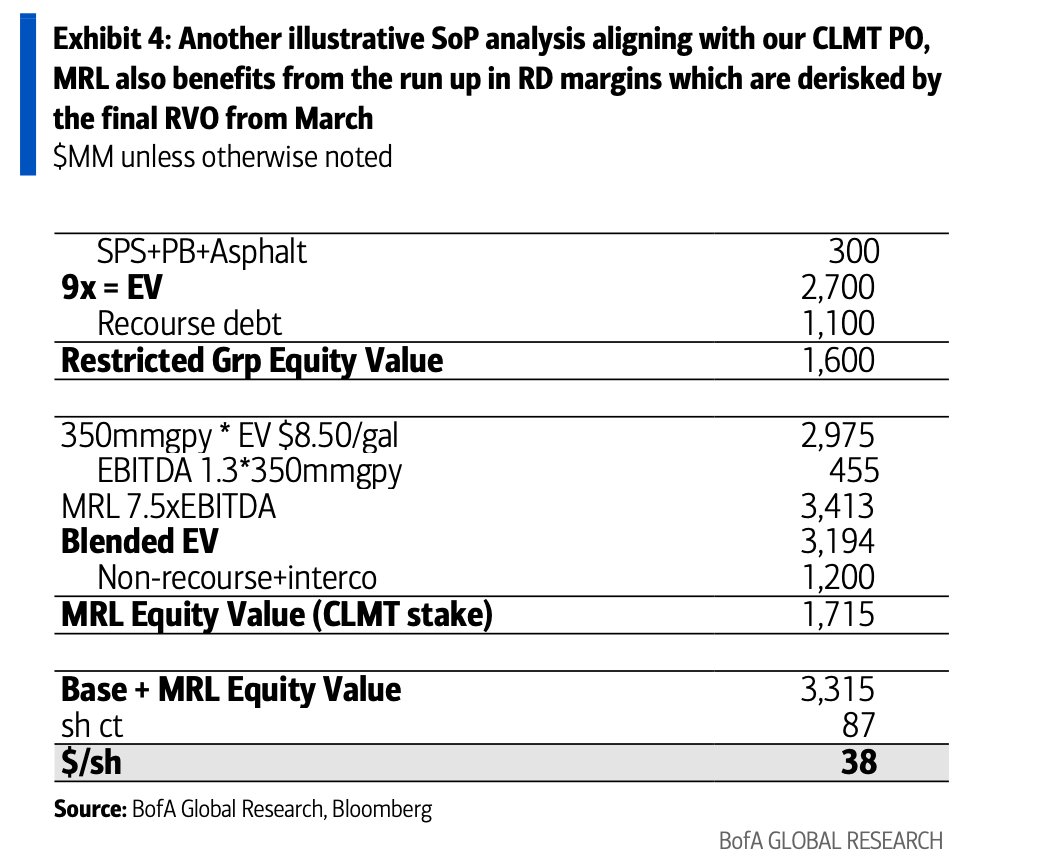

BoFA's sum of the parts analysis is also extremely flawed.

1) I am 100% aligned w/ $2.7B EV @ Restricted group.

2) I am 100% not aligned with MRL valuation construct. The analyst is taking a blended EV value of A) $8.50/gal replacement value + B) 350M full project gallons x $1.30 EBITDA/gal x 7.5 multiple.

Critical Issues:

1) MRL will not build 350 million gallons. They'll most likely stop with the 2nd reactor capacity which gets them 250 million gallons (220M gals SAF + 30M gals RD)

2) BofA's $1.30/gal EBITDA is too low. Why? $2/gal RD index margin less $0.40/gal fixed opex less $0.25/gal of transportation = $1.35 EBITDA/gal on RD gallons. The analyst is missing the $1+ SAF premium that is stacked ***ONTOP OF RD.***

English

$CLMT new BofA note: Raising PT to $38. The context is good, but the SOTP valuation math is absolutely wrong.

"Market margin gains in recent weeks at Montana Renewables, DGD, and Feed

Ingredients all support higher sum of parts and DCF value for DAR and CLMT, which is

the basis of our PO raises. in terms of quarterly results, catalysts for margin inflection

are 2Q26 for DGD as timing headwinds roll off, and 3Q26 for MRL as MaxSAF build-

related tpt headwinds roll off. We also reiterate that feed commod price gains—

benefitting Feed Ingredients—are in earlier innings since BD tpt appears to not yet have

reacted to the Final RVO’s increase in RINs demand. Moreover, relative feed prices imply

little supply stress so far as vegoils average near FOGs, whereas at full sectorwide

capacity the addressable market for vegoil is significantly larger than for FOGs due to

the scarcity of pretreatment capacity and fuel spec issues for FOG-based biodiesel.

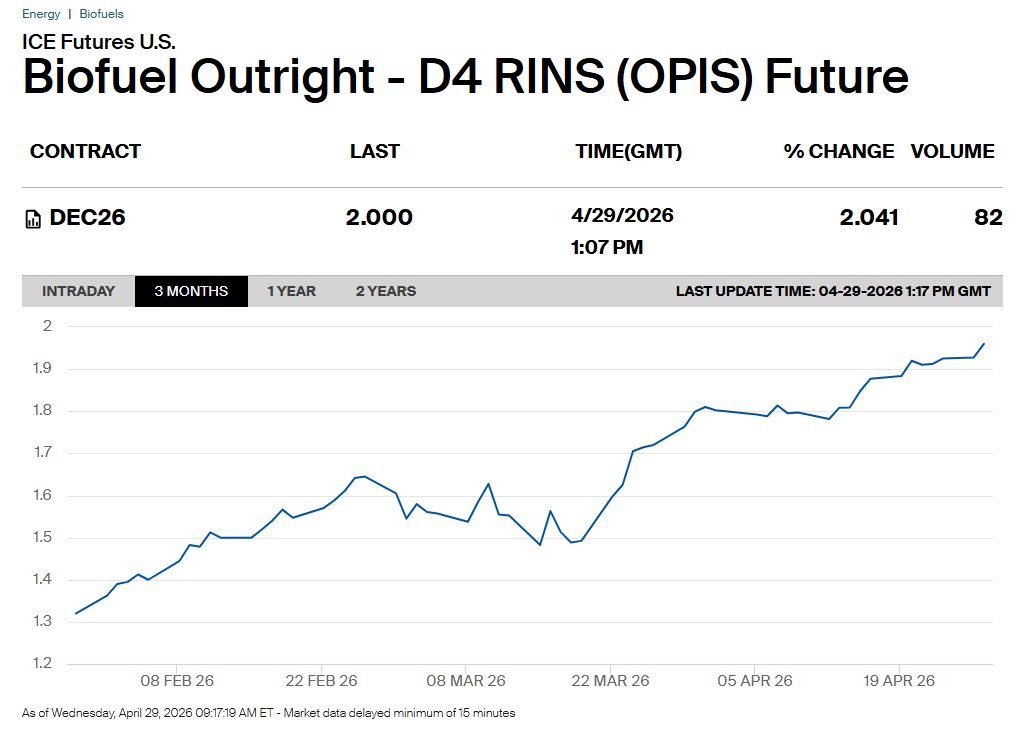

In March, RVO growth finalized, D4 RIN averaged $1.60,

and 500mm-RIN deficits per mo; BD ramping only slowly

In March, all signals in the RINs market pointed to an extremely tight market: a final D4

(BBD) RVO that grows >60% y/y in 2026, 500 million-RIN deficits per month on average

YTD for categories D4 thru D6 (our ests based on the y/y blend rate step up), and a

$1.60 average RIN price. To balance the RINs market, the entire BBD market’s

production capacity needs to run full, including biodiesel (and even that is likely not

enough). Market tightness has culminated in a ~$0.50/gal BD EBITDA margin (or

$20/bbl) at the high end of the cost curve (our est), and yet BD utilization rates have

been relatively slow to respond (+26% m/m)—slower than the RD util reaction to rising

margins (43% m/m; partly recovery from TAR), despite BD being well off 5-yr peak rates.

It is possible that marginal BD operators have been deferring ramp-up until after a

favorable RVO has been finalized, but for some marginal operators it seems likely that

margins may need to run even higher from here for BD operators to decide to run full or

restart idled capacity to achieve historical peak rates. DGD margins under similar

historical cost of supply regimes support this; back in 2018-2022, when, like today,

supply from small BD plants were needed to balance the market, DGD EBITDA/gal

averaged about $2.00, vs our $1.10-1.20/gal forecast based using an itemized cost stack

est in 2026. In sum, we think our RD mgn estimates are well-anchored on quantifiable

marginal supply cost of BD, but they could prove conservative if it ends up that ratably

higher BD mgns are needed to fill capacity."

English

@BioDaddy76 Elon makes LCFS credits at his charging stations, did you know that? When you combine that with the whole spaceX thing, you realize he was always 10 steps ahead of you.

English

A little while ago I bought stock in RocketLab (RKLB). One reason it will go up, the other is rockets go to moon which is where you will need to go to get your RINs in the future

English

Biodiesel has blending limits in many regions. Europe is well supplied as a result. Thus it needs to go to US or other regions (Indonesia, Malaysia, US, Canada).

Oddly enough if elevated diesel prices cannibalize demand it’s bad for biodiesel in some areas that are limited to 5% blend caps.

One solution is to raise blend thresholds in warm climates, yet there tend to be technological feasibility requirements. For reference, Indo is at B40 and considering B50. Brazil is considering B16. Meanwhile much of Europe and US is B5.

English

The moderator trying to calm everyone down asks “sir, if I may, what is your name!?”

The man gets up to walk out of the room and looks at the moderator one last time and says

“BIODADDY”

And walks out leaving the hall with what left to consider

English

Near the end the moderator asked the group if they had any other thoughts. A man at the back simply called out

“RINs”

English

Our latest on marginal RIN economics:

US biofuel quotas for 2026-27 indicate net exports of biomass-based diesel need to flip to net imports into 2027, yet our analysis of ship traffic at 11 global export hubs suggests flows are still funneling into Europe. This could push D4 RIN prices toward $2.15 vs. $1.78 in mid-April to spark biodiesel restarts and overcome tax-credit monetization challenges.

(Link to note 👇)

Brett Gibbs@OilandGibbs

In the wake of 2026-27 RVOs, what do you want to turn to next?

English