Sabitlenmiş Tweet

Bleap

2.8K posts

Bleap

@BleapApp

The future of finance. Powered by @arbitrum

Spend, save & trade smarter → Katılım Ağustos 2023

836 Takip Edilen14.1K Takipçiler

JUST IN: $100,000,000 worth of crypto shorts liquidated in the past 60 minutes.

English

Bleap retweetledi

🌟 NEW Pragma Lisbon speaker announced:

@JoaoAlvesDotETH, Co-founder of @BleapApp

July 25 • Pavilhão Carlos Lopes 🇵🇹

ethglob.al/HKRXP56HKA

English

This July, our co-founder and CEO João Alves will be speaking at @ETHGlobal’s Pragma Lisbon, sharing what we’ve been building at @BleapApp

we hope to see some of you there

English

English

@Heinrichlio @Defi_Warhol @Revolut @BleapApp We're just honest. Bleap is a great crypto card and more people should know about them

English

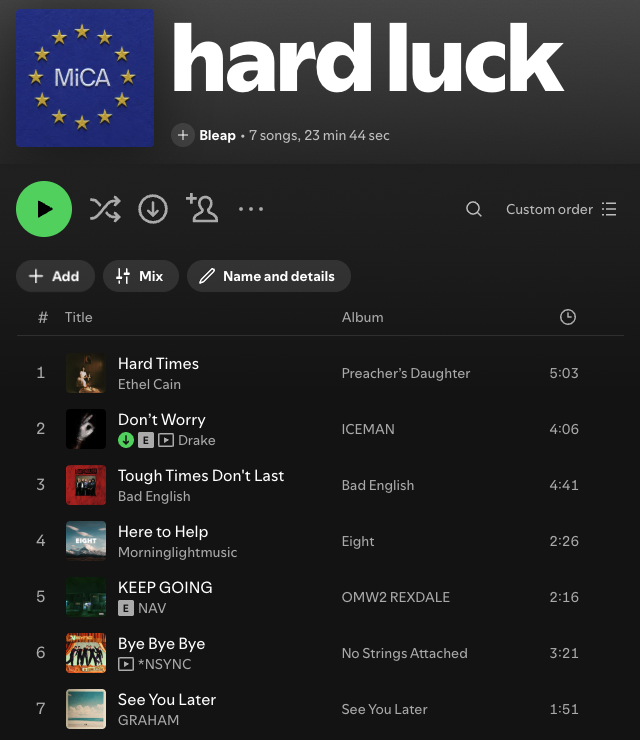

Almost no crypto card in Europe is MiCA-compliant yet.

Almost all of the crypto cards right now offer half-solutions and regulatory workarounds.

I ranked them from strongest to weakest compliance setup (for now)

↓

1/ @Revolut crypto

Only MiCA-compliant card on this list | full KYC | EEA coverage | bank transfer support

2/ @wirexapp

Full KYC | bank transfer support | MiCA application in progress

3/ @MetaMask Card

Full KYC | EEA + UK + Switzerland | regulated payment partners

4/ @Karta_Personal

Full KYC | bank transfer support | broad European availability

5/ @xplaceapp

Full KYC | bank + crypto funding | less public regulatory clarity

6/ @itstuyo

Full KYC | European availability | mostly crypto-funded

7/ @coca_card

Broad Europe + UK availability | bank funding | lighter KYC

8/ @RedotPay

Full KYC | fragmented European availability | weaker EU clarity

9/ @KASTxyz

Full KYC | bank funding | less EU regulatory clarity

10/ @Plasma One

Full KYC | limited availability | European coverage unclear

English

@BleapApp Bold claim from the intern :)

He/she is so humble.

English

@defyneric @KASTxyz @avici @RedotPay @ether_fi @wirexapp @payy_link @coca_card @itstuyo @holyheld @XMoney @ready_co @KoloHub @Plasma @useTria @gnosispay @Cypher_HQ_ @Karta_Personal @phantom nice

now can you do one with those who have a MiCA license

English

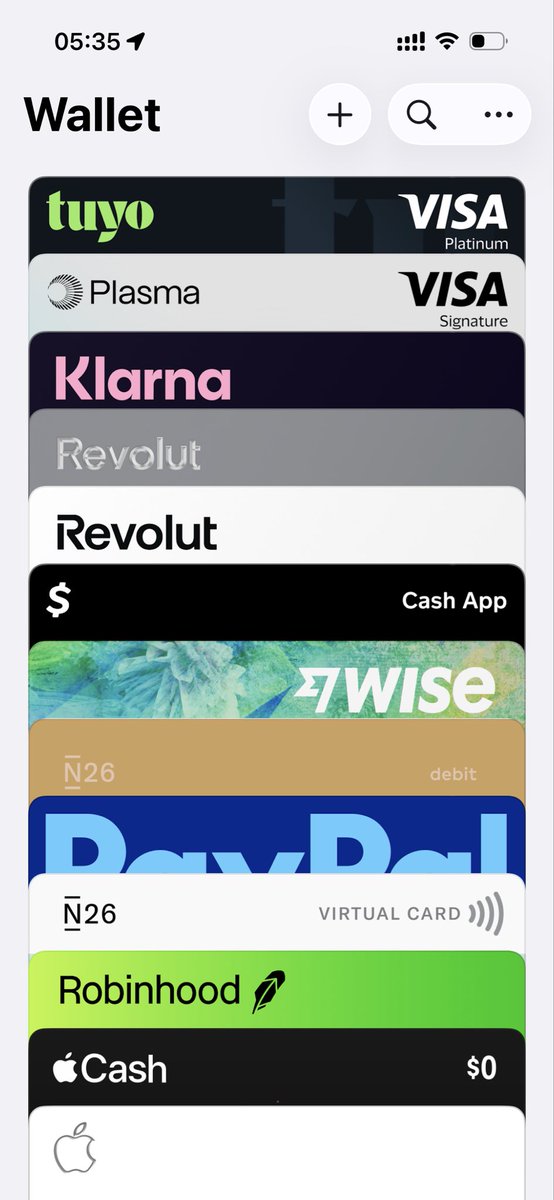

I've compiled a list of 326 neobanks

on X ALONE.

this is getting absurd:

@KASTxyz

@avici

@RedotPay

@ether_fi

@wirexapp

@payy_link

@coca_card

@itstuyo

@holyheld

@XMoney

@ready_co

@KoloHub

@Plasma

@useTria

@gnosispay

@Cypher_HQ_

@Karta_Personal

@phantom

@Solayer_Pay

@xMoney_com

@SolidYield

@xplaceapp

@bfinancepay

@brookwellapp

@solflare

@Exa_App

@UpholdInc

@KarmaWallet

@BleapApp

@Nexo

@Krak

@hyperbeat

@lava_xyz

@arq_finance

@belo_app

@lemonapp_ar

@mercadopago

@ripioapp

@joinpeanut

@minipay

@eldoradoio

@cashi

@trustee_io

@ur_global

@liminalcash

@oobit

@PulsarMoneyApp

@deel

@FlexSuperApp

@CashApp

i was only able to tag the top 50 due to X’s limitations on mentions

who did i miss off the list?

English