Sabitlenmiş Tweet

My company let me goes 2 months ago and I see where our economy is headed.

I pulled out out my 401k and slammed it all on #Bitcoin around $16.7k - $19k & Eth at & $595.

Did I make the right decision?

🤔🤔🤔

English

TEŁÇØĮN_ANDY

16.3K posts

@Blockchain_Andy

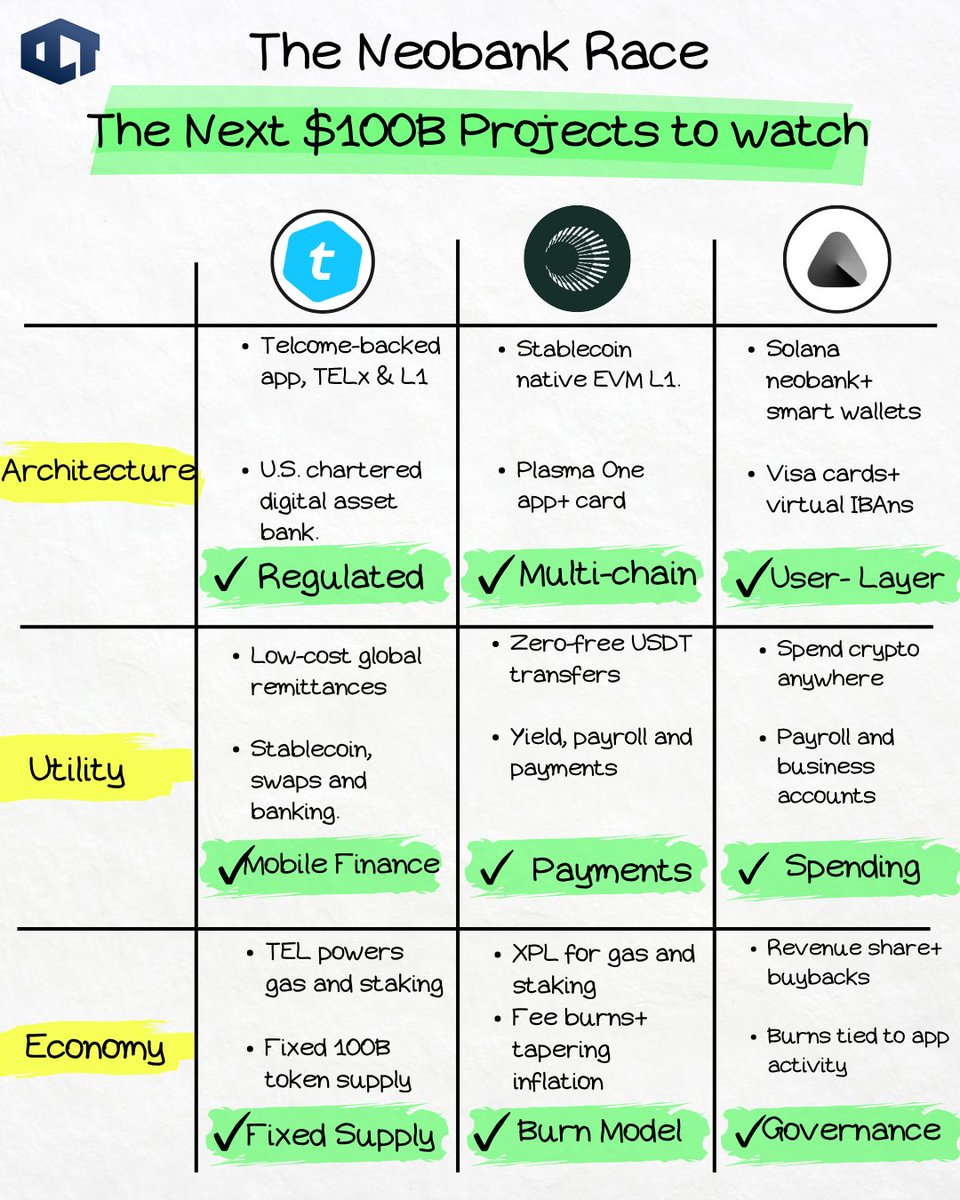

$TEL First Crypto Project To Be Approved In Nebraska For Digital Assets Depository.

JUST IN: Democratic Socialist Nithya Raman, dubbed "the next Mamdani," is now projected to win the LA mayoral election. 60% chance she leads the City of Angels.