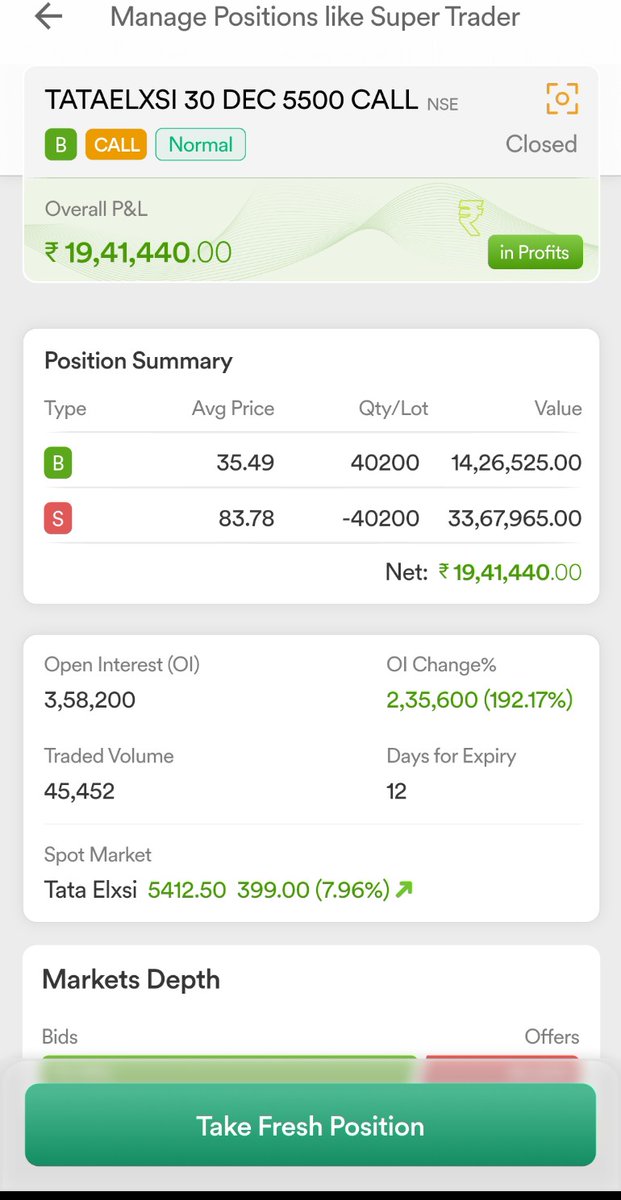

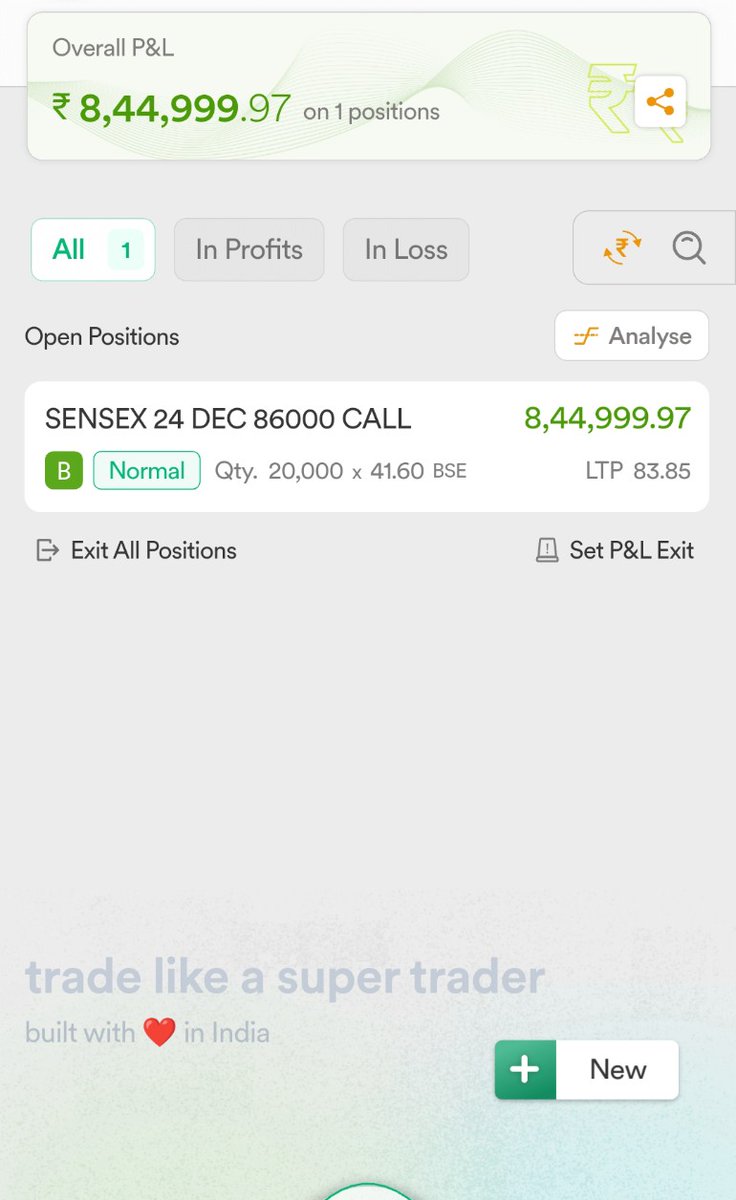

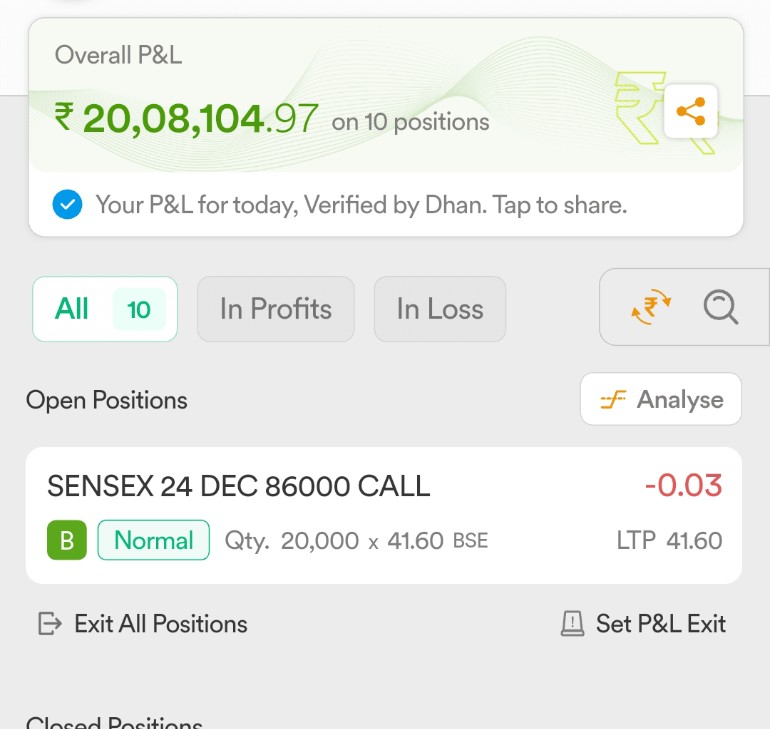

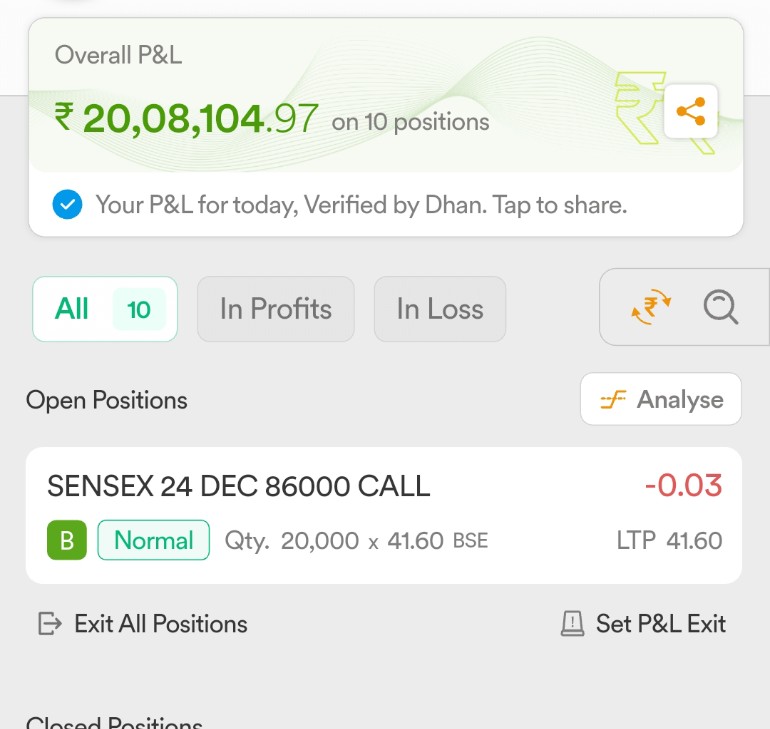

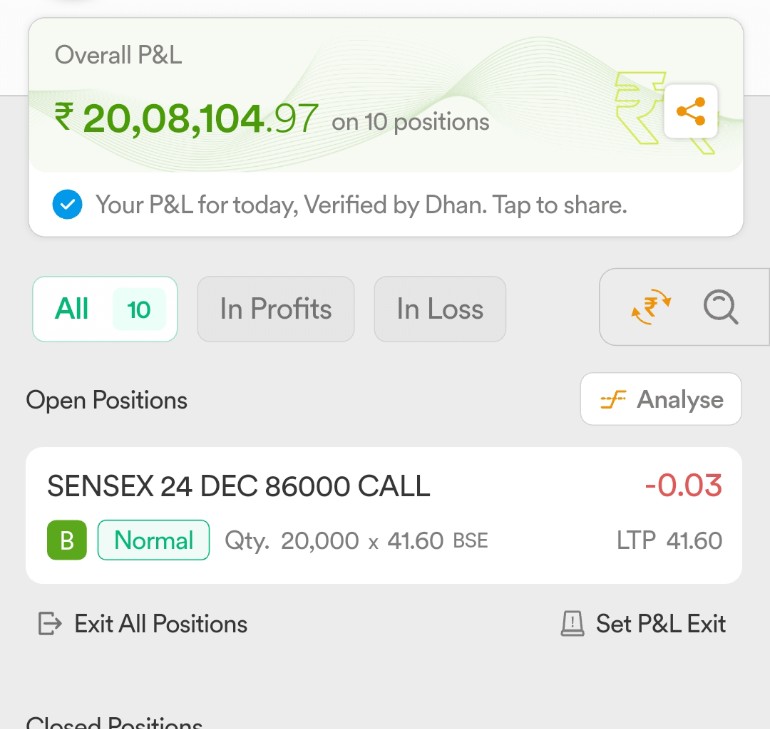

@BoomingTrder@piyush_trades Based on Black-Scholes, assuming Nifty gaps up 150 pts (Sensex ~490 pts to ~85,419) and IV ~8.1%, the SENSEX 24 DEC 86000 CALL could open around ₹68 on Monday. Market conditions may vary.

Situation of current businesses of Bhavish Agarwal:

> Ola cabs: lost big market share against uber and rapido

> Ola electric: market share fell from 35% to 7% in 1 year

> Krutrim AI: launched & disappeared so quickly that nobody noticed

This is all because of bad kamra (sorry “bad karma”) that he got from his customers.

That’s what happens when you sell faulty products and then deny even giving proper service to them in arrogance.

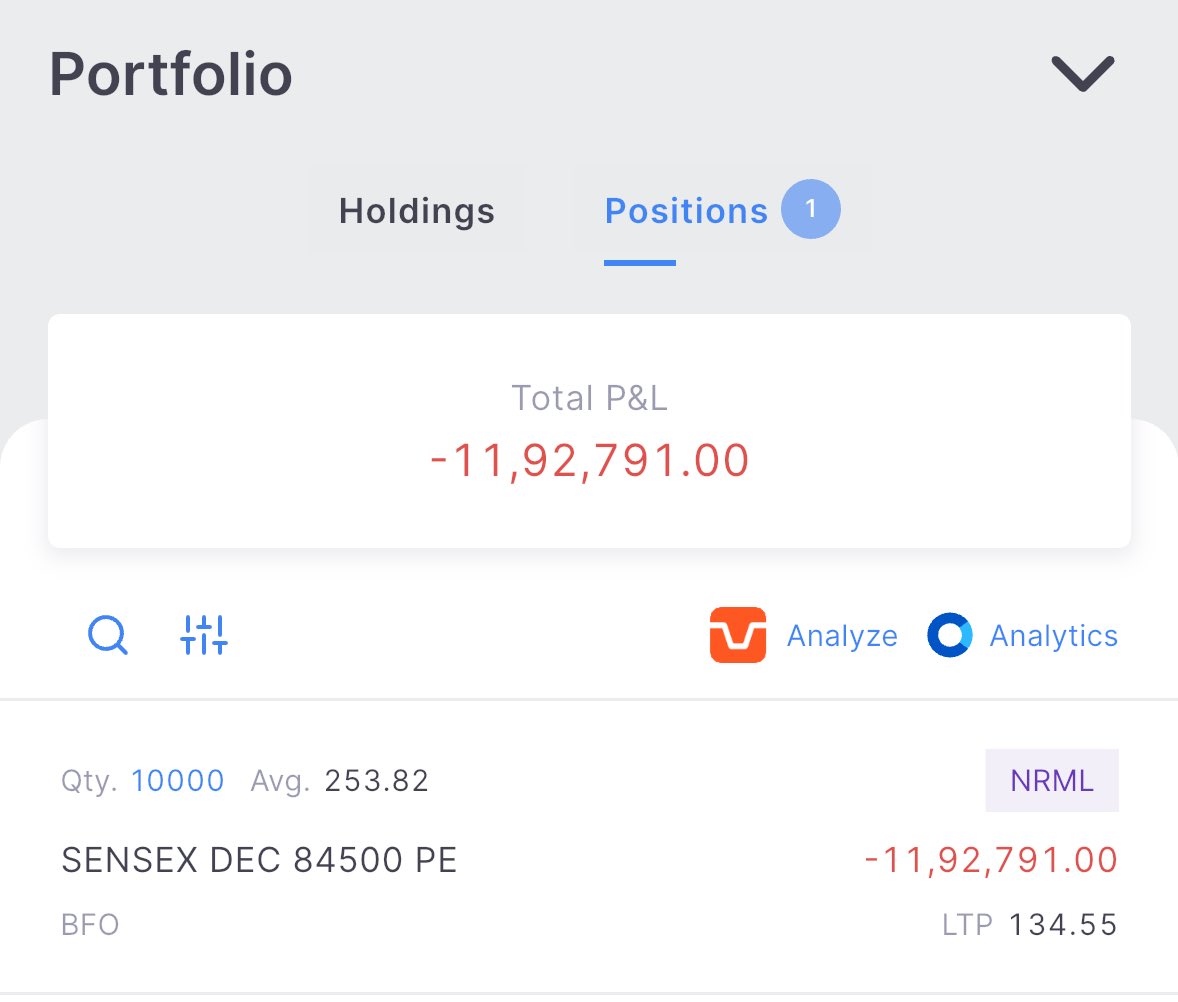

Going with NIFTY PUTS.

Not pushing higher qty as Friday and I don’t want to carry stress over weekend if I don’t exit.

NIFTY CMP : 25960.

So let’s go with Deep itm puts and see where we end.

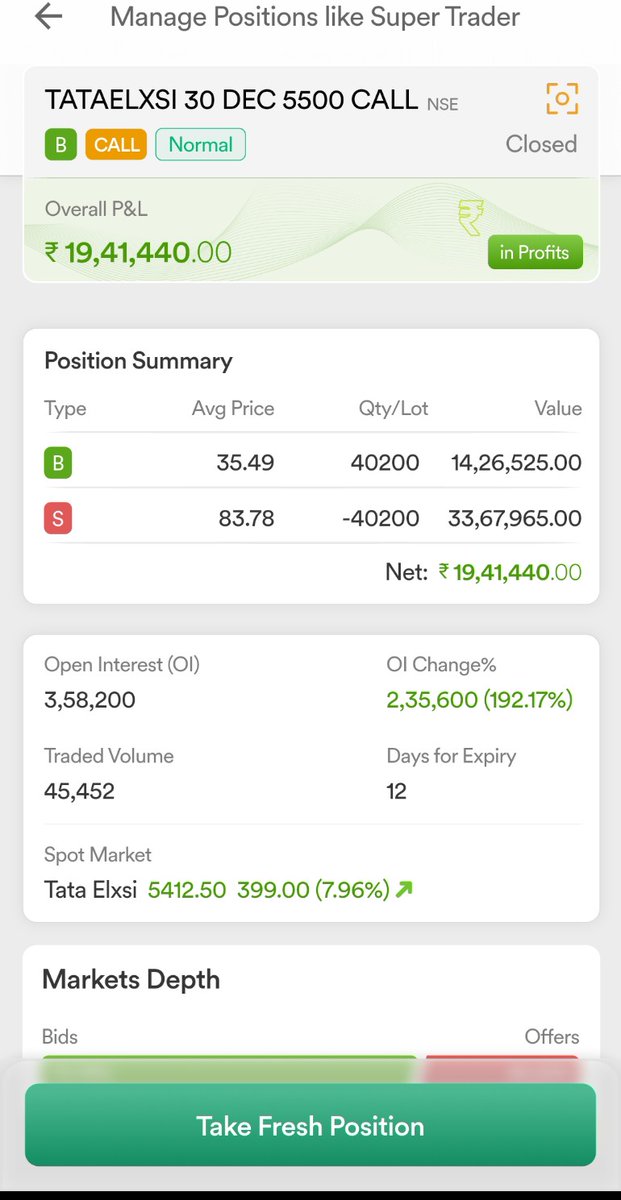

One common reason why traders blow up is because of poor position sizing. In other words, how much do you bet on a trade.

You can be right on direction 60% of the time and still lose everything if you size your positions poorly. One oversized trade can wipe out months of gains. This is why position sizing is a big part of risk management.

@mysandz recently spoke to Tom Basso, one of the original Market Wizards, to discuss his approach to trading. I was listening to the interview and the one thing that stood out to me was how Tom's thinking on position sizing evolved over decades.

He started simple: risk the same percentage of equity on every trade, inspired by Larry Hite's philosophy that every bet should be equal in terms of potential loss.

But then came a silver trade with explosive volatility. Clients were calling, nervous about the wild swings. So he realized it wasn't just about the amount you could lose—it was also about the speed of movement. High volatility creates psychological stress that leads to poor decisions.

So he added a second layer: volatility as a percentage of equity. Now he'd calculate both risk % and volatility %, then take the smaller of the two.

Then came the third refinement: margin-to-equity ratios. Some markets have deceptively low risk and volatility but require high margin because of sudden jump risk. By incorporating all three factors, he never got caught overexposed.

The result was a position sizing system that automatically scales down when markets get too volatile, protects against margin squeezes, and keeps portfolio risk in check. It's really interesting conversation. Link to the full interview is in the comments.

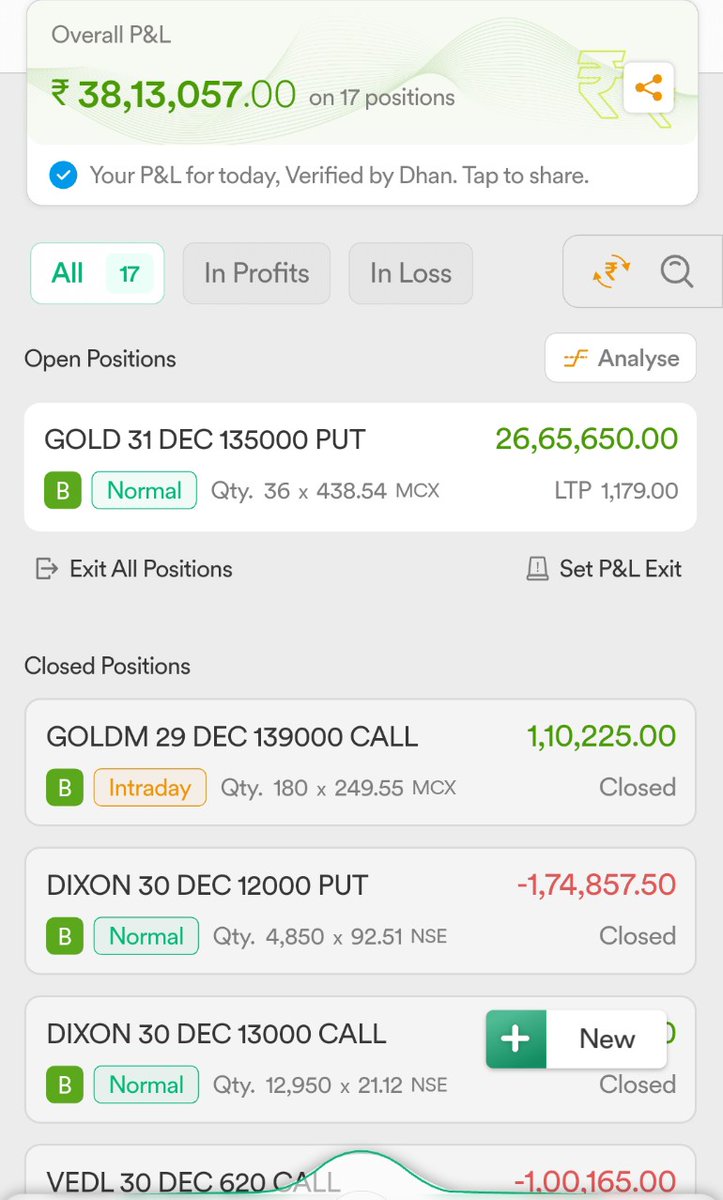

Options buying is king

And who says market is manipulative

#OptionsTrading#NSE#bse#HFT

Done for the day

Options buying can let all your dreams come true