Sabitlenmiş Tweet

John🎣

9.2K posts

John🎣

@BottomPhishing

Conditions-first tape reader. Daily reads, watchlists & regime calls. I don't force trades. I wait for the water to move. The discipline most traders skip.

Market Pulse Discord 👉 Katılım Ekim 2017

429 Takip Edilen1.3K Takipçiler

The June CPI came in at 3.5% year over year, well below the 3.8% consensus. Monthly CPI fell -0.4%, driven by a 9.7% drop in gasoline prices, more than double the -0.1% to -0.2% decline economists expected. Core CPI cooled to 2.6% year over year, its lowest since February, versus the 2.9% forecast. The breadth of the slowdown was the real signal. This wasn't one category pulling the number down. Disinflation is extending across multiple categories, and the data confirms what falling oil has been suggesting for weeks: the Iran war inflation impulse is fading. Fed rate hike odds for the July meeting dropped from 35% to 15% immediately after the print. Warsh told Congress during his first semiannual testimony that "the inflation surge of the last five years will be a thing of the past." The market believed him today.

The Nasdaq surged +0.90% to 26,107.01, reclaiming its 50-day moving average for the third time this month. The S&P 500 gained +0.38% to 7,543.59. The Dow was essentially flat at +0.02% to 52,508.27, but only because $IBM collapsed -24% and by itself cut roughly 425 points from the index. Without that single stock, the Dow would have been up meaningfully. Volume rose modestly on both exchanges, with Nasdaq volume up +2.27% and NYSE volume up +2.28%. Distribution days dropped to 9 on the Nasdaq and 5 on the S&P 500 as two older distribution days fell off the 25-day window. Exposure holds at 60%-80%.

Stock action showed 140 up on volume versus 116 down, with 7 near pivot and 1 breakout. The ratio is modestly positive. Semis bounced hard on the inflation data, with $AMAT up more than 5%, $LRCX, $TER, $STM, and $MU all gaining more than 3%. The $SMH ETF rose more than 2%. Tech led all sectors. The CPI print gave the chip group exactly what it needed: a reason for yields to fall and a reason for the Fed to hold.

Bank earnings kicked off Q2 reporting season, and $GS stole the show. Goldman posted EPS of $20.98 versus $14.48 expected on revenue of $20.34 billion versus $16.13 billion consensus. Equities trading hit a record as market volatility from the Iran war drove massive client activity. $GS surged more than 8%. $JPM rose +2.2% after reporting $16.9 billion in profit with record revenue in every business line and equities trading revenue up 35% year over year. $BAC beat with $1.21 EPS versus $1.13 expected. $WFC posted $2.00 EPS versus $1.72 consensus. The banks are making money on this volatility, and the earnings are confirming that corporate America is navigating the environment.

$IBM was the session's casualty. Shares plunged -24%, potentially the worst single-day loss in the company's history, after preliminary Q2 results showed revenue growth slowed to 1% with a 7% decline in infrastructure sales. CEO Arvind Krishna said clients shifted capital spending toward servers, storage, and memory in the final weeks of June, squeezing IBM's software and infrastructure stack. The irony: the same AI memory boom that is powering $MU and $SKHY is pulling spend away from IBM's legacy businesses. One company's buildout is another company's budget cut.

Trump backed off his demand for a 20% shipping fee through the Strait of Hormuz but the U.S. launched fresh strikes on Iran overnight. Oil settled up 1.5% on WTI above $79, touching $80 intraday, with Brent above $84. The energy picture is more complicated than the CPI suggests. June's gasoline prices drove the inflation decline, but oil has risen sharply again in early July on the reinstated blockade and continued hostilities. Regan Capital's CIO framed it well: the Iran war inflation surge is fading, but this may just be temporary relief as tensions have escalated in recent days. The next CPI print will tell you whether falling oil was a trend or a one-month head fake.

Still on vacation with the family, disconnecting as much as possible. The CPI print and bank earnings gave the tape a solid foundation to build on, but the Iran escalation and oil above $80 are the counterweight. Earnings season is just starting. $TSM reports Thursday. Warsh testifies again Wednesday. The data will keep coming whether I'm watching or not.

Tight lines and tighter stops 🎣

The StrikeZone for Wednesday, July 15:

$SPY, $SSO

English

Oil above $79, Brent above $84. Trump backed off the 20% Strait of Hormuz demand but U.S. launched fresh Iran strikes overnight. June gasoline drove the CPI decline, but oil has risen sharply in early July. The energy picture is more complicated than the stat suggests.

English

Yesterday: Big money was selling the biggest stocks hard enough to drag the indexes down, but most stocks aren't participating in that selling. That's the divergence. Ten distribution days means there's been a lot of institutional selling pressure. 60%-80% exposure means I'm not pressing, just watching.

English

There’s a time to go long, time to go short and a time to go fishing. 🎣

English

Distribution hit double digits on the Nasdaq. The Nasdaq fell -1.55% to 25,873.18, the S&P 500 dropped -0.79% to 7,515.34, and the Dow slipped -0.26% to 52,498.64. The Russell 2000 lost -0.83%. NYSE volume surged +17.91% while Nasdaq volume ticked up +1.85%. Distribution days climbed to 10 on the Nasdaq and 6 on the S&P 500. Ten distribution days. That number has never been this high during the entire uptrend. Exposure holds at 60%-80%.

Stock action showed 97 up on volume with zero down for the second consecutive session. 7 near pivot. 1 breakout. The zero-down reading is notable even on a day where the Nasdaq lost more than 1.5%. The selling is happening in the heaviest-weighted names while the broader list is not participating in the liquidation on volume. That divergence has been the defining feature of this tape for over a month, and it's still intact.

Trump escalated the Iran conflict again. He posted on Truth Social that the U.S. is reinstating "THE IRANIAN BLOCKADE, so named because it is only stopping Iran's ships or customers from entering or leaving." He also announced a new 20% fee on international shippers. The U.S. and Iran exchanged heavy airstrikes over the weekend, marking the most significant escalation in the scale and reach of attacks since the conflict began on February 28. Tehran said it has closed the Strait of Hormuz. The MOU signed in Switzerland last month is now functionally dead, the blockade is back, and the brief window of falling oil that gave the market its best stretch since April is over.

Oil surged 9.4% on the session, with crude settling near $77.68. That's a $7 move in a single day and the sharpest one-session spike since May. Energy stocks rallied, with the $XLE gaining 3%. But the damage to the rest of the tape was immediate. Every dollar higher in crude feeds directly back into the inflation picture that was just starting to ease. The 10-year yield advanced. The dollar strengthened. The consumer squeeze that falling gas prices had begun to relieve reverses if oil stays at these levels.

Semiconductors took the worst of it. $SKHY dropped -9.3% on its first full day trading under the new ticker, giving back most of Friday's 13% debut gain. $SNDK fell -12.3%. $MRVL lost between 6-12%. $INTC dropped -6.1%. The Philadelphia Semiconductor Index was the session's clear underperformer. The chip group that has been repricing since early June now faces the added headwind of rising energy costs, higher inflation expectations, and a Fed chair who is about to sit for his first semiannual Congressional testimony on Tuesday and Wednesday. Warsh will be questioned directly on the inflationary effects of the conflict and the path forward for rates.

Financials rose +0.65% ahead of big bank earnings starting Tuesday, with $C and $GS both reporting. Utilities gained +0.68%, the session's best-performing sector. When utilities lead, the market is telling you it wants safety, not growth.

This is our family vacation week, so I'm stepping back and disconnecting as much as possible. I'll put out StrikeZone watchlists periodically as I scan, but the priority this week is stepping away and letting the market sort itself out. Between double-digit distribution on the Nasdaq, the Iran blockade back in effect, oil spiking 9% in a day, and Warsh testifying before Congress for the first time, there's no shortage of catalysts. But none of them require me to be at the screen. The tape will be here when I get back. Right now, the water is more productive than the charts.

Tight lines and tighter stops 🎣

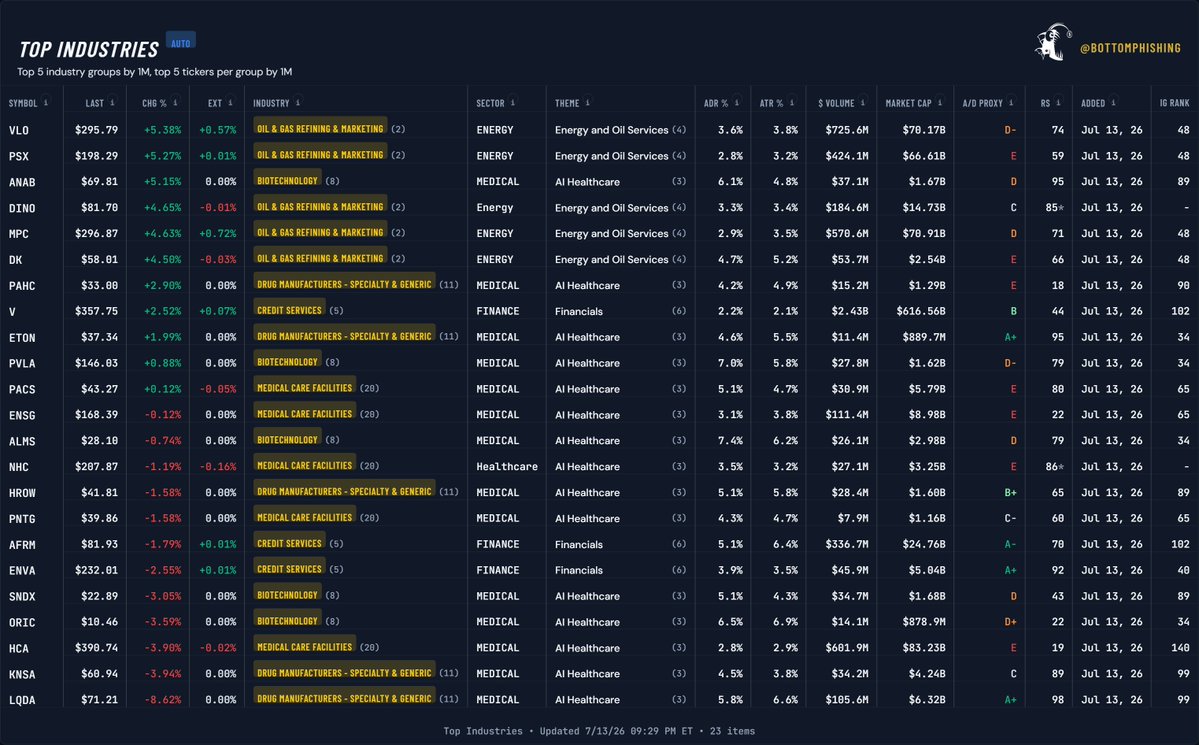

Top Industry Group Theme Tracker tickers for Tuesday, July 14:

$VLO, $PSX, $ANAB, $DINO, $MPC, $DK, $PAHC, $V, $ETON, $PVLA, $PACS, $ENSG, $ALMS, $NHC, $HROW, $PNTG, $AFRM, $ENVA, $SNDX, $ORIC, $HCA, $KNSA, $LQDA

English