BrandonMFarley

219 posts

@HumansNoContext Terrible mistake doesn’t make him dumb or stupid.

English

The internet is debating on if this is fat or not, is she?

English

Lets pray together🙏

Heavenly Father, cover Ivanka with Your peace that surpasses all understanding. Guard her heart, her mind, her home, and her family. Send Your angels before her, behind her, and beside her. Let her walk in safety, strength, and courage, knowing that You are her refuge and fortress.

We thank You that she is safe. We thank You that darkness did not prevail. And we ask You to continue protecting President Trump as he stands in Washington carrying the burden of this nation during such a serious time.

The Lord is our light and our salvation. Whom shall we fear?

God protect Ivanka.

God protect President Trump.

God protect the Trump family.

God protect America.

English

@ClownWorld I’m fine with his actions. Bikes have a right to be on public roads. Dogs should be secured.

English

@PhantomBlack699 A delay tactic??? Does someone think something is inevitable and trying to pushback whatever date they can???

English

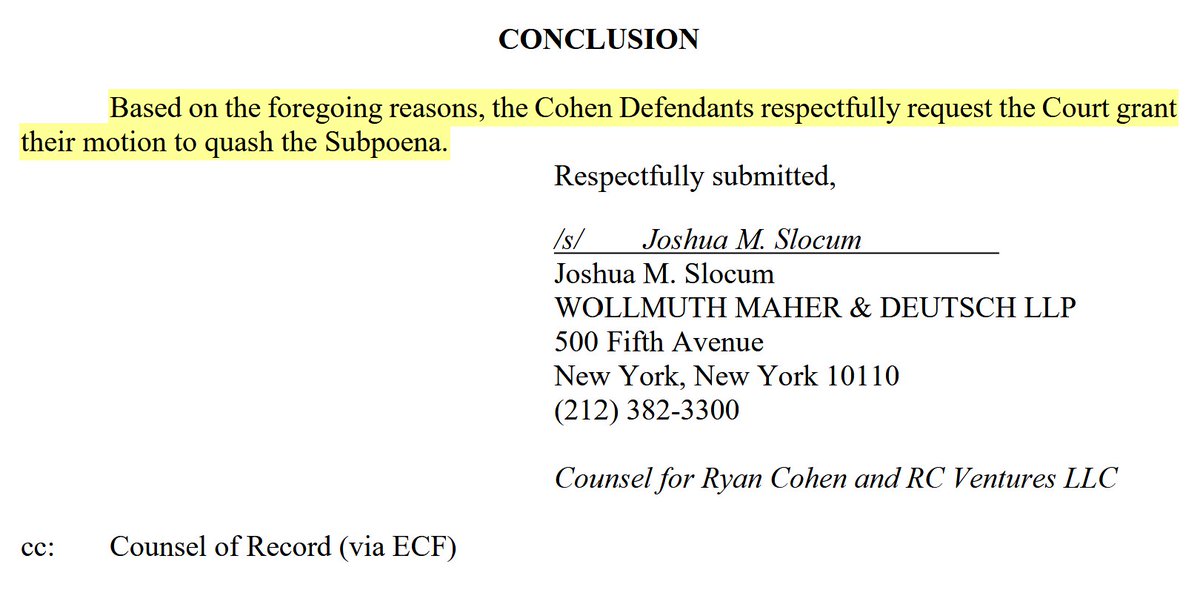

Ryan Cohen V DK-Butterfly discovery documents were just filed

The Cohen Defendants ask the Court to enter an order quashing the subpoena in full, as the subpoena was served long after the fact-discovery deadline.

This is related to the Section 16b short swing profit claims. Fact discovery closed on January 30, 2026.

English

@mqudsi @SprinterPress People with big butts will look taller while sitting down

English

@SprinterPress They’re the same height (cushions, too). One president is just a weeeeee bit heavier than the other causing the cushion to sink.

English

The Chinese applied their tricks on Trump, giving him a smaller chair than the one the Chinese president sits on!

The discomfort on Trump's face is obvious, as Xi appears to be a head taller!

English

This guy is using the left hand lane , which is open. There is a mile long backup and everyone is over in the right hand lane.

He drives all the way up until he has to merge.

Some people are saying what a jerk he is for not getting in line like everyone else, but a great many people are saying that the cars in the right lane merged into one lane too soon and that if they had used the left lane, instead of being a mile backup it would have been a half a mile backup.

What’s your take? Do you think he was correct in using the left lane and merging up at the front or should he have merged right and got in line way in the back like everyone else?

English

@ReesePolitics Removes Conflicts of Interest. Doesn’t seem bad to me.

English

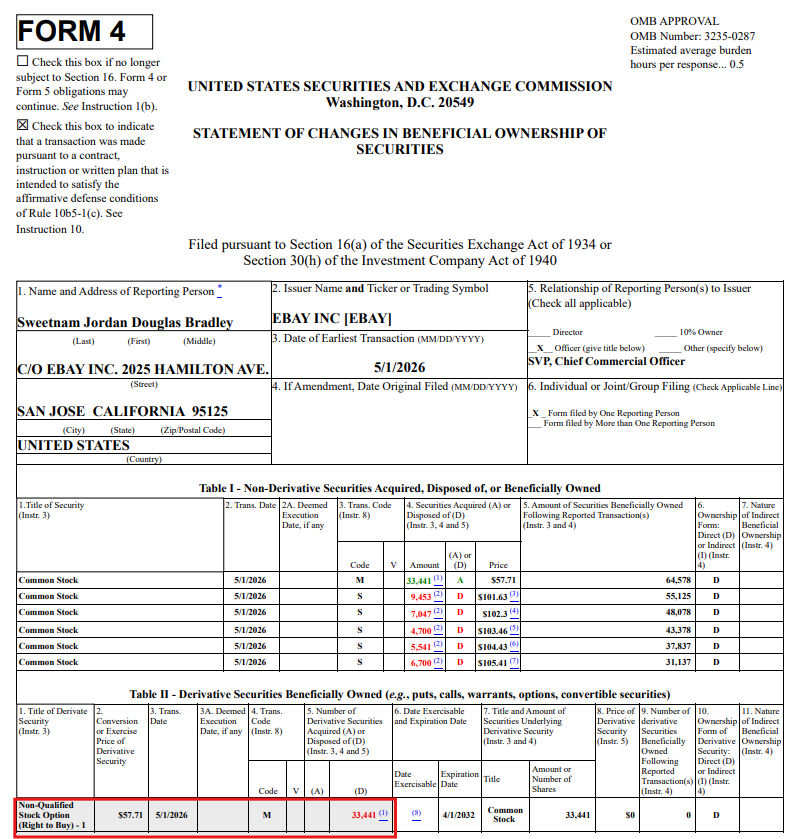

Wow EBAY CEO Jamie Iannone just sold $4,550,000 worth of stock and SVP CCO Jordan Sweetnam sold $3,426,000 on May 1, the same day WSJ published its exclusive $GME takeover bid story.

That is not a good look for EBAY.

English

@xMarketNews Shorts panicking??? More like, Shorts excited!

English

BREAKING🚨 GAMESTOP COST TO BORROW RATE INCREASES 200%+ (from .66 to 2.04)

SHORT INTEREST INCREASES TO HIGHEST LEVEL SINCE MARCH AT 17%+ $GME

Shorts are starting to PANIC ⬇️

English

@PhantomBlack699 Judging by eBay current share price, doesn’t look like folks are taking offer seriously. eBay at about 109 right now.

English

@PhantomBlack699 Honest question… What does “Tokenization” do? Without explanation, I imagine that instead of buying/selling one share… it could be a different unit.

English

Reminder that Citadel were panicking about tokenization and suggested that the SEC "tread lightly" 👇

Salvatore Linteum@PhantomBlack699

Citadel are in panic mode over stock tokenization Last week, Citadel issued a letter urging the SEC to “tread cautiously” with tokenization link to letter: sec.gov/files/citadel-… CNBC attempted to probe into Ryan Cohen’s plans on tokenization in their interview, but were quickly shut down by the GameStop CEO. The $GME share price has been suppressed heavily recently, with 80%+ of daily trades routed through dark pools to avoid organic price discovery on the lit markets. Citadel are scared of the tokenization button being pushed, here are some insights into their letter to the SEC. Citadel uses this letter in an attempt to position itself as a "champion of regulation and transparency" despite facing a $7 million SEC fine in 2023 for order mismarking violations that directly relate to short selling practices: cnbc.com/2023/09/22/sec… Citadel Securities urges the SEC’s Crypto Task Force to treat tokenized U.S. equities (new “look-a-like” securities issued on blockchains) as fully subject to existing securities laws rather than granting broad exemptions. While acknowledging that limited technical accommodations may be needed to address blockchain-specific features, Citadel warns against self-serving attempts to bypass core rules and emphasizes that real innovation must come from improvements in market efficiency, not regulatory arbitrage. Citadel processes approximately 47% of all U.S.-listed retail volume and want to retain their dominance in the settlement markets, tokenization is a threat to their business model. Several of Citadel’s “public-interest” recommendations would keep tokenized U.S equities inside today’s opaque, centralized clearing structure, exactly the environment that allowed its 2015-2020 Regulation SHO mismarkings and other naked-short-related controversies to go undetected. By rejecting real-time, on-chain settlement (the accountability model Overstock adopted with its tZERO blockchain dividend) Citadel preserves market practices that can obscure share inventory and delivery-fail data. Here are the recommendations made in the letter, with the self-serving benefits they provide to naked short selling and malpractice under the guise of concern and transparency: Recommendation A Require tokenized-equity trading venues to register as full national securities exchanges, not ATS “sandboxes,” and undergo the full rule-filing, cybersecurity and fair-access regime Why this is self-serving Exchange registration demands multimillion-dollar compliance infrastructure already built by Citadel’s preferred partners; it discourages lightweight blockchain venues that could clear and settle continuously on-chain. Potential Impact on Naked Short Selling practices Forces tokens back into the DTCC/NSCC settlement loop where fails-to-deliver are netted and obscured, reducing the ledger-level visibility that real-time token settlement would provide. Recommendation B Reject all “broad exemptive relief” and treat tokens as traditional equities subject to T+2 net settlement and Section 31 fee funding Why this is self-serving Maintains the same batch-settlement timetable that regulators cite as fertile ground for naked shorts (locate failures can be hidden for two days). Potential Impact on Naked Short Selling practices Prevents atomic, delivery-versus-payment settlement that would immediately expose unlocated shares, the mechanism tZERO designed to “box in” naked short sellers Recommendation C Insist that blockchains are “not a substitute” for the consolidated tape and cannot provide real-time post-trade data Why this is self-serving Undermines the core transparency advantage of tokenization; an immutable ledger of every share. Potential Impact on Naked Short Selling practices Keeps regulators and investors dependent on broker-dealer blue-sheet data, the very data Citadel "accidentally" mismarked for five years, obscuring millions of short-sale orders. Recommendation D Emphasize margin frameworks and close-out rules within existing broker-dealer pipes rather than on-chain collateral management Why this is self-serving Leaves Citadel’s wholesale market-making business in control of locate services and buy-ins, revenue streams threatened by blockchain-based “Digital Locate Receipts” like tZERO’s. Potential Impact on Naked Short Selling practices Continues the practice whereby brokers can delay or partially locate shares, a key enabler of naked short selling. Recommendation E Citadel argue that tokenized equities issued by third parties will “siphon liquidity” and create “counterparty credit risk” Why this is self-serving Frames innovative token issuers as risky while ignoring that Citadel’s own order-flow internalization concentrates liquidity. Potential Impact on Naked Short Selling practices Discourages issuers from exploring token dividends (e.g., Overstock’s OSTKO) that force reconciliation of share counts and trigger short squeezes when excess synthetic shares exist Several policy demands in Citadel’s submission, portrayed as investor-protection steps would lock tokenized equities into the same centralized structures where mismarked or undelivered shorts can hide, erect high compliance costs that deter novel, transparent blockchain venues, and deflect momentum toward real-time share-inventory reconciliation. Citadel fear accountability. Given Citadel’s recent Regulation SHO infractions and its dominant role in retail order flow, the firm has clear incentives to resist a tokenized framework that could make every locate, borrow and fail-to-deliver visible in real time. Citadel’s surface level regulatory Virtue Signalling within this letter is pretentious, and the embedded concerns around settlement obligations is the real concern they have with stock tokenization.

English

@RagnarRiese yeah let him post a yolo update when $GME has a pending m&a that could tank the stock short term if anything lol makes total sense to do it now lol

English