Bry_mon

280 posts

Omg, I’m getting the itch to take a camera and just stream of conscious talk to it. Post it on a YouTube channel.

500 likes and I’ll start posting videos this summer.

Not engagement farming. Just seeing if there is interest.

English

Without skin in the game it’s just chill analysis. With real money on the line? Way more emotionally taxing.

The AI Investor@The_AI_Investor

$MU - the fragility is real after betting big on something like DRAM recently and digging into all kinds of numbers and scenarios, from GPU HBM demand to CPU DRAM projections, plus the memory supply side, etc. Looks like just a few articles but it ended up consuming so much of my time and mental energy because of the sizable bet. Much more relaxed if I just write about things without putting big money into them. Need some rest lol

English

@Sandeman52 I started seriously last March (transferred assets to RH in May). With about $25k I think. Up till now I've probably put in a little over $5k of extra cash. But as of today...

English

$NBIS Anyone a millionaire yet? If not don’t worry, it’s early!

SandemanStocks@Sandeman52

I’m going to make some of you millionaires. I don’t want anything in return.

English

@k_a_y_b_e_e_ @aleabitoreddit I ended my sub for them. I learned that I need a more concentrated portfolio. They do pick good companies, but they list out so many.

English

@aleabitoreddit Loved how you stood up to the Citrini folks bearish On AAOI. Especially after they were riding high from the doom porn post

English

$AAOI is now up ~6-7x at $200+.

Feels like nobody else was long last year aside from me and like two other people on X?

Remains one of my top high conviction optical longs moving forward into 2027 due to massive revenue ramp + Made in America supply chains.

English

$NBIS Numbers are great y'all

Peter Morley@wienglischmann

$NBIS Some highlights from our Q1 2026 earnings: * ARR +674% YoY; FY guidance updated to $7-$9B ARR and $3.0-3.4B revenue. * Adj. EBITDA margin for AI cloud up nearly 2x QoQ to 45%. * Contracted capacity now >3.5 GW, ahead of 3 GW target; targeting >4 GW by YE26. We also announced that we have secured up to 1.2 GW of power and land for a new owned AI factory in Pennsylvania, bringing our total number of sites exceeding 100 MW to seven. Full press release here: nebius.com/newsroom/nebiu…

English

$NBIS

- Contracted capacity now exceeds 3.5 GW, surpassing our 3 GW target; we now expect to have more than 4 GW of contracted capacity by the end of 2026.

“We also announced today that we have secured up to 1.2 GW of power and land for a new owned AI factory in Pennsylvania, bringing our total number of sites exceeding 100 MW to seven.”

Are you kidding me??!!🙏🙏🙏🫠🫠🫠

English

@aleabitoreddit I see some people say they don't like trading Taiwan stocks because of the illiquidity. Is it really that illiquid? If so, do you have any concerns about it?

English

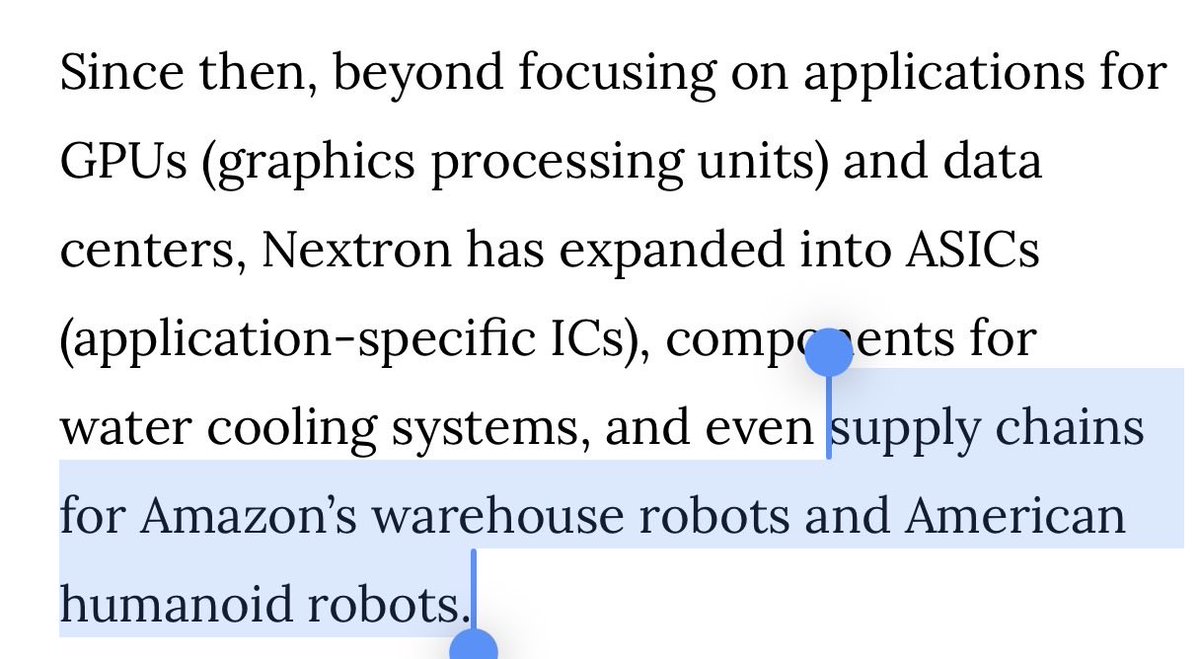

Just putting it out there with the Goldman Sachs $NVDA supplier note.

There’s a very interesting ~$210m MC company Nextronics (8147) that I ended up taking positions on following GS.

That supplies CPO connectors and Cage Thermal Modules to Nvidia CPO supply chains.

They’re also in $AMZN supply chains and Humanoids. And massage chairs too.

Just thought I’d share an interesting idea (NFA/DYOR), I’ll do a BOM analysis later, but it looks very material relative to MC as Nvidia’s CPO program scales up.

Of course risks are multi-sourcing/getting designed out, but there’s probably a reason why GS flagged this micro supplier multiple times among $4-10B+ companies.

Serenity@aleabitoreddit

Today I learned there’s a $NVDA CPO supplier that builds massage chairs and US Humanoids on the side. The Toto toilet HBM meme keeps showing up everywhere.

English

@Ren_aramb Market euphoria is a clear sign of an overheated market!? Get ready for the 🐻 attack!

English

@Gubloinvestor I bought 33,587 shares at $1.32. Might as well hold it forever.

English

You can earn so much by just listening to earning calls and interpret the numbers.

The algo’s just look at the basic earning numbers and decide to trade on that, they don’t interpret them.

There are so many examples.

For $FLNC the algo’s pushed it from 12 to 16. If you would have listened to the earnings you realise that 16 is still way too low, so I bought. 1 day later and Fluence now trade at 24.

Same for $WOLF, the numbers in itself weren’t fantastic so algo’s pushed it down 12%. But if you know the company and listen to the earnings call, you would have realised they are on the right track, $WOLF is now up 32% since.

Another example, but one I couldn’t capitalise on is $AEHR. I remember them beign down 12% in aftermarket. I wanted to buy them but I don’t have broker who supports that. $AEHR is up 50% since.

Learn to interpret the numbers and what you should be looking for in an earnings call and you’ll be a better investor.

KaizenInvestor@Kaizen_Investor

Just listened to the earnings call from $FLNC and decided to add to my position at $16.67. The earnings were spectacular in my opinion. Yes, they missed revenues due to a delayed shipment of $80 million, but the backlog keeps rising and Fluence management is confident they can deliver. 50% of the backlog comes from new customers and the main part of this backlog is for datacenter purposes. The datacenter backlog is around 12 GW, with the major part of this connected to 2 hyperscalers. To give you an idea, Fluence now have around 22GW deployed or contracted globally. So, this is a major deal. They announced 2 MSA's with major hyperscalers and are expecting a first order in Q3 already. They also said that they would speed up delivery for these hyperscalers and are expecting deliveries within a year. So, we should see first revenues from these deals in 2027. They also explained the heavy selection process for these hyperscalers. Apparently 26 companies were notified, but due to the difficult technical specifications most of the companies could not fit the standards. The main reason they were able to agree these MSA's was due to the fact that their technology is already proven. He spoke about the Fluence lab, so I suppose these Hyperscalers visited the lab and approved. The main focus remains on top-line growth. There were some questions about the high OPEX costs in percentage of revenues but Fluence want to control these by growing revenues instead of lowering costs. Happy to have started a stronger position here. Datacenters are looking for high quality of power to get them through the fluctuations and it looks like Fluence can provide it. Now valued at $3.4B with a $5.6B backlog, still looks pretty cheap.

English

@pepemoonboy This is what I'm trying to learn how to balance as well. I know it's near impossible to time bottoms and tops. But I also want to let winners win. So I did $AXTI CCs cause I was up 300%. Got assigned, but profit is profit. And it was almost 30% of port at a certain point.

English

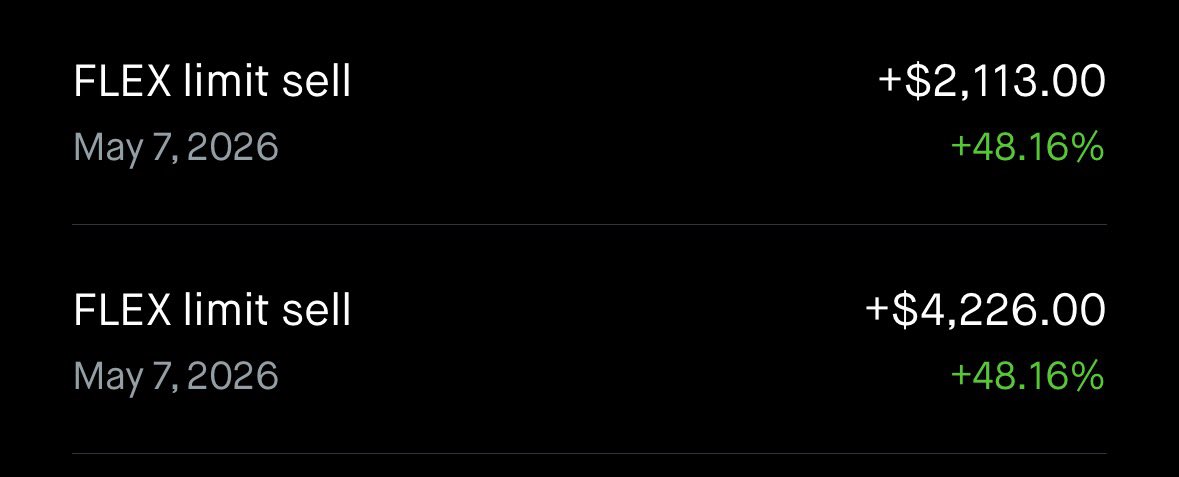

I sold 150 of my 400 $FLEX shares.

Why?

Because I initiated my position 15 days ago and it went up 50%.

That’s an insane return in two weeks…

Additionally, it made up around ~40% of my AI portfolio, which is too much in my opinion.

I do believe in the company, which is why I’m planning to hold the remaining 250 shares long term.

This is not financial advice, just a transparent look into my thought process and investing journey.

I’m learning to trim on the way up, which has always been difficult for me to do.

It’s not easy, but I believe it needs to be done when the underlying stock has had parabolic moves in a short period of time.

Many of you “expert” investors/traders may not agree with the move, and that’s ok.

Profit is profit baby!

Pepe Invests@pepemoonboy

I think I found a gem that no one is talking about yet. Everyone on FinX talks about the same stocks, but every now and then a gem that no one has heard of pops up. The company I'm talking about is Flex Ltd., ticker symbol $FLEX. 🧵 Why $FLEX might be an undervalued stock in the AI infrastructure space right now. A thread.

English

@Ren_aramb They're going have dilution voting results May 15th. Maybe we get another entry point there.

English

Which stock do you regret the most not buying after looking it up or ended up selling to soon?

For me it’s $AXTI

Bought it at 16, watched it go all the way up to 70 just to sell it at 56 due to dilution scare and it’s now trading back at 116 just one month later, and it will continue rallying.

English

@michaelsikand @LeStonkJames He sounded annoyed because they didn't understand what it actually takes to produce their products.

English

@LeStonkJames I loved when he chuckled and said this was my PHD thesis. He said I think we know how to make these lasers.

English

Management is the bear case with $AAOI.

But I like that it's a founder led company.

Founder/CEO Dr. Lin has not made an informative sell after a 900% 1Y rally.

He's ONLY been making informative buys. $1M total since last May.

Lin thinks he can make a generational play.

Michael Sikand 🦑@michaelsikand

The reason $AAOI is such a volatile stock... These dudes are either lying SO hard or this is the most asymmetric set up in the stock market. Today they said they can go from $150M/quarter to $470M/month in ONE YEAR. Photonics TAM says yes. Mgmt track record does not.

English

Maybe we’re all just overthinking it…

After hundreds if not thousands of trades. My YTD is barely more than half of that of $SNDK, which hasn’t stopped going up.

Going forward, if anyone asks me for investing advice, I’m going to irresponsibly tell you to full port $SNDK and call it a day.

Just kidding… or maybe not…

English