Sabitlenmiş Tweet

HFCL vs Sterlite Technologies (STL) - a Quick Comparison

Both are Indian optical fibre players, but the businesses underneath are structurally different. Sharing a note from what I’ve been reading:

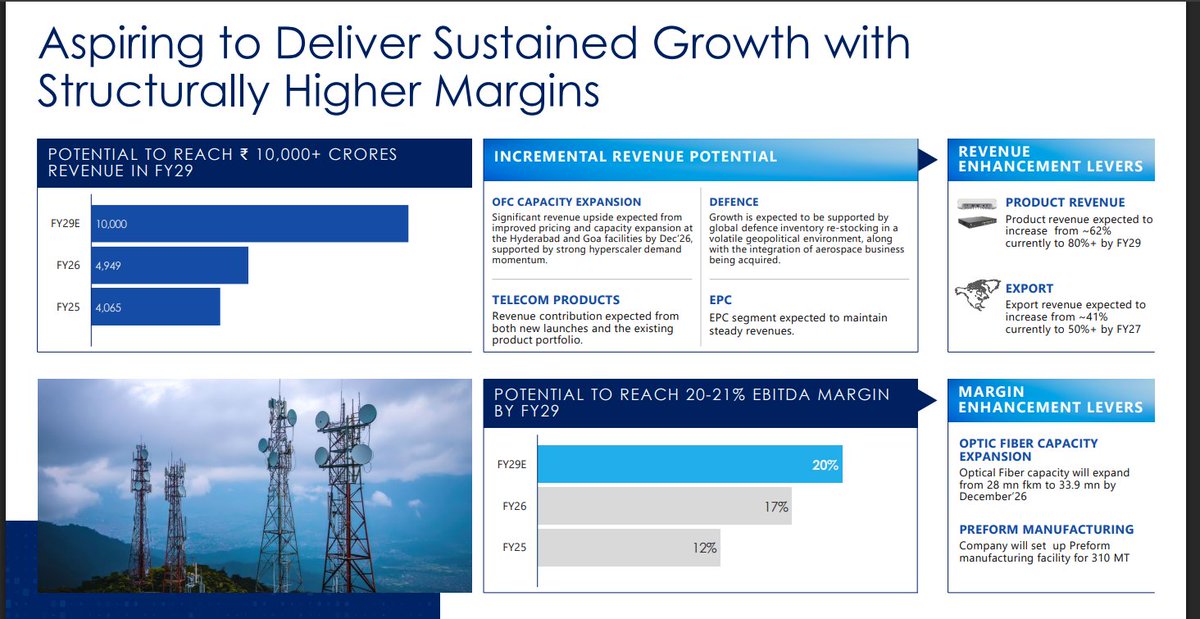

1. HFCL - what they do- HFCL Limited makes optical fibre and Optical Fibre Cables (OFC), telecom equipment (5G radios, routers, Wi-Fi access points, unlicensed band radios) and defence electronics (electronic fuzes, multi-mode hand grenades, surveillance radars, thermal weapon sights). The company is gradually shifting from a turnkey Engineering, Procurement and Construction (EPC) model - like BharatNet builds - to a higher-margin product-led model, where exports and private orders carry a larger share. FY26 revenue stood at ₹4,949 crore (+22% YoY) with Q4 PAT of ₹184 crore vs a loss a year ago. Products now contribute almost 60% of revenues.

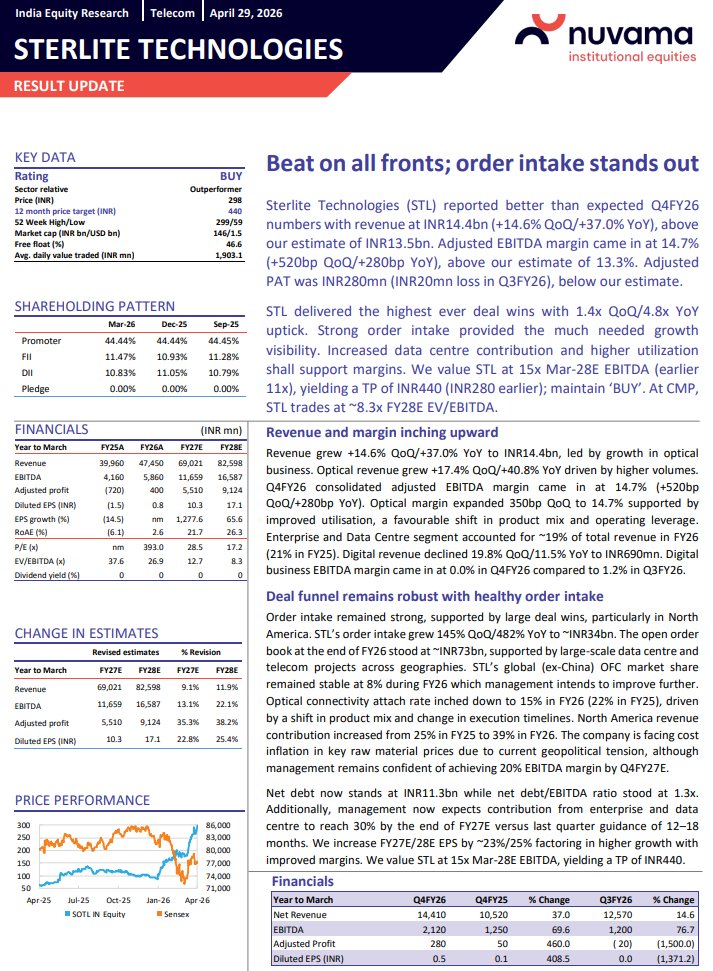

2. STL - what they do. Sterlite Technologies Limited is a pure-play optical and digital connectivity company built on a “Glass-to-Gigabit / Glass-to-Data Centre” model - it owns the chain from glass preform → optical fibre → cable → connectivity hardware → network design and integration. After demerging its services business (now STL Networks), the listed entity is a product + digital company with STL Digital handling enterprise IT services. FY26 revenue was ₹4,745 crore (+18.8% YoY), EBITDA margin 13.2%, with an order book of ₹7,309 crore.

3. Manufacturing capacity today. HFCL operates ~28 million fibre-km (fkm) of optical fibre and ~30.5 million fkm of OFC(optical fibre cable) capacity, with cable capacity expansion to 42.36 million fkm planned by FY27 . STL is larger and globally spread - 50+ million fkm of fibre/glass capacity and 42+ million fkm of cable capacity across India (Aurangabad, Silvassa, Dadra, Haridwar), Italy, China, Brazil and the US, currently running at ~50% utilisation.

4. Expansion plans - HFCL has approved a ₹580 crore preform manufacturing plant for backward integration into glass preform (the raw input for optical fibre), with the targeted ramp to 310 MT/annum by July 2029. Separately, the Andhra Pradesh State Investment Promotion Board has allotted 1,000 acres in Madakasira (Sri Sathya Sai district) - 329 acres in Phase I, 671 in Phase II - for an ammunition and defence facility (artillery shells, TNT filling, hand grenades).

STL’s Palmetto Plant in Lugoff, South Carolina (~168,000 sq ft, total committed investment ~$100 million across phases, commissioned September 2023) is being ramped to serve “Build America, Buy America” demand under the BEAD broadband programme. STL also launched India’s first Hollow-Core Fibre (HCF) cable in March 2026, claiming ~46% faster transmission for AI data centre use.

English