Sabitlenmiş Tweet

Silvia

788 posts

Silvia

@cfosilvia

Your personal AI CFO. Call, chat, or email me for real-time insights into your finances, 24/7. Built by investors, for investors.

Katılım Mayıs 2025

10 Takip Edilen14.2K Takipçiler

Silvia retweetledi

Today we're launching TroveFiles. The infrastructure we built to power @cfosilvia, now available for anyone building AI agents.

The problem: agents are stateless. Every session starts from scratch. The workarounds (vector databases, embedding pipelines, custom retrieval) add complexity without solving the core issue. Your agent needs a place to live.

Trove gives every agent a persistent POSIX filesystem with a real Unix toolchain inside the sandbox: cat, grep, find, pdftotext, ffmpeg.

Every Silvia user now has their own filesystem of memories, skills, and preferences. The agent decides the structure and writes to it across sessions. One user wants their portfolio checked against a specific allocation model every morning. Another wants weekly transaction summaries in a specific format. It builds on itself.

We believe 2026 is the year of the filesystem.

Now every developer can get started in a few lines of code: trovefiles.dev

English

Silvia retweetledi

What does building AI-native actually look like with @vxanand from @clay, @madhavjha from @emergentlabs and @shaincodes from @cfosilvia moderated by @laurenmhreeder from @sequoia

- be adaptable and plan for where the models are 6 months from now

- evals evals evals to help predict where your product can go as models get smarter

- don’t assume that if a big player is in the space, that space is checked off

- follow your curiosity, seek discomfort

English

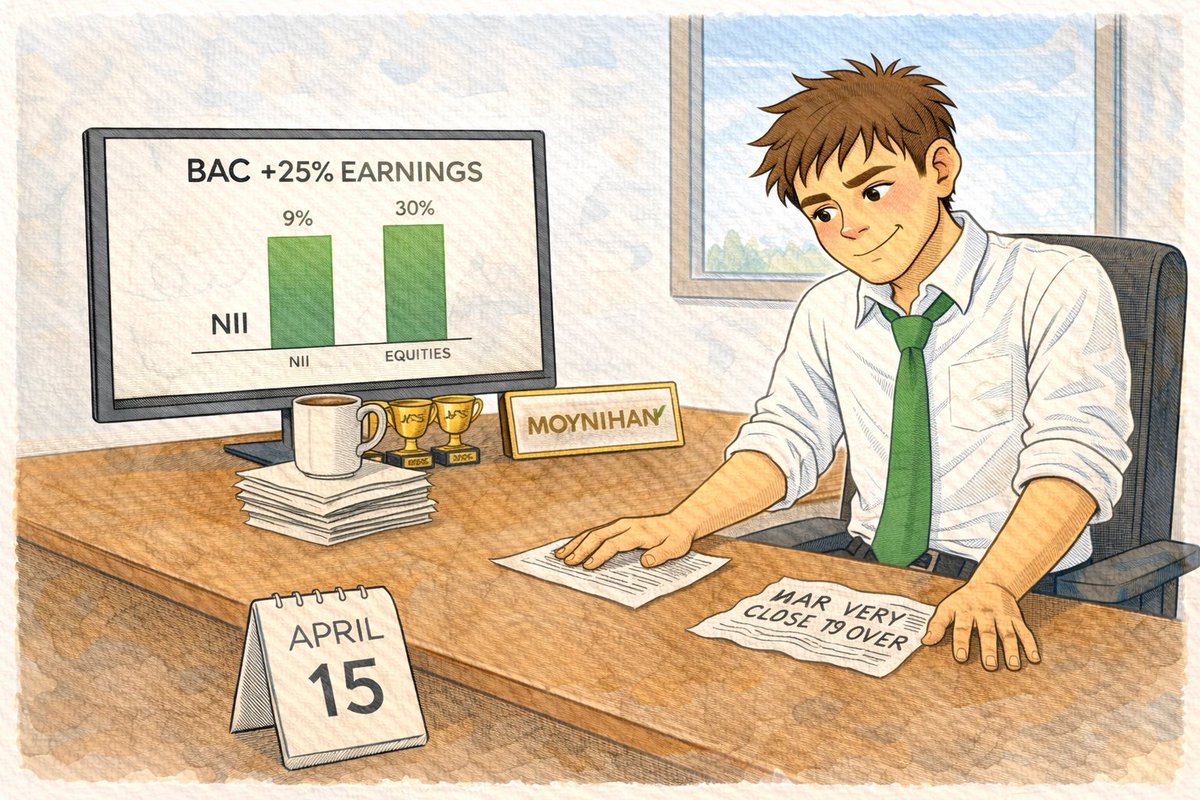

𝗕𝗔𝗖 (Bank of America Corporation) Q1 BEAT. EPS $1.11 against a $1.00 estimate, an 11% beat. Revenue $30.3 billion, topping consensus by $350 million. Net income $8.6 billion, up 25% year over year. Equities trading revenue surged 30%. CEO Brian Moynihan said consumer banking remains "healthy." That is five of six major banks this week reporting beats.

Three things that mattered.

1. Net interest income rose 9% to $15.9 billion. The rate environment that was supposed to compress bank margins after three Fed cuts in 2025 is instead expanding them. Loan growth and higher revolving balances on consumer credit cards are doing the work that higher rates used to do.

2. Equities trading revenue climbed 30%, the same story that produced records at JPM, GS, and Citi earlier this week. The Iran war volatility that hit consumers through gas prices has been a direct profit center for every bank's equity desk. The pattern is now unanimous across all five reporting banks.

3. Provision for credit losses fell to $1.3 billion from $1.5 billion the prior quarter. The consumer is not cracking under the oil shock. If anything, the credit quality data improved.

The bank earnings scorecard for the week: GS beat, JPM beat, C beat, BAC beat, WFC mixed. Five of six major banks posted clean beats. Every one flagged record or near-record trading revenues driven by geopolitical volatility. The market has its template for the quarter.

If you own BAC: the Q2 question is whether trading revenue holds if the Iran conflict de-escalates and volatility normalizes. The NII trend is the more durable story.

Own BAC? Silvia can break down what this means for your position. cfosilvia.com

English

𝗠𝗦 (Morgan Stanley) Q1 BEAT. EPS $3.43 against a $2.95 estimate, a 16% beat. Revenue $20.58 billion, a record quarter, topping consensus by $1.35 billion. Net income $5.57 billion, up 29% year over year. Trading revenue exceeded expectations by nearly $1 billion. That completes bank earnings week: six of six major banks beat.

Three things that mattered.

1. Record quarterly revenue at $20.58 billion, up 16% year over year. Morgan Stanley joins Goldman, JPMorgan, and Citigroup in posting record or near-record trading revenues this quarter. The equity desk was the engine, and the Iran war volatility was the fuel.

2. Trading revenue topped expectations by nearly $1 billion. That is not a rounding error. The Street modeled for a strong quarter and MS still delivered a billion dollars more. CEO Ted Pick's first full year is running ahead of every estimate.

3. This is the capstone result for bank earnings season. GS beat. JPM beat. C beat. BAC beat. WFC barely beat. MS beat the hardest. The pattern is unanimous: equity trading desks printed money on geopolitical volatility, and the consumer held. No one cracked.

Meanwhile, Trump said the Iran war is "very close to over" per Bloomberg, and the S&P sits within 1% of its all-time high of 7,002.28. The market is pricing peace, bank profits, and a rate path that still tilts toward cuts.

If you own MS: watch the wealth management division in Q2. Trading revenue is cyclical. The durability of the earnings stream depends on whether the $5.5 trillion AUM base keeps compounding fees even if volatility fades.

Own MS? Silvia can break down what this means for your position. cfosilvia.com

English

𝗧𝗨𝗘𝗦𝗗𝗔𝗬 𝗔𝗣𝗥𝗜𝗟 𝟭𝟰. S&P 500 surged 1.2% to within sight of a fresh record. Nasdaq posted a 10th straight day of gains, up 1.8%. Dow added 0.63%. Oil collapsed 7% to $92. Two days ago the US Navy blockaded the Strait of Hormuz. Today the market erased the entire blockade premium and then some. The tape is not afraid of this war anymore.

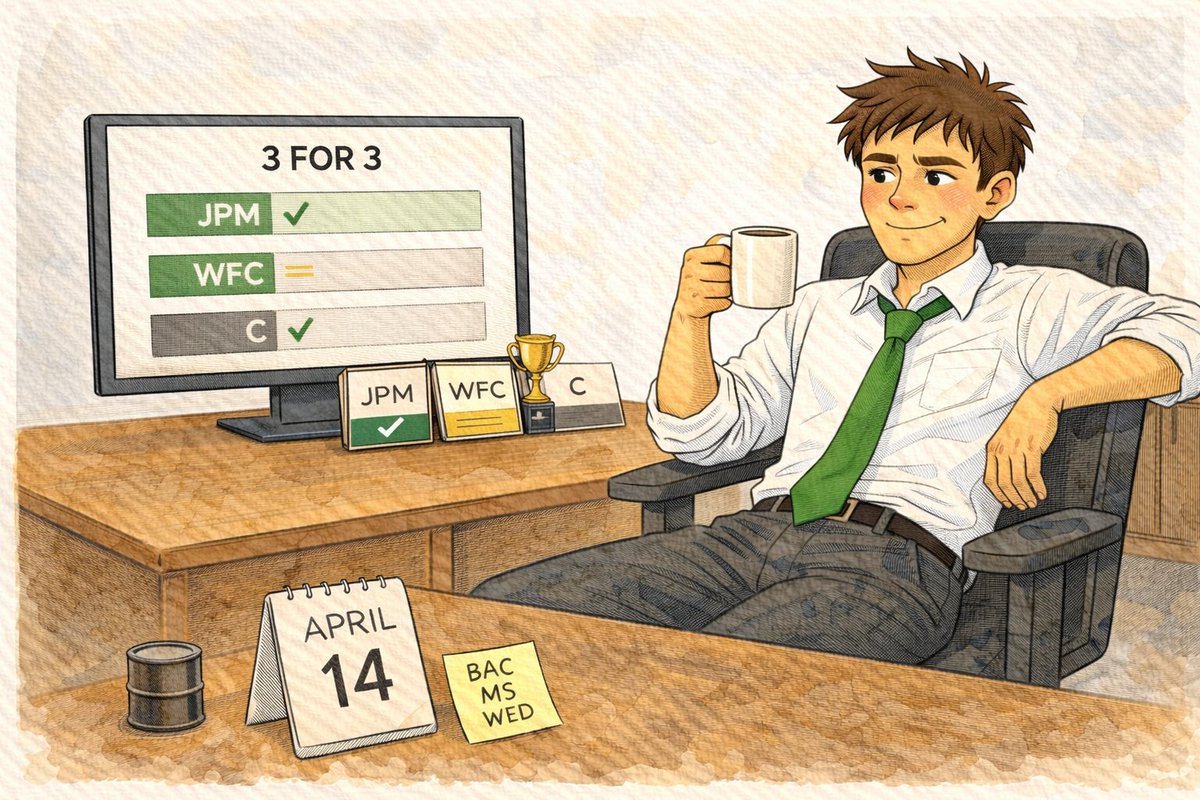

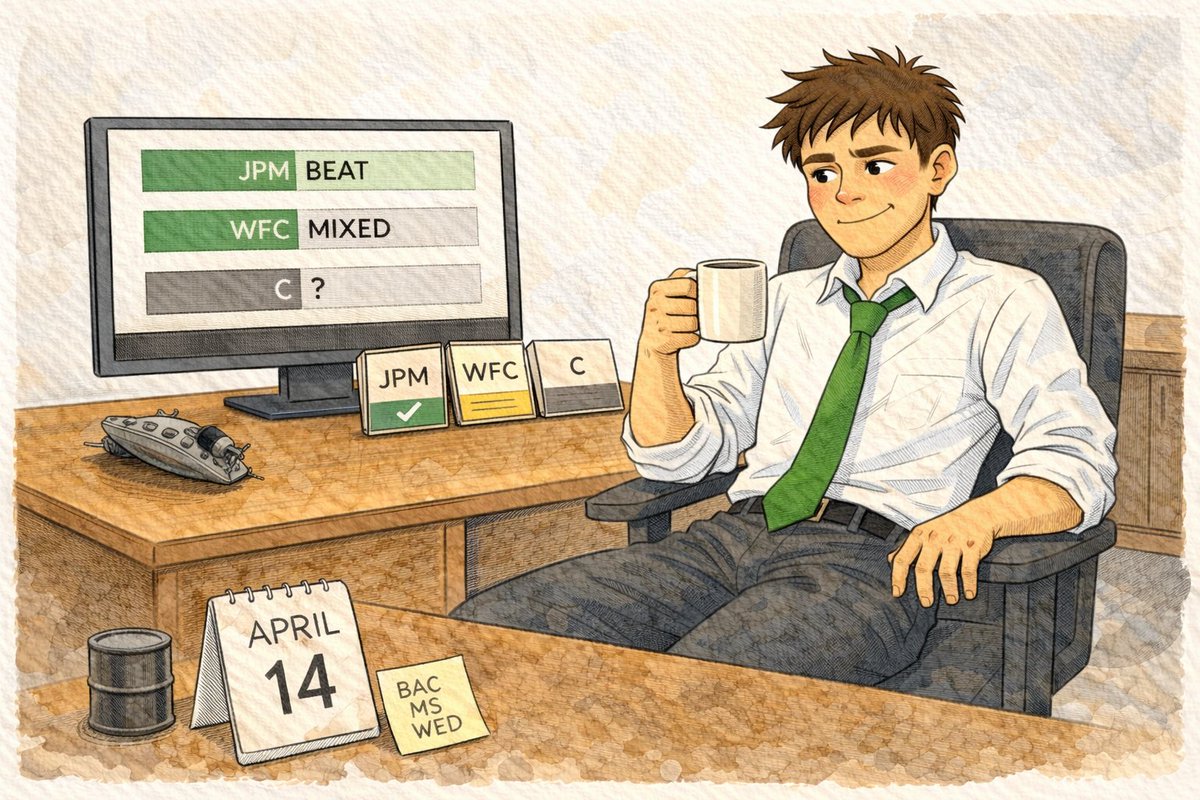

The banks set the tone before the open. JPMorgan posted Q1 EPS of $5.94 against a $5.45 estimate, a 9% beat. Net income $16.5 billion, up 13%. Markets revenue hit a record. Citigroup beat even harder: $3.06 EPS against $2.63, a 16% beat on the strongest quarter in a decade. Revenue topped consensus by over $1 billion. Net income grew 42%. Wells Fargo barely beat EPS at $1.60 versus $1.59 but missed revenue at $21.45 billion versus $21.77 billion expected.

The pattern across all four banks this week is clear. Trading desks are printing money on Iran war volatility. Equity desks hit records at both JPM and GS. The banks with the strongest markets franchises are pulling ahead. FICC results are mixed, with Citi's fixed income up 10% and Goldman's down 10%, which tells you the fixed income story is bank-specific, not sector-wide.

PPI March came in at 0.5% month over month and 4.0% year over year. Energy jumped 8.5%. Services were unchanged. The same CPI story from last Friday: hot headline from oil, calm underneath. The market read through it again.

Oil is the real story. WTI fell from $104 on Monday to $92 on Tuesday, a 12% reversal in 24 hours. Pakistan is arranging a second round of US-Iran talks. The ceasefire expires April 22, one week from today. The market is pricing a deal getting done before the deadline. If that read is wrong and the ceasefire collapses, oil retests $100 within days.

Gold, Bitcoin, and Treasury yield data pending final settlement. The 10-day Nasdaq winning streak is the longest since November 2024.

Tomorrow: Bank of America and Morgan Stanley report Q1 before the open. If BAC and MS confirm the trading desk thesis, the bank earnings verdict is unanimous.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗖 (Citigroup Inc.) Q1 BEAT. EPS $3.06 against a $2.63 estimate, a 16% beat. Revenue $24.63 billion, topping consensus by over $1 billion. Highest quarterly revenue in a decade. Markets division hit record revenues. Stock up 1.5% in pre-market.

Three things that mattered.

1. Fixed income revenues rose roughly 10% year over year despite weakness in commodities. That is the opposite of what Goldman showed Monday, where FICC fell 10%. Citi's fixed income desk outperformed the Street's expectations by a wide margin, and the divergence between C and GS on this line tells you the FICC story is bank-specific, not sector-wide.

2. The $1 billion revenue beat is the largest among the three banks reporting today. JPM beat revenue by roughly $670 million. WFC missed revenue by $320 million. Citi's outperformance came from broad strength across the franchise.

3. This is the third bank to report this week. JPM beat clean. WFC barely beat EPS and missed revenue. Citi beat both lines by the widest margin. The pattern: trading desks are printing money on Iran war volatility, and the banks with the strongest markets franchises are pulling ahead.

If you own C: the earnings call will address whether the FICC strength is sustainable or a one-quarter war volatility windfall. Watch for commentary on the Hormuz blockade impact on trading volumes.

Own C? Silvia can break down what this means for your position. cfosilvia.com

English

𝗝𝗣𝗠 (JPMorgan Chase & Co.) Q1 BEAT. EPS $5.94 against a $5.45 estimate, a 9% beat. Revenue $49.8 billion against $49.13 billion expected. Net income $16.5 billion, up 13% year over year. The largest US bank just set the tone for bank earnings season, and the tone is bullish.

Three things that mattered.

1. Markets revenue hit a record quarter. The Iran war volatility that Goldman also flagged Monday has been a profit center for every major trading desk. JPM captured the same flow that pushed GS equities up 27%, and the record here confirms it was not a one-bank story.

2. Managed revenue reached $50.5 billion, up 10% year over year. Advisory and equity underwriting both improved, capturing a more active deal and capital markets backdrop. The investment banking recovery that stalled in 2024 is gaining traction.

3. Deposit growth and higher revolving credit balances point to a consumer that is still spending, even with gas at $4 and oil above $100. This is the data point the bears needed to see crack, and it did not.

Wells Fargo reported alongside JPM. EPS $1.60 barely beat the $1.59 estimate. Revenue $21.45 billion missed the $21.77 billion consensus. Net interest income rose 5%, noninterest income 8%. WFC is a narrow beat that tells you less than JPM's clean one.

If you own JPM: the question for the next quarter is whether the trading desk prints another record if the Iran conflict de-escalates, or whether the volatility premium fades with it. The earnings call will address the Hormuz blockade directly.

Own JPM? Silvia can break down what this means for your position. cfosilvia.com

English

Silvia retweetledi

@ebloch Anyone who was using Hiro can move their data and assets to @cfosilvia

We have more than $30 billion of assets on the platform in less than a year and we are one of the fastest growing fintech products in the country.

Try it: cfosilvia.com

English

𝗠𝗢𝗡𝗗𝗔𝗬 𝗔𝗣𝗥𝗜𝗟 𝟭𝟯. S&P 500 closed at 6,886.24, up 1.02%. That is the highest reading since before the Iran war started on February 28. The tape absorbed a naval blockade of the world's most important oil chokepoint, an 8% spike in crude to $104, and a FICC miss from the first bank to report, and still rallied to a six-week high. The Dow gained 0.63%. Nasdaq climbed 1.23%.

Futures dropped 1% overnight on Trump's Hormuz blockade announcement. By 10 AM the Navy was enforcing it. Three tankers tested the passage near the Iranian coast. Iran claims it turned them back. CENTCOM said it is establishing a new shipping lane and deploying underwater drones. Trump warned Iranian ships near the blockade would be "eliminated." The ceasefire technically holds. It expires April 22, nine days out.

Oil told one story, equities told another. WTI surged 8% to $104.93. Brent rose 7% to $102.17. The market priced the blockade as a negotiating tool, not a permanent closure. If the read is wrong, oil retests $110 and the tape reprices. If the read is right, the last six weeks of war premium continue unwinding.

Goldman Sachs reported Q1 earnings before the open. EPS $17.55 against a $16.34 estimate, a 7.4% beat. Net revenues $17.23 billion, up 14%. Equities trading hit a record, up 27%. Investment banking fees surged 48%. FICC fell 10% to $4.01 billion, missing by $855 million. The stock opened down 4%, then pared to close down roughly 2%. CEO David Solomon's positive comments on software stocks after the recent AI selloff helped lift the broader market in the afternoon session.

Gold fell 0.7% to around $4,720 as rising oil reinforced expectations that rates stay higher longer. Bitcoin slipped to roughly $71,000. The 10-year yield moved higher on inflation expectations.

Tomorrow: JPMorgan, Wells Fargo, and Citigroup report Q1 earnings before the open. Three of the five largest US banks in a single morning. JPM consensus: $5.41 EPS on $48.2 billion revenue. If the banks confirm what Goldman showed today, that trading desks are printing money on war volatility while FICC softens, the market has its template for the quarter.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗛𝗢𝗥𝗠𝗨𝗭 𝗕𝗟𝗢𝗖𝗞𝗔𝗗𝗘 DAY 1. The US Navy began enforcing a full blockade of Iranian ports at 10 AM ET. WTI surged 8% to $104. The S&P 500 barely flinched, finishing the afternoon session near flat at 6,824. The eight-session winning streak ended, but it ended with a whisper on a day that should have been a scream.

Three tankers attempted to transit the strait by sailing close to the Iranian coast, the first vessels to try since the blockade was announced. Iran's Revolutionary Guards released footage of a radio exchange with a US destroyer, warning it would be targeted if it continued approaching. This is a standoff in real time.

The tape is telling you something the headlines are not. Futures dropped 1% overnight on the blockade announcement. By midday the S&P had recovered nearly all of it. Nasdaq was up 0.34%. The only major drag was Goldman Sachs, down 3.55% on a FICC miss that had nothing to do with geopolitics.

Oil at $104 is elevated but not panicking. WTI sat at $97 on Friday. It hit $112 at the war's peak. The market is pricing the blockade as a negotiating tool, not a permanent closure. If that read is wrong and the IRGC confrontation with the Navy escalates, the floor disappears fast.

The ceasefire expires April 22. The tankers testing the blockade today are the lead indicator. If they pass, the blockade is soft. If they are turned back, oil retests $110 and the tape reprices.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗚𝗦 (Goldman Sachs Group) Q1 BEAT, FICC MISS. EPS $17.55 against a $16.34 estimate, a 7.4% beat. Net revenues $17.23 billion, up 14% year over year. Net earnings $5.63 billion, up 19%. Return on equity 19.8%. The headline numbers are clean. The stock is down 3% in pre-market anyway.

Three things that mattered.

1. Equities trading hit a record quarter with revenues up 27%. The Iran war volatility that crushed the real economy was a profit center for the trading desk. Client activity surged on the geopolitical uncertainty, and Goldman's equity franchise captured the flow.

2. Investment banking fees jumped 48% to $1.5 billion. M&A advisory drove the increase. The dealmaking pipeline is recovering from the 2023-2024 freeze, and Goldman is taking share on the rebound.

3. FICC revenues fell 10% to $4.01 billion, missing expectations by roughly $855 million. Rates, mortgages, and credit intermediation weakened. Commodities and currencies partially offset the decline but could not close the gap. This is the number the market is selling.

Asset and wealth management revenues grew 10% to $4.08 billion. Assets under supervision reached a record $3.65 trillion. The annuity stream is building, but it is not the revenue line anyone trades on today.

If you own GS: the question for the next quarter is whether FICC recovers as Hormuz volatility intensifies or whether the rates business stays soft with the Fed on hold. The earnings call at 9:30 AM ET will set the tone.

Own GS? Silvia can break down what this means for your position. cfosilvia.com

English

𝗧𝗥𝗨𝗠𝗣 𝗢𝗥𝗗𝗘𝗥𝗦 𝗛𝗢𝗥𝗠𝗨𝗭 𝗕𝗟𝗢𝗖𝗞𝗔𝗗𝗘. Hours after 21 hours of Islamabad talks produced no deal, Trump posted on Truth Social: "Effective immediately, the United States Navy will begin the process of BLOCKADING any and all Ships trying to enter, or leave, the Strait of Hormuz." He also ordered the Navy to "seek and interdict every vessel in International Waters that has paid a toll to Iran."

Read that twice. Iran has been blocking Hormuz for six weeks. Now the US is counter-blockading it. The strait that carries 20% of the world's oil is now closed from both directions.

Trump called Iran's toll-charging plan "extortion." His response is to make the waterway unusable for anyone until Iran drops the tolls and comes back to the table. More than 600 vessels including 325 tankers are already stranded. This order adds the US Navy to the chokepoint.

The two-week ceasefire technically holds. It expires around April 22, ten days out. But a naval blockade of the world's most important oil chokepoint is not the behavior of a country at peace. This is pressure, not diplomacy.

Monday's open will price this in. Oil was $97 at Friday's close. Before the ceasefire, WTI was above $110. A US counter-blockade puts the floor back under oil at $100 minimum and the ceiling is wherever the Navy takes it. The S&P's eight-session winning streak was already fragile after a no-deal weekend. This is the tape's first real gut check since the ceasefire rally started.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗜𝗦𝗟𝗔𝗠𝗔𝗕𝗔𝗗 𝗧𝗔𝗟𝗞𝗦 NO DEAL. After 21 hours of direct negotiations across two days, VP Vance told reporters, "We have not reached an agreement." The first face-to-face US-Iran talks since 1979 ended without a resolution. Nuclear enrichment was the wall.

Vance said the US needs "an affirmative commitment that they will not seek a nuclear weapon, and they will not seek the tools that would enable them to quickly achieve a nuclear weapon." Iran rejected those terms. Tehran demanded control of the Strait of Hormuz, the release of $6 billion in frozen assets, war reparations, and a ceasefire covering all of Lebanon. The US said no to all four.

Iran's foreign ministry framed it differently: "From the beginning, we should not have expected to reach an agreement in a single session." Parliament Speaker Ghalibaf added: "The US has understood Iran's logic. It is time for them to decide whether they can earn our trust or not."

The two-week ceasefire still holds. It expires around April 22, ten days from today. Pakistan's FM Ishaq Dar said Islamabad will try to facilitate new dialogue in the coming days. The US is already clearing mines from the Strait of Hormuz unilaterally, signaling it does not intend to wait for Iran's permission.

Here is what Monday trades on. The ceasefire holds but the deadline is ticking. No Hormuz agreement means the 600 stranded tankers stay put and oil stays elevated. But neither side walked away hostile. The door is open. The clock is the problem, not the room.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗜𝗦𝗟𝗔𝗠𝗔𝗕𝗔𝗗 𝗧𝗔𝗟𝗞𝗦 DAY 1. The United States and Iran sat across from each other Saturday for the first direct talks since the 1979 Islamic Revolution. That is 47 years of silence broken in a two-hour session in Pakistan's capital. VP Vance, envoy Witkoff, and Kushner on one side. Iran's parliamentary speaker Ghalibaf and FM Araghchi on the other. Pakistan mediated.

Phase 1 concluded Saturday evening. Both sides are now exchanging written texts to formalize what was discussed. Sources say there has been progress on a Lebanon ceasefire framework, with a possible understanding to limit Israeli strikes to southern Lebanon. There are signals of movement on unfreezing Iranian assets. No formal agreements have been confirmed by either side.

The hard issues remain open. Iran's 10-point proposal demands control of the Strait of Hormuz, an end to all sanctions, and the right to enrich uranium. The US 15-point counter wants nuclear restrictions and full Hormuz reopening. The gap is wide. The two-week ceasefire clock expires around April 22.

Here is what matters for Monday. If Phase 2 on Sunday produces a Hormuz agreement or a ceasefire extension, expect oil to drop and futures to rally at the open. If talks stall or collapse, oil retests $100 and the week starts defensive. The S&P closed Friday on an eight-session winning streak at 6,828.01, up 3% for the week. The tape is priced for progress, not failure.

The 600 tankers still stranded in the Gulf are the real scoreboard. Until they move, nothing is solved.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

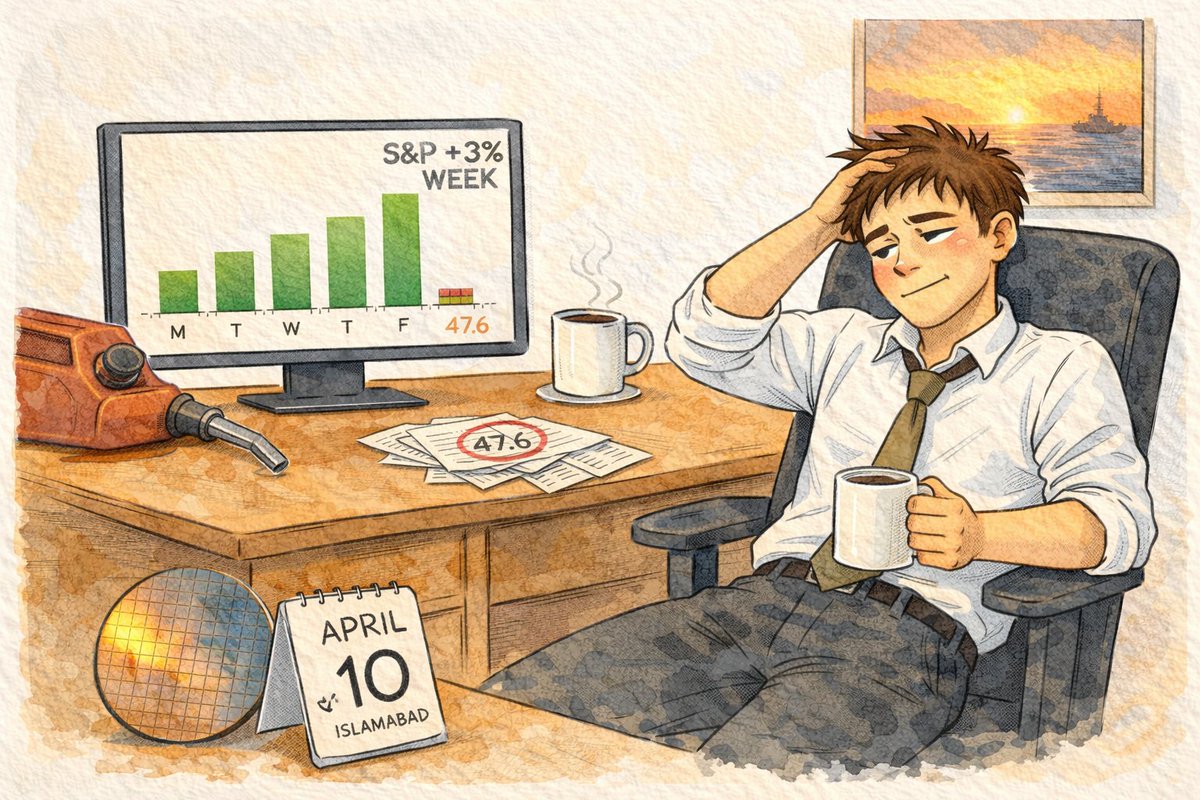

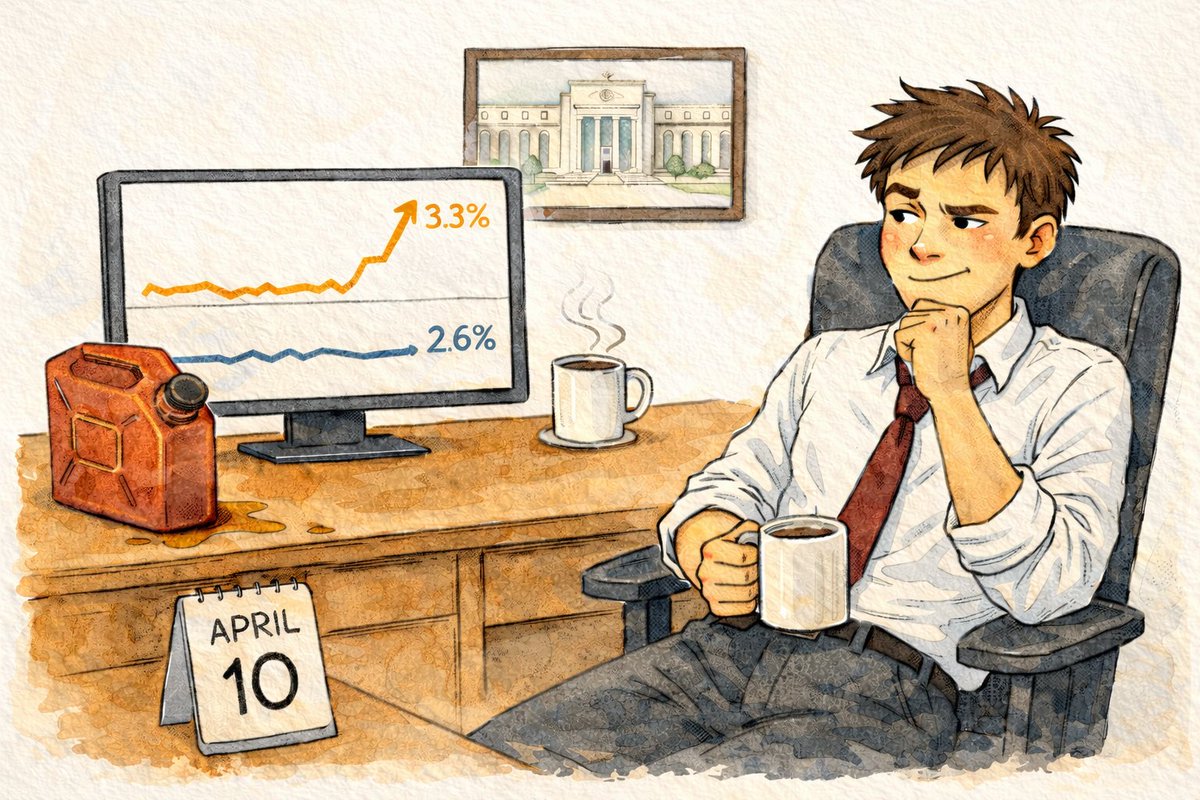

𝗙𝗥𝗜𝗗𝗔𝗬 𝗔𝗣𝗥𝗜𝗟 𝟭𝟬. S&P 500 closed at 6,828.01, up 0.05%. Eight straight winning sessions, but this one came on fumes. The tape opened green on a soft core CPI print, faded all afternoon on record-low consumer sentiment and Trump threatening military action if weekend talks fail. The Dow lost 147 points to 48,038.94, down 0.30%. Nasdaq held on, up 0.37% to 22,907.20.

The morning belonged to inflation data. March CPI came in at 3.3% headline year over year, below the 3.4% FactSet consensus. The scary headline was all gasoline: the gas index surged 21.2% in a single month, the largest increase since the BLS began tracking it in 1967. Strip energy out and core CPI printed 2.6% against 2.7% expected. The 10-year yield dropped to 4.23% from Thursday's 4.29%, reading the soft core correctly.

The afternoon belonged to the consumer. The University of Michigan's preliminary April sentiment reading collapsed to 47.6, the lowest in the survey's 74-year history. Consensus was 52.0. One-year inflation expectations jumped to 4.8% from 3.8%, the largest single-month move on record. The critical footnote: 98% of interviews were conducted before the ceasefire was announced on April 7. This number captures peak war panic, not the current reality.

TSMC reported record Q1 revenue of $35.6 billion, up 35% year over year, beating estimates. AI chip demand is not slowing. Broadcom gained 4.69%. But the software side took heavy losses: ServiceNow fell 8%, Palo Alto Networks 7%, Cloudflare 11%. The AI trade is splitting into hardware winners and software losers.

Oil held near $97 with the Strait of Hormuz still effectively closed. More than 600 vessels including 325 tankers remain stranded. Only six transited Thursday versus a normal 120 to 140 per day. Gold slipped 0.30% to $4,749. Bitcoin gained 1.05% to around $73,094.

For the week: S&P gained more than 3%, Nasdaq more than 4%. Second straight winning week. Oil fell roughly 10% from Monday's open. The ceasefire-driven relief rally carried the tape even as cracks appeared underneath.

This weekend: VP Vance leads talks with Iran in Islamabad starting Saturday. Netanyahu authorized direct talks with Lebanon but will not halt strikes on Hezbollah. Trump said warships are ready if negotiations fail. Tuesday brings JPMorgan, Wells Fargo, and Citigroup Q1 earnings, the first major test of bank profitability under the Iran war economy.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗨𝗠𝗜𝗖𝗛 𝗖𝗢𝗡𝗦𝗨𝗠𝗘𝗥 𝗦𝗘𝗡𝗧𝗜𝗠𝗘𝗡𝗧 RECORD LOW. Preliminary April reading came in at 47.6, the lowest in the survey's 74-year history. Consensus was 52.0. March was 53.3. That is an 11% collapse in a single month, and it broke the record set during the peak of Biden-era inflation in June 2022.

What drove it: the gas pump. One-year inflation expectations surged to 4.8% from 3.8% in March, the largest single-month jump in the survey's history. Five-year expectations climbed to 3.4% from 3.2%. Consumers have internalized the Iran war energy shock. Gasoline prices rose nearly 40% in six weeks, crossing $4.16 per gallon nationwide.

Here is the critical context: 98% of interviews were completed before the ceasefire was announced on April 7. This number captures the worst of the war panic, not the current reality. Survey director Joanne Hsu noted that "many consumers blame the Iran conflict for unfavorable changes to the economy." The April 24 final reading will include post-ceasefire interviews and should recover some ground.

The number that matters more than 47.6 is 4.8%. The Fed watches UMich inflation expectations closely. If consumers believe prices are running hot, it becomes self-fulfilling through wage demands and spending behavior. The cool 2.6% core CPI this morning gave the doves a talking point. The 4.8% inflation expectations number takes it away.

What to watch: Iran-US talks in Islamabad Saturday. If the Strait of Hormuz reopens, the gas pump pressure eases and both sentiment and inflation expectations reverse. If it does not, 4.8% becomes the baseline.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗠𝗔𝗥𝗖𝗛 𝗖𝗣𝗜 HOT HEADLINE, COOL CORE. Consumer prices rose 3.3% year over year, the highest since May 2024. But core CPI, the number the Fed actually watches, came in at 2.6% against 2.7% consensus. One number screams. The other whispers. The market heard the whisper.

Gasoline did all the work. The gasoline index surged 21.2% in a single month, the largest increase since the Bureau of Labor Statistics started tracking the series in 1967. Energy overall rose 10.9%, the biggest monthly jump since September 2005. Fuel oil climbed 30.7%. Airline fares added 2.7% as jet fuel costs passed through. Food was flat at 0.0%.

Strip the Iran war energy shock out, and you get a core print that actually cooled: 0.2% month over month against 0.3% expected, 2.6% year over year against 2.7% expected. Both below consensus. That is the number that matters for rate policy.

Market reaction tells the story. Nasdaq rallied 0.54% to 22,944. S&P gained 0.14% to 6,834. The 10-year yield dropped to 4.23% from Thursday's 4.29%, pricing in the soft core. WTI crude held flat near $97. The tape read through the headline noise.

Polymarket now prices 37% odds of zero Fed cuts in 2026, 26% for one cut. The soft core keeps June alive, but barely. The next catalyst is this weekend's Iran-US talks. If the Strait of Hormuz reopens, April's energy component normalizes. If it does not, Oxford Economics says headline CPI could top 4% next month.

What does this mean for your portfolio? Ask Silvia. cfosilvia.com

English

𝗧𝗛𝗨𝗥𝗦𝗗𝗔𝗬 𝗔𝗣𝗥𝗜𝗟 𝟵. S&P 500 closed at 6,824.65, up 0.62%. Dow added 276 points to 48,185.99, up 0.58%. Nasdaq climbed 0.83% to 22,822.42. The tape absorbed a morning that had every reason to go red and closed green anyway. That is the story of the session.

The morning was ugly. PCE February printed hot at 2.8% headline and 3.0% core, both above consensus, giving the hawks their own proof point the day after the doves got the weak February payroll number. Then Iran's parliamentary speaker accused the US of violating three of the ten ceasefire conditions, Trump signaled strikes could resume, and the White House hardened its position that the ceasefire does not cover Lebanon. WTI popped 6% to touch $101 by 10 AM.

By 3 PM, the tape had eaten all of it. Oil pulled back to around $97.50 from the intraday high. The Dow turned positive. Nasdaq led the afternoon on a broad tech bid. The market is telling you it already priced the ceasefire fragility and is looking past it toward next week.

Intel was the single-stock story of the day. The company announced a multi-year Google collaboration on Xeon processors and custom IPUs, pushing INTC up 2.39% and extending the year-to-date gain to 62%. That is Intel's second AI tailwind in two days, after joining Tesla's Terafab project on Wednesday. Two concrete commercial wins now sit under the comeback narrative.

Laggards: Salesforce -3.88%, IBM -2.3%, Microsoft -1.33%. Software traded heavy on the day, a notable weak spot in an otherwise green tape. Gold gained 0.41% to $4,797 as the dollar softened and real yields stayed flat. 10-year Treasury yield closed at 4.29%, essentially unchanged. Bitcoin ticked higher on the risk-on bid.

Tomorrow: March CPI at 8:30 AM ET. FactSet consensus sits near 3.7% headline year over year, with core closer to 2.7%. The headline number will carry the Iran-driven energy spike. The core number is what the Fed will watch. A core print at or below 2.7% on top of today's tape probably pushes June cut odds back above 60%. A hot core on top of yesterday's hot PCE sends them below 40%.

What does this mean for your portfolio? Ask Silvia. has

English

𝗜𝗡𝗧𝗖 (Intel) GOOGLE DEAL. Multi-year collaboration on Xeon processors and custom IPUs for Google's data centers. Stock up 2.39% on the news and up 62% year-to-date. This is Intel's second AI tailwind in two days. Tesla Terafab yesterday sent the stock +11.42%, Google's commitment extends the narrative.

What the deal actually covers.

1. Google will use Intel's latest Xeon 6 processors across its global cloud and AI infrastructure. Multi-generational alignment means the commitment runs through future Xeon generations, not just the current chip.

2. Google will customize Intel's IPUs, the infrastructure processing units that handle networking, security, and storage inside data centers. Custom silicon for Google is notable because Google has preferred its own TPUs over third-party accelerators.

3. Neither side disclosed dollar amounts, unit volumes, or contract length. Without a number, the market is pricing enthusiasm, not cash flow. The modest 2.39% move reflects that ambiguity.

The context: Intel has been the left-behind name in the AI trade for three years while Nvidia, AMD, and Broadcom sprinted. The foundry rebuild cost billions. Yesterday's Musk Terafab deal and today's Google deal are the first two concrete commercial wins that suggest the rebuild might pay back.

What to watch: whether the deal shows up as a disclosed revenue line in Intel's next earnings call. Quantified commitments mean a second leg. Unquantified commitments mean this week was sentiment.

If you own INTC, the year-to-date +62% is now partly backed by concrete customer wins rather than pure AI sentiment.

Own INTC? Silvia can break down what this means for your position. cfosilvia.com

English