Cin3 PPKING

63 posts

5月4日16点

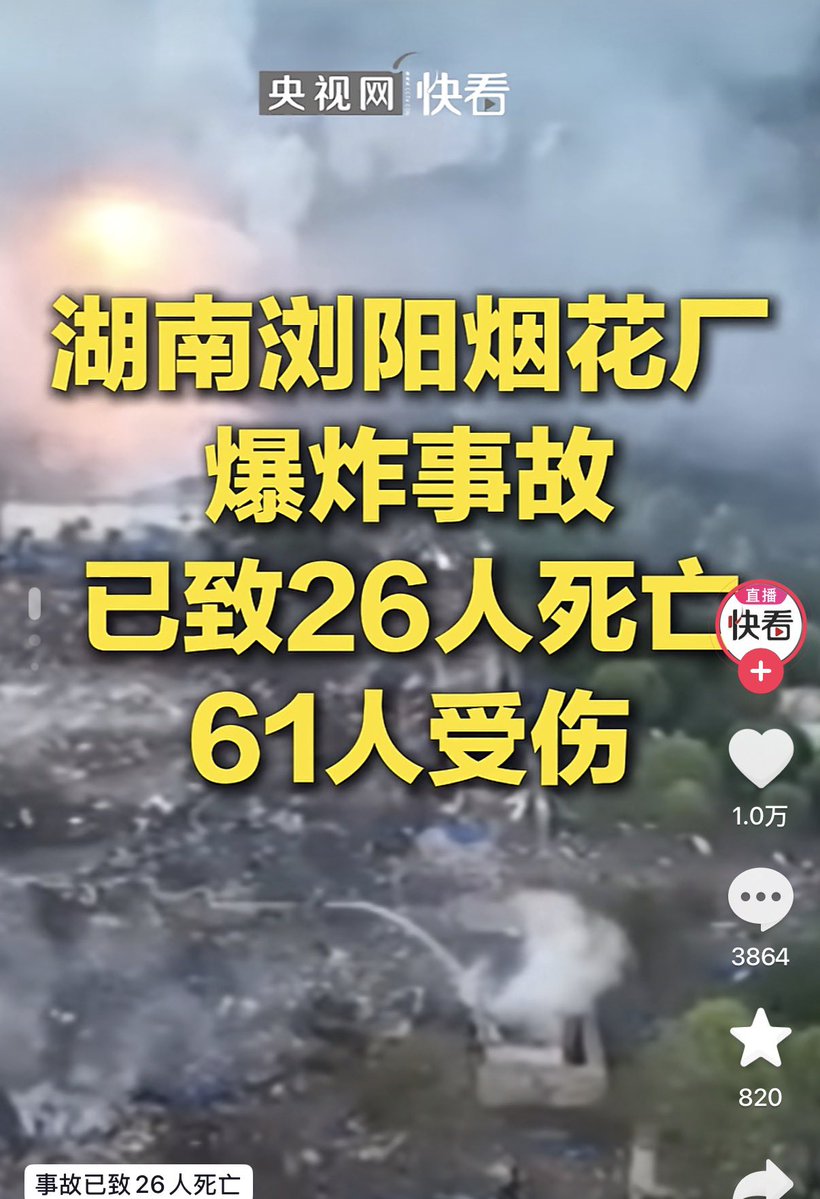

湖南浏阳烟花厂大爆炸‼️

官方说目前26死,61伤‼️😱

目前工厂还有两个黑火药库没爆🙀

航拍看,整个周边区域全部夷为平地‼️

威力堪比当年天津大爆炸

(天津当年死了173个)

讽刺的是,如此大的事故

人们还没来得及哀悼

当地人已经开始自发网络控评……

要求不要发视频影响当地……

湖南浏阳是中国的“花炮之乡”

30万以上从业人员。2025年产值超500亿元人民币

我相信这些人真的是自发控评

我不知道应该谴责他们还是同情他们

哎🙁😮💨……

中文

$IREN -> Last night @mikealfred mentioned analysts and investors are still missing the forest for the trees on IREN's ambitions. There's a number of ways to interpret what that means, but my takeaway is the IREN community is too focused on signing deals for site hosting, while the IREN team is actually focused on cloud hosting themselves at scale.

Why? ->

- Ask yourself two questions, 1) if HS are willing to pay this much for compute, how much margins do they stand to gain that IREN could otherwise capture themselves? 2) if we are as constrained on compute as everyone says, is there not room for another HS that has such compute available?

- Mike has hinted at this repeatedly, but often gets brushed aside as the more "realistic" and immediate payoff is site hosting only.

- a $1 Trillion MC is really only achievable if they go down this route, and are successful.

- $IREN would be the ONLY fully vertically integrated offering in the market

- Recent heavy marketing in Australia and on the PGA tour are not necessary for site hosting only, clearly they want their name to reach beyond those seeking infrastructure

- B300 GPU purchase without a contracted customer... a tell

How? ->

- Power: @FransBakker9812 has prudently identified another 6-8GW IREN may be working on actively. I also wouldn't be shocked if IREN looks to acquisitions in the space to further grow the pipeline.

- Software: @danroberts0101 has already mentioned IREN is working a multi billion dollar deal that includes the software stack. I can't speak to how much expertise they have in house, but they do have posted roles for Software Engineers, Solutions Architect, Enterprise Systems Engineer, etc.

- Sales: this is the biggest question mark for me. IREN isn't hiring at all on the BD front. Might be strategically hiding this expertise buildout but it's the one aspect of this HS journey that isn't clear to me yet. Also might just be the easiest resource to buildout when it's necessary to do so (avoid cash burn in the meantime)

- Capital: a separate post would be required for this, but $6B ATM would be another tell here. No one thought that much was needed for their current picks/shovels business model approach with HS pre-paying so aggressively.

Welcome thoughts/challenges on this. Excited to see what Earnings holds.

₿itcoin ₿utcher 🥩 🐑 🐷@bitcoinbutcher1

English

@FransBakker9812 Since beginning of 2026:

#NBIS +86%

#CRWV +66%

#IREN +20%

Which is the worst? just simply waste of time on IREN. It’s not neo cloud it’s still bitcoin manier.

English

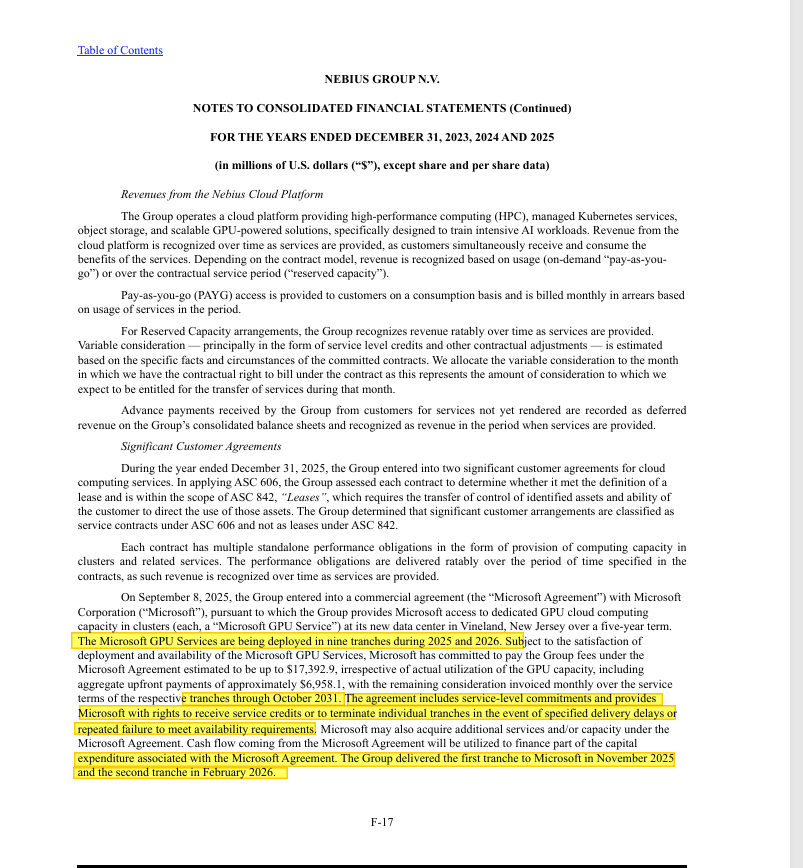

Since everyone is dying to hear my thoughts on the 40% prepayment $NBIS got for their contract with $MSFT, I will say this much:

Nebius has agreed to deliver a contract valued at almost 2x that of $IREN, in a relative similar time period.

Microsoft is the ultimate beneficiary of the compute, and the topline means as much as it will translate to GPU hours for them, and that solves their capacity constraints.

Without going into the details about how many GPUs it may be (which we don't know, but estimates are pricing it around the same level as $IREN), $MSFT is still getting a lot more GPU hour instances from $NBIS, to be delivered throughout 2025-2026.

So, Nebius agreed to solve 2x the constraint for Microsoft relative to $IREN who UNDERSUBSCRIBED their Horizon footprint, to go with GB300 to match the similar timeline that Nebius was requested.

In other words:

Nebius was more cooperative (provided more GPUs, more capacity, and ultimately more GPU hour instances).

Nebius agreed to supply much more contract value, and compute, by the end of 2026.

And was awarded 2x the prepayment % as a result.

So, I am not salty, in tears, or otherwise complaining.

Nebius got a good deal on their capex, and this is fair considering their agreed to capacity.

I say fair, because I think it's proportional to their agreed to GPU hours, relative to Iren who is handicapping $MSFT with a fixed rack qty design in Horizon.

So 20% for 9.7B and 40% for 17.##B is proportional, and not something I worry about.

Nebius held up their end in negotiations and got the prepayment that fits a high profile, high capacity, high risk build-out.

They delivered 2 out of the original 9 tranches. And now they have to hold up their end on the delivery of the other 7 this year.

Don't forget that Microsoft is the one who agrees to pay up front. If you solve a bigger problem for them, they are not too shabby to pay up front proportionally.

English

@mindofzen_ Since beginning of 2026:

#NBIS +86%

#CRWV +66%

#IREN +20%

Which is the worst? just simply waste of time on IREN. It’s not neo cloud it’s still bitcoin manier.

English

Seems way too obvious of a trade but maybe it's that simple, 200 MW of capacity contracted with ~2 GW of capacity being currently built/available. Stock has been digesting the initial move 9 months.

Company mentioned multiple advanced negotiations in their last ER call.

$IREN

zen@mindofzen_

$IREN

English

$NBIS got 40% Pre-Payment for the Microsoft deal.

That's great for all bare-metal players. $IREN $CRWV

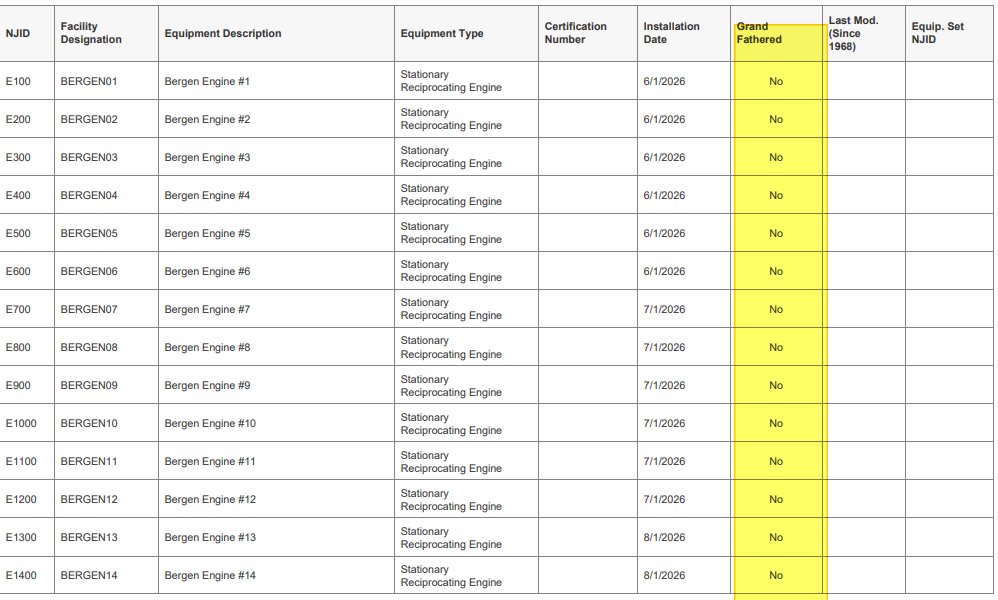

But here is my concern around Vineland

1. Execution:

If vineland is only pulling 5MW from the the local grid and thermal images seem to show no heat remittance, then where did they actually deliver those two tranches.

(See Attached)

The bergin engines does not have air-permit approval, and they cant operate 27/32 engines at 90% base load without them. They were installed on 6/1/2026 through january. They are not grandfathered.

(See Attached)

Does it say anywhere in Q2/Q3, 20-F and response to FT it was delivered from the Vineland datacenter, no.

I assume they might have have used finland for the 2nd tranche since it was expanded for liquid cooled GPU's beginning 2026, which is inline with the 2nd tranche feb 2026 delivery. They must have used another datacenter for the first tranche.

Also how will they deliver 7 tranches in 6 months if the first 2 tranches took 5 months. This is assuming there is no delays from the air-permits.

2. Failure to meet Tranches

If Nebius is delayed or can’t deliver capacity, they don’t immediately lose the Microsoft contract, but they start taking hits in stages: first service credits (financial penalties), then reduced revenue if capacity isn’t available, and eventually Microsoft can terminate individual tranches and stop paying for them.

Since they’ve already delivered the first two tranches, they’re not in trouble yet, but if they can’t scale future tranches especially without Vineland coming online they risk losing significant long-term revenue and weakening the overall deal, even if the upfront payments are already secured

English

@DustinHuntwn Since beginning of 2026:

#NBIS +86%

#CRWV +66%

#IREN +20%

Which is the worst? just simply waste of time on IREN. It’s not neo cloud it’s still bitcoin manier.

English

$IREN

1. we sell when the power is ready.

2. we know the price only goes up.

3. we don't lease, we own.

I hope they wait until after the ER for any announcement. Bitcoin still a factor in ER. Let's get it out of the way.

It could legitimately even go higher than that once they start banking Microsoft revenue too, along with potential expansion at the future Horizon 5-10. Once the market starts to see it's a repeatable process the OK 1.6GW will start to get priced in too. Crazy shit

They'll likely have offers for the entire projected operation now that they've delivered on a major promise. The pivot will finally be in.

Like if you STILL believe $IREN.

Also you can follow me,I'll be updating you with the latest info on $IREN and more related content.

English

Bullish $IREN

“Maybe Neo-Clouds will see a re-rating? ”

“If there’s a global supply crunch in new compute and mad scramble for every bit of new capacity that could be brought online, the existing compute companies like the “Neoclouds” that are already installed or about to be become much more valuable, no matter how terrible their unit economics might’ve previously seemed, right?”

Zephyr@zephyr_z9

many are saying this

English

Since beginning of 2026:

#NBIS +86%

#CRWV +66%

#IREN +20%

Which is the worst? just simply waste of time on IREN. It’s not neo cloud it’s still bitcoin manier.

@danroberts0101 @mikealfred

English

Maybe it’s bullish that $IREN has been deliberately delaying a deal as they understand that their position becomes stronger by the day.

Small Cap Snipa@SmallCapSnipa

$NBIS RECEIVED 40% PREPAYMENT FROM MICROSOFT Nebius just disclosed that’s Microsoft provided $6.95 billion upfront prepayment under their latest agreement AI Infrastructure providers are gaining leverage As hyperscalers race to secure AI compute capacity, contract terms are becoming increasingly favorable for cloud providers

English

@ArtofSpecuycky 正常來說,其他數據中心都還沒建好,算力的合約早就被搶光了,現在建好都沒人要,IREN的數據中心應該存在一些問題,很可能是技術/支援缺陷,而導致遲遲沒有合約… 因為曾有人比較過,其他數據中心像NBIS那些都是一條龍服務,你要用算力嗎,客戶不需要額外做太多,但IREN好像就只賣算力,支援遠遠不足。

中文

$IREN 财报前瞻:Sweetwater 1已通电,5月7日的真正悬念只剩一个

先说昨天发生的事

2026年5月1日,IREN正式宣布Sweetwater 1变电站成功接入ERCOT电网,1.4GW高压变电站通电完成。

市场等了半年的里程碑,在财报前6天悄悄落地。

没有大张旗鼓。没有股价暴涨。

因为市场知道:通电不是终点,客户才是。

财报数字:不是重点

先把头条数字说完:

共识预期:总营收$219.9M,AI Cloud $83.1M,EPS -0.24。上季度营收$184.7M,miss了将近20%,股价跌6.9%。

我预期这次头条数字大概率再次miss。

原因很简单:

Q1比特币价格走弱

矿机加速下架腾挪给GPU

= 比特币收入继续萎缩

这不是风险,这是战略

越快甩掉比特币

市场就越快用数据中心的估值体系看IREN

唯一重要的问题

Sweetwater 1的第一个客户是谁?

1.4GW电力已经通了。 全球算力荒还在持续。 B300现货$100万还被抢光。

从逻辑上讲,IREN不可能通电之后坐等客户上门。

几个细节值得注意:

细节一:通电公告的措辞

IREN官方声明原文:"energization is an important step toward bringing grid-connected capacity online and reducing time-to-compute for customers。"

用的是"customers",不是"potential customers",不是"future customers"。

这可能是措辞习惯,也可能意味着谈判比公开信息显示的更深入。

细节二:Childress的异动

100MW+矿机正在被下架。

你不会无缘无故放弃现成的现金流,除非已经知道那块容量要给谁用。

细节三:上季度提到的"数十亿美元软件交易"

这句话在上季度财报电话会上被管理层提及,然后再也没有后续解释。

这不是偶然的口误。

我对5月7日的判断

确定会看到的:

Sweetwater通电确认(已发生)

AI Cloud收入约$81-83M

ARR从$2.3B往上走

50K B300 GPU进度更新

可能出现的惊喜:

新客户合同宣布

→ 第二个Hyperscale合同

→ 股价短期+20-30%,估值重估开始

ARR跳升至$3B+

→ 意味着新合同已签但未宣布

→ 间接确认客户进展

"数十亿美元软件交易"更新

→ 上季度提及,这次必须给答案

有没有惊喜的概率:

我的判断:60%有正面惊喜

不是因为有内幕

而是因为:

通电选在财报前6天发生

≠ 巧合

= 在为更大的公告做铺垫

市场怎么定价这次财报

期权市场定价显示财报后预期波动幅度约±16%,对应约±$7。

有新客户合同 → $55-65(+20-40%)

财报好无合同 → $48-52(+5-15%)

miss无催化剂 → $38-42(-10-20%)

我的核心观点

IREN现在面临的不是执行问题。

Childress已经证明了执行力。 微软合同已经证明了客户质量。 Sweetwater通电已经证明了时间节点。

IREN面临的是叙事问题。

市场还在用"矿商"的眼光给它5-6x P/S的估值。 AWS和Azure这样的云基建商享受8-12x P/S。

这中间的差距不需要任何新的奇迹来填平。

只需要Sweetwater签到第一个Hyperscale客户。

电已经通了。 钱在等答案。 5月7日,见分晓。

#IREN #AI基础设施 #数据中心 #财报前瞻 #StockMarket #Investing #交易

中文

@treasury_bill @Lazarus_Capital No reaction AH????? We have $47.12 right now

English

@LukasFrije1re Not happening. @danroberts0101 will say this on next call:

"Look mate we are still early in the AI cycle."

English

On paper, $IREN looks great

Secured energy, GPU deliveries and energized sites coming soon

But they cant sign a deal to prove their business model works.

A deal with 12M+/MW like NBIS would save the company and shut down the bears.

But the market needs to see execution

English

@BlackPantherCap why you dont buy crwv or nbis ? it take years it waste of time! time is money

English

Most people underestimate how long the runway is for AI infrastructure buildout. $IREN 4.5 GW pipeline doesn't come online in six months. It comes online over three years. Patience is the position.

English

I just watched the $nbis interview between Roman and Daniel Koss.

And I am even more bullish on $iren...

Roman Chernin:

"This is the game of scale"

"This is the game of capacity"

"Can you support the growth of your customers"

"The combination of our scale and our vertical Integration that we would control infrastructure needs and the ability to do just the right engineering job and provide the performance will let us be very successful."

Sounds like Iren to me...

English

@AvivArazi The policy shift has left Sweetwater 1 (SW1) facing a sudden requirement for $70 million in non-refundable interconnection fees, alongside an additional $70 million in financial security.

English

@rreddi The policy shift has left Sweetwater 1 (SW1) facing a sudden requirement for $70 million in non-refundable interconnection fees, alongside an additional $70 million in financial security.

English

@ilzmcfly This policy shift has left Sweetwater 1 (SW1) facing a sudden requirement for $70 million in non-refundable interconnection fees, alongside an additional $70 million in financial security.

English

@XCapitalMgmt This policy shift has left Sweetwater 1 (SW1) facing a sudden requirement for $70 million in non-refundable interconnection fees, alongside an additional $70 million in financial security.

English

Key $GOOG earnings quotes related to $IREN thesis:

*On Cloud growth and demand intensity:

"Cloud accelerated again this quarter due to strong demand for our AI products and infrastructure. Revenue grew 63%, exceeding $20 billion for the first time, and our backlog nearly doubled quarter-on-quarter to over $460 billion."

"Google Cloud's backlog nearly doubled sequentially, reaching $462 billion at the end of the first quarter."

"We expect to recognize just over 50% of the backlog as revenue over the next 24 months."

*On compute constraints:

"Obviously, we are compute-constrained in the near term. As an example, our cloud revenue would have been higher if we were able to meet the demand."

"We are seeing unprecedented internal and external demand for AI compute resources."

*On CapEx trajectory:

"We are updating our full year 2026 CapEx guidance range to $180 billion-$190 billion, up from our previous estimate of $175 billion-$185 billion."

"Looking ahead, these strong results reinforce our conviction to invest the capital required to continue to capture the AI opportunity. As a result, we expect our 2027 CapEx to significantly increase compared to 2026."

"CapEx was $35.7 billion in the first quarter, with the overwhelming majority of this spent in technical infrastructure to support the AI opportunities we see across the company. Approximately 60% of our investment in technical infrastructure this quarter was in servers, and 40% was in data centers and networking equipment."

"The significant increase in our investment in technical infrastructure will continue to put pressure on the P&L in the form of higher depreciation expense and related data center operations costs, such as energy."

*On TPU sales to customer data centers:

"As TPU demand grows from AI labs, capital markets firms and high-performance computing applications will begin to deliver TPUs to a select group of customers in their own data centers in a hardware configuration to expand our addressable market opportunity."

"In Google Cloud, as Sundar mentioned, we will begin to deliver TPU hardware to a select group of customers in their own data centers. We expect to begin recognizing a small % of the revenues from these agreements later this year, with the vast majority of revenues to be realized in 2027."

"There are situations where it makes sense. For example, you take customers like capital markets, where they're running this highly performant AI workloads. They wanted, you know, TPUs in their data centers. There are, you know, and those trends are true across a diverse set of industries and in certain cases, frontier AI labs too."

*On $NVDA partnership:

"NVIDIA GPUs are a core part of our AI accelerator portfolio and will be among the first to offer NVIDIA Vera Rubin NVL 72 in addition to the Blackwell and Hopper-based instances already available."

*On token processing volume (demand intensity proxy):

"Our first-party models now process more than 16 billion tokens per minute via direct API use by our customers, up from 10 billion last quarter."

"Over the past 12 months, 330 Google Cloud customers each processed over 1 trillion tokens. 35 reached the 10 trillion token milestone."

English

This policy shift has left Sweetwater 1 (SW1) facing a sudden requirement for $70 million in non-refundable interconnection fees, alongside an additional $70 million in financial security.

Strategic Posturing #IREN

English