@Capital4Value@MarketPalmer_ Yes, of course they manage the odd repair that comes up which is all pass through to the owner. But there really isn’t any work for a PM to do after the tenant is in place. Paying 10-15% a month of a $3-4k rent is bananas. For what? Depositing the check for you?

Arizona coach Tommy Lloyd has agreed to a new deal with the school, he announced. Arizona’s new five-year deal with Lloyd will make him one of the five highest paid coaches in college basketball, per me and @jeffborzello.

@TimRodocker@MarketPalmer_ How do you keep the PM incentivized to care about your property. $65/mo basically means they will work 2 hours (max) on your property a month. Or else, they make zero.

@Capital4Value@MarketPalmer_ Never waste your time managing a rental home. I pay $65 a door to a manager to do it for me. I have to make about 5 decisions a year. If that…

IRS closed ~440k tax audits in 2024.

Most of the audits are for people making $0-$50,000

Small businesses with lots of deductions, earned income tax credits, etc

Audit risk generally goes down as your income goes up.

If you are buying a business, and you are analyzing cash flow

If a company takes bonus/179 depreciation

You should normalize depreciation to it's economic life instead of showing the full basis

Otherwise cash flows will be understated & really throw off your analysis

I took out a life insurance policy on my neighbor even though I don’t even know their name.

I then used AI to create a fake newspaper and a fake obituary and sent that to the insurance company.

Easiest way to get Rich quickly in 2026

Why aren’t more people doing this?

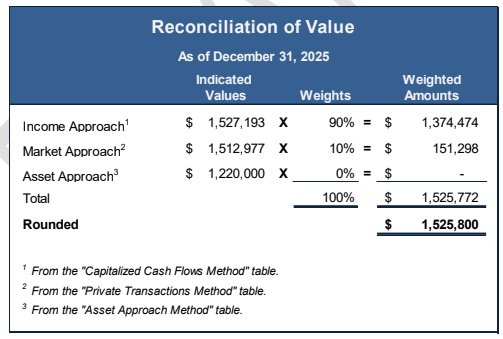

All approaches should be considered

Generally the asset approach is the lowest value as it excludes any intangible value of the business

With a going concern premise, and a profitable business that plans to be profitable in the future, the business should have intangible value above & beyond just the worth of the fixed assets

This is always an unsettling feeling in valuation

The market & income approaches are close: Yay!

But the cost approach is not much lower. and the company makes money every year.

The Kicker: The owner upgrades equipment frequently.

You want a mix, tax wise with your investment accounts:

Tax Free: Roth, HSA, 529, etc.

Tax Deferred: Traditional accounts

Taxable: Brokerage account

But... you don't have to contribute to each, each year

There are times throughout your life where one is better than the others

Here's the framework I think through:

- Pretax 401(k): use in your highest income earning years, think 32-37%

- Roth 401(k): use in your lower income earning years, think 12-24%

- mega backdoor Roth 401(k): use whenever you have the funds if you have maxed above

- Roth IRA/backdoor Roth: use after maxing out above every year you can (sometimes it makes sense to do before maxing out above)

- HSA: use and max out when you have an HSA eligible plan. Best of both worlds here with pre-tax deferral, tax free growth and use

- Taxable: use the entire time to build liquidity and another place to pull from in the future

- Cash balance plan: in very, very high earning years

- Deferred comp: in last few years before retirement if you are a very high earner