0xMin retweetledi

0xMin

2.6K posts

0xMin retweetledi

0xMin retweetledi

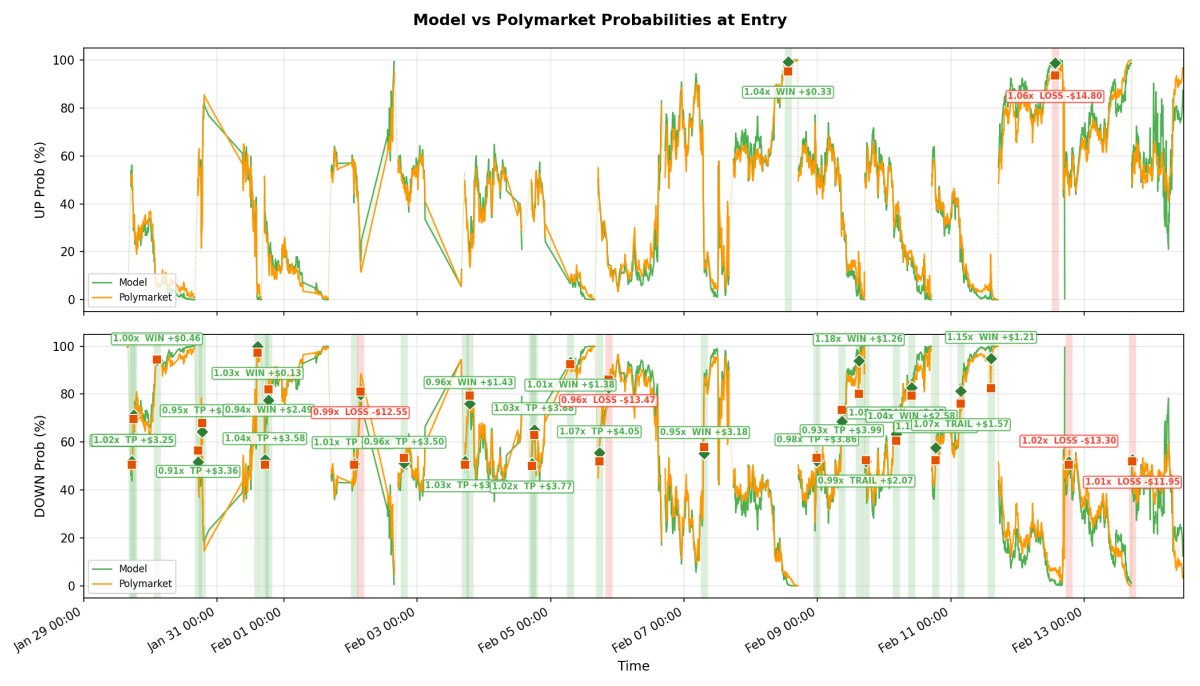

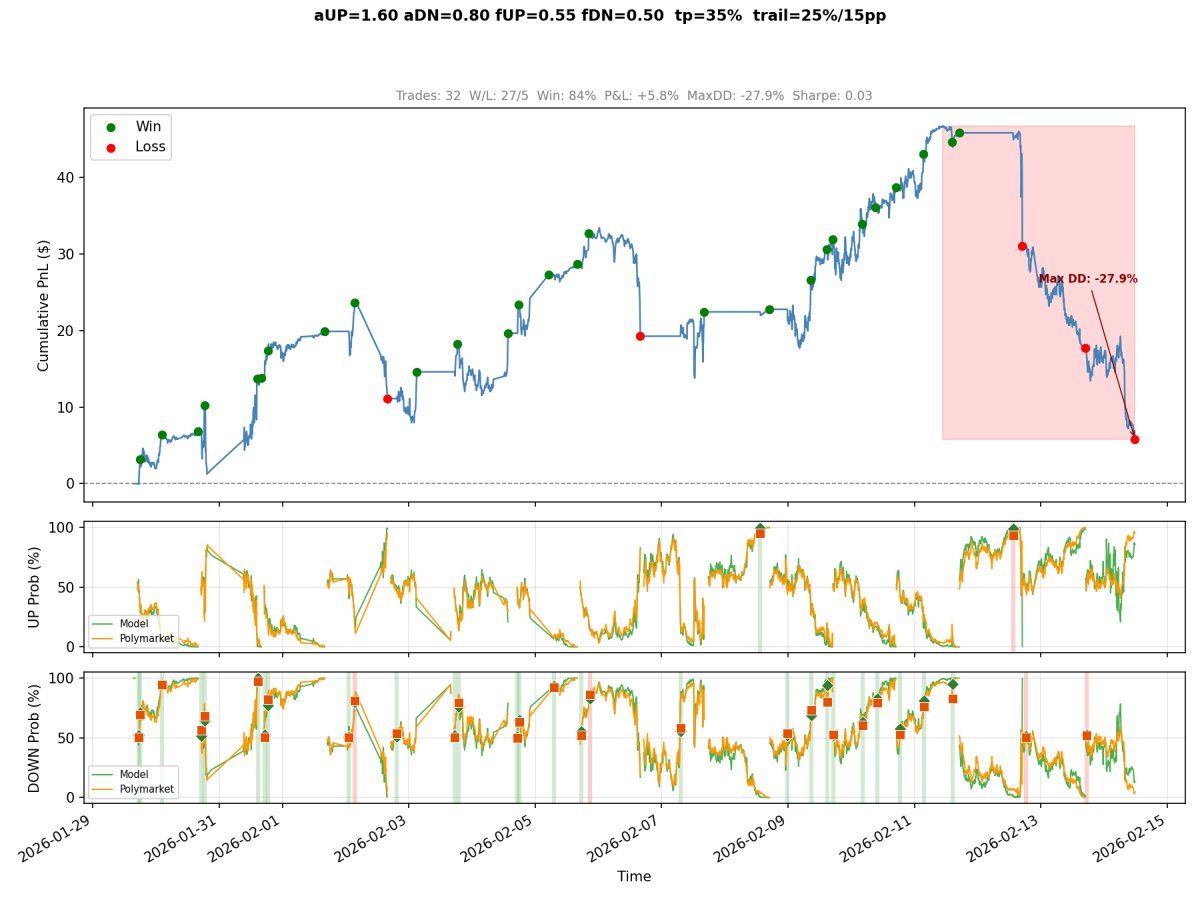

昨天转发了一篇用 Deribit 波动率曲面推导 Polymarket 二元期权定价的思路。一位做 PM 自动化交易的大哥@jtrevorchapman 告诉我,他几个月前试过类似的路径,结论是在 15 分钟尺度上,波动率曲面能给的信息,市场微结构信号可以更快更准地捕捉到。

我赶紧去看了大哥的实盘,发现他当前使用的交易系统表现非常优秀,盈利因子 4.29(每亏 $1,能赚回 $4.29),胜率 93%,而且他有问必答毫无保留。

热心哥的核心系统是一个三层架构:记忆 → 信号 → 防御

1. 记忆层

每个 session 开始,先扫描最近 30 +个已结束的 session,找出最像当前盘面的历史 session。比如当前 BTC 价格在某个位置、波动率是某个水平、市场情绪是某个状态,在过去类似的session中,最后结果是 UP 赢得多还是 DOWN 赢得多?如果是 UP 多,那么系统会带着这个“历史经验”(先验偏差)进入下一层。

2. 信号层

这层关注实时数据,每秒钟运行8-12条规则,然后独立投票UP / DOWN + 置信度(0-100%)。这些规则中热心哥认为 CVD(累计主动买卖量差)是预测力最强的单一指标。其他还有预言机报价距离、 Binance 动量、订单簿不平衡、UP / DOWN 代币价格走势(反映 PM 上所有参与者的集体判断)。

所有规则按置信度加权,得出方向和综合置信度,如“方向 YES,综合置信度约 65%”。

3. 防御层

方向确定后,用五个因子算出一个 0-1 系数,直接乘到仓位上,1 就是全仓执行,0 就不做。所以同样一个"65% 置信度 YES"的信号,根据防御层的评估,仓位大小也会有区别。这五个因子如下:

- CVD 同不同意?如果信号层说 UP,但 Binance 上的净卖压很大(CVD 不同意),仓位直接大幅压缩。CVD是热心哥极其看重的因子,在session混乱的情况下(预言机报价反复穿越基准价格 5 次),CVD 甚至有一票否决权(系数降为 0)。

- 距离基准价格多少?如果 BTC 现价和基准价咬得很紧,说明随时可能翻盘,需要压缩仓位。

- session 剩多少时间?如果只剩最后两三分钟,任何突发波动都来不及反应,风险陡增。

- 当前 session 预言机报价反复穿越了基准价格几次?超过 5 次就算混乱。混乱市场里信号可靠性大打折扣,仓位要激进压缩。

- 当前入场价的利润空间够不够?入场价越高,对胜率的要求也越高,所以系统在高价位时对信号可信度要求极高。比如 $0.95 入场时,只允许最无歧义最干净的信号通过。

除了核心系统之外,热心哥还提过几个额外细节:

- 只做 BTC,不做 ETH 市场,估计是 ETH 的信号不稳定

- 用 40 天、每 200 毫秒记录一次的数据做回测,发现在 session 剩余 6 分钟的时候指标才开始可靠。他用这个来衡量反转风险,过滤掉不该进的session。

限于时间没有全部整理完,他时间线上还有很多细节,推荐去翻翻。原文来自这篇回复:

x.com/jtrevorchapman…

中文

0xMin retweetledi

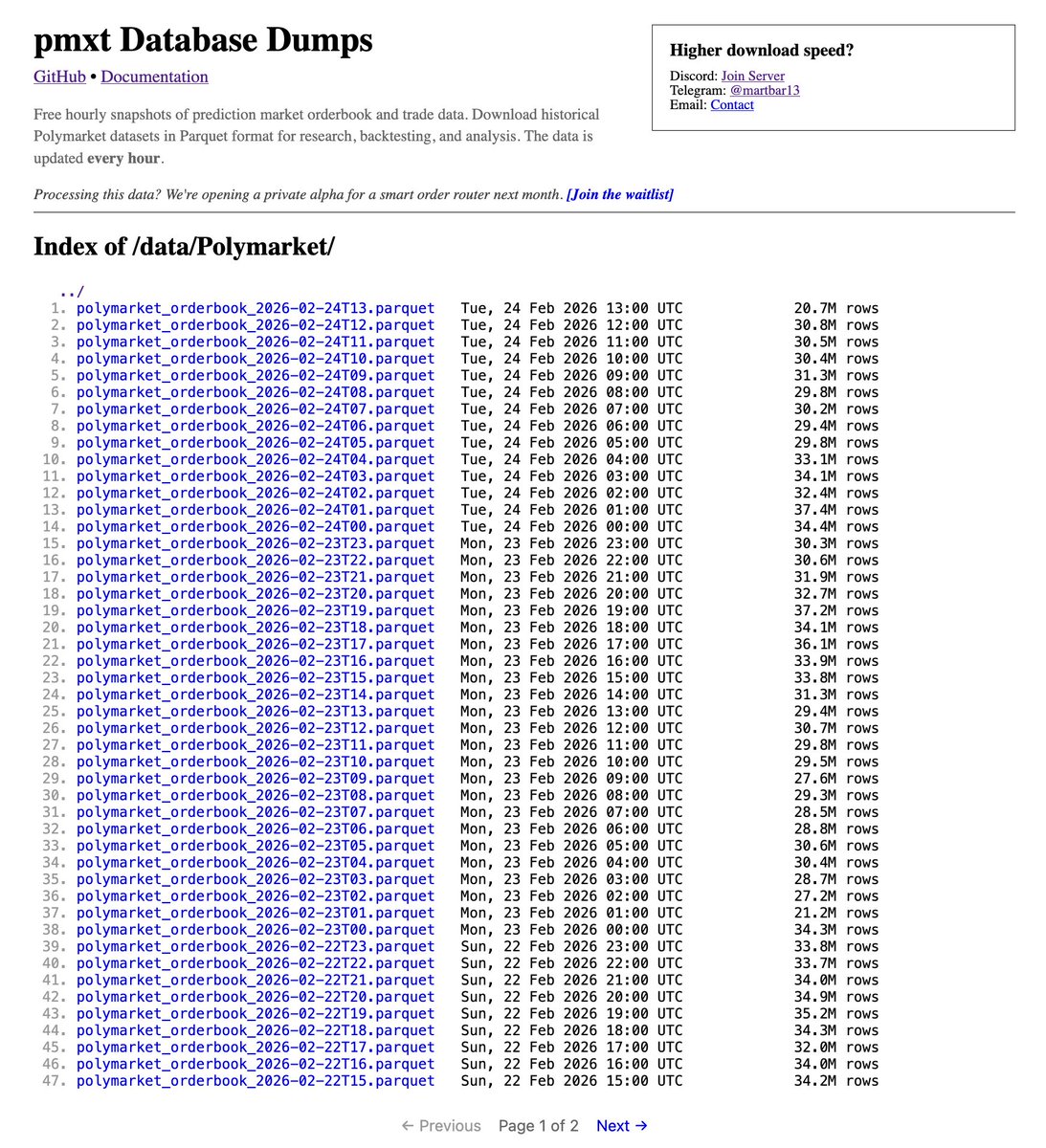

预测市场终于有公开的全量 orderbook 数据了。

每小时更新,记录所有市场的每一次挂单变化和成交,30M 行/快照,Parquet 格式免费下载。Polymarket / Kalshi / Opinion 都覆盖。

成交记录只能告诉你「发生了什么」,挂单簿才能告诉你「为什么发生」。做策略回测的人都知道这个数据有多稀缺。

Martin@martkiro

I just published a data dump of full order book data from @Polymarket The data is maximally granular. There is no filtering whatsoever. Every order book change and trade is saved. Across all markets Updates are hourly. Each snapshot contains ~30M rows. Snapshots are downloaded as parquet files. Each file is approx. 500MB-1GB large. The data dump is already 2B+ rows large and growing fast. But this is just part 1/3. Coming soon is a much bigger dump that also includes @Kalshi / @opinionlabsxyz / @trylimitless etc I started collecting this data because I noticed I couldn't get it from Dome API. Their historical order book data was filtered limiting its usefulness. Also now with the acquisition there's a lot of uncertainty about whether they will continue operating

中文

0xMin retweetledi

上一篇说到 Polymarket Up/Down 市场的定价模型不是主要的竞争优势来源,但是没有肯定也不行,如果大家对于研究定价模型没有思路,可以看看下面这篇,也许有所启发。

作者的核心思路是利用 Deribit 期权市场的专业定价来给 Polymarket 的二元期权估值。具体来说:

Deribit 上有大型做市商用复杂的波动率模型定价,这些信息都隐含在期权的报价里。但 Deribit 并没有和 Polymarket 完全匹配的超短期期权(比如 15 分钟到期的),所以不能直接查看某个行权价的隐含波动率。

作者的做法是每隔 5-10 秒抓取 Deribit 全部期权报价,用 SSVI 模型拟合出完整的波动率曲面,然后插值得到任意到期时间和行权价对应的隐含波动率,最后代入 Black-Scholes 的二元期权公式算出"公允概率"。当这个概率和 Polymarket 的市场价出现足够大的偏差时,就是交易机会。

Vladic@Vladic_ETH

PROBABILITY ARBITRAGE: HOW TO BEAT POLYMARKET USING DERIBIT OPTIONS Trading "Bitcoin Up or Down" on feelings is a casino. Trading them through options math is a systematic business. The strategy is simple: Deribit knows the future better than retail on Polymarket. The options market contains the volatility models of market makers like Galaxy and Wintermute. Our task is to export this knowledge into the inefficient Polymarket order book. 1) The Fundamental Idea Polymarket Up/Down markets are essentially binary options > If Price > Strike: Pay $1 > If Price < Strike: Pay $0 The price (e.g., 55 cents) is the implied probability (55%) Polymarket is driven by the crowd. Deribit is driven by giants using complex volatility models. If the Deribit model shows a 60% probability of an upside move, but Polymarket trades at 50 cents, you have found a Positive EV trade with ~20% ROI. 2) The Math To find the fair probability, we use a modified Black-Scholes formula for binary options. We need the Probability of expiring ITM. Formula for P(Up): Variables: > F (Forward Price): Futures price > K (Strike): The target price on Polymarket. > T (Time): Time to expiration in years. > σ : The hardest part - Implied Volatility (IV) 3) The Data Pipeline You cannot just scrape IV from the Deribit interface because there are no options expiring in 15 minutes. You need to build a Volatility Surface. Algorithm: • Snapshot: Capture the entire Deribit options book every 5-10 seconds. • Fitting: Build a Volatility Smile curve using an SVI model or cubic splines. • Interpolation: Interpolate σ for our specific time and strike • Calculation: Plug the resulting σ into the (d2) formula to get the Fair Price 4) Execution and Risks Example Trade: • Model: Calculates N(d2) = 0.62$ • Market: YES shares trade at $0.54$. • Edge: 0.08 • Action: Limit buy Pitfalls: > Spread & Fees: Your model must account for friction. If Edge < 2-3%, the trade is unprofitable. > Drift: On 15-minute frames, Forward is close to Spot, but during high volatility, the difference is critical. Always use perpetual contract data to calibrate. > Latency: The bot must react within milliseconds of a Deribit book update. You are not guessing where Bitcoin will go. You are arbitraging the inefficiency between a trillion-dollar professional options market and a retail prediction market This is pure quant trading

中文

0xMin retweetledi

THEORY WITHOUT PRACTICE IS DEAD. HERE ARE THE PROOFS

The source who highlighted this mechanic (and with whom we are calibrating live execution right now) just shared their trade report

This is what PnL looks like when you trade pure mathematical inefficiency between Deribit whales and Polymarket retail, instead of feelings.

The edge is real. We continue testing

Vladic@Vladic_ETH

PROBABILITY ARBITRAGE: HOW TO BEAT POLYMARKET USING DERIBIT OPTIONS Trading "Bitcoin Up or Down" on feelings is a casino. Trading them through options math is a systematic business. The strategy is simple: Deribit knows the future better than retail on Polymarket. The options market contains the volatility models of market makers like Galaxy and Wintermute. Our task is to export this knowledge into the inefficient Polymarket order book. 1) The Fundamental Idea Polymarket Up/Down markets are essentially binary options > If Price > Strike: Pay $1 > If Price < Strike: Pay $0 The price (e.g., 55 cents) is the implied probability (55%) Polymarket is driven by the crowd. Deribit is driven by giants using complex volatility models. If the Deribit model shows a 60% probability of an upside move, but Polymarket trades at 50 cents, you have found a Positive EV trade with ~20% ROI. 2) The Math To find the fair probability, we use a modified Black-Scholes formula for binary options. We need the Probability of expiring ITM. Formula for P(Up): Variables: > F (Forward Price): Futures price > K (Strike): The target price on Polymarket. > T (Time): Time to expiration in years. > σ : The hardest part - Implied Volatility (IV) 3) The Data Pipeline You cannot just scrape IV from the Deribit interface because there are no options expiring in 15 minutes. You need to build a Volatility Surface. Algorithm: • Snapshot: Capture the entire Deribit options book every 5-10 seconds. • Fitting: Build a Volatility Smile curve using an SVI model or cubic splines. • Interpolation: Interpolate σ for our specific time and strike • Calculation: Plug the resulting σ into the (d2) formula to get the Fair Price 4) Execution and Risks Example Trade: • Model: Calculates N(d2) = 0.62$ • Market: YES shares trade at $0.54$. • Edge: 0.08 • Action: Limit buy Pitfalls: > Spread & Fees: Your model must account for friction. If Edge < 2-3%, the trade is unprofitable. > Drift: On 15-minute frames, Forward is close to Spot, but during high volatility, the difference is critical. Always use perpetual contract data to calibrate. > Latency: The bot must react within milliseconds of a Deribit book update. You are not guessing where Bitcoin will go. You are arbitraging the inefficiency between a trillion-dollar professional options market and a retail prediction market This is pure quant trading

English

0xMin retweetledi

I just published a data dump of full order book data from @Polymarket

The data is maximally granular. There is no filtering whatsoever. Every order book change and trade is saved. Across all markets

Updates are hourly. Each snapshot contains ~30M rows. Snapshots are downloaded as parquet files. Each file is approx. 500MB-1GB large.

The data dump is already 2B+ rows large and growing fast. But this is just part 1/3. Coming soon is a much bigger dump that also includes @Kalshi / @opinionlabsxyz / @trylimitless etc

I started collecting this data because I noticed I couldn't get it from Dome API. Their historical order book data was filtered limiting its usefulness. Also now with the acquisition there's a lot of uncertainty about whether they will continue operating

English

0xMin retweetledi

0xMin retweetledi

看完 Polymarket 最近的链上数据

我觉得最值得注意的事:

用户在两个月内涨了快50%

2025 年 10 月,Polymarket 月活用户大概在 47.8 万。

到 2026 年 2 月,这个数字是 68.8 万——历史新高,两个月涨了 44%。

暂时没有任何证据证明这些是羊毛用户,而且在 crypto 市场低迷的市况下,我不认为羊毛用户可以增长如此剧烈。

一种推断是 2025 年底 CFTC 批准 Polymarket 重返美国市场,2026 年 1 月正式开放。被禁了快三年的美国用户终于能合法交易,第一个月就灌进了大量新钱包。

在 crypto 最严峻的冬天,我还是认为 Polymarket 很有可能成为 2026 最大的空投。

中文

0xMin retweetledi

0xMin retweetledi

0xMin retweetledi

Binance Wallet集成Aster Perp,币安系的资源进一步整合

双赢局面:BN Wallet给Aster输送更多用户,Aster给BN Wallet丰富了合约交易这一功能模块

Aster 🥷@Aster_DEX

Aster now powers perpetuals on @BinanceWallet (Web). SafePal. Trust Wallet. Now Binance Wallet. When wallets need perps infrastructure: matching engines, deep liquidity, precise pricing—they no longer reinvent the wheel. Aster is where wallets go for perps. 👉 web3.binance.com/en/perpetuals?…

中文

0xMin retweetledi

You can now trade Perpetual Futures on Binance Wallet (Web) – provided by @Aster_DEX .

✨Earn Aster points when you trade.

🎁Participate in an exclusive campaign for Binance Wallet users, share up to 200,000 USDT in rewards!

Start now 👇

binance.com/en/support/ann…

English

0xMin retweetledi

承蒙大家厚爱,polymarket-sdk 仓库现在已经有 129 个 star 和 37个fork.

开源YYDS!

github.com/cyl19970726/po…

@Polymarket

今天更新了下架构,基本上你在polymarket上需要的所有操作这里都提供了对应的方法,比如存钱,Swap,Search Market,以及给大家提供一个ArbitrageService,大家如果想做套利可以用这个进行套利尝试。

ArbitrageService:

Polymarket Arbitrage简单来说:

就是如果 Buy Pair(yes,no) 的成本小于 1USDC,那么你可以同时买1yes和1no,然后去合约里换回1USDC, 这样就可以赚一个价差。

相反如果 Sell Pair(yes,no) 大于 1USDC, 那么也可以去合约里花1USDC mint 1 Pair(yes,no) 然后卖出同样也可以赚取价差。

但是在实际的套利过程中,利润产生的那个时刻,其实是没有时间给你去链上操作合约的,所以我们在实现套利服务的时候采用的是动态仓位,就是USDC : Pair(yes,no) 的比在20%~80% 之间从而保证我们出现 Sell的机会有Pair(yes,no)可以Sell,出现Buy的机会有USDC可以买入.

以及因为套利很多时候会有一个严重的问题,就是往往你只能部分成交,所以可能出现 (YES,NO) 数量不是1:1 的情况,这里我在套利服务里使用了比较简单的办法处理,看就是卖掉多的那一个token,保证YES跟NO 1:1

以及也实现了帮你随时情况仓位的 settlePosition 功能等等

关于Polymarket完整套利原理,我在仓库的文档里也写了完整文档,需要的朋友可以自取github.com/cyl19970726/po…

0xhhh@hhhx402

写了一个 polymarket-sdk 把 @Polymarket 的所有api 接口都封装了一下。 并且在API接口的基础上提供了,K线 接口,套利检测,缓存,orderbok 自动排序等等,需要的自取吧: github.com/cyl19970726/po… 架构如下:

中文

0xMin retweetledi

写了一个 polymarket-sdk 把 @Polymarket 的所有api 接口都封装了一下。

并且在API接口的基础上提供了,K线 接口,套利检测,缓存,orderbok 自动排序等等,需要的自取吧:

github.com/cyl19970726/po…

架构如下:

中文

0xMin retweetledi

0xMin retweetledi

$ASTER 火箭发射项目Rocket Launch 第一期 $AT 总结

一共刷了约5M的成交量

拿了1w颗出头的AT + 1110颗ASTER 约4300U

忠诚者奖励给了3000U (头几天刷的真大毛)

刷交易量成本大概1000U左右

如果加上S3的奖励 大概会再给1500颗aster 约1500U

那么最终就是损1000U 拿8800U的奖励 获利7800U

之前预计是大毛 但是比预期少了不少

一 是因为后面几天每天10M+的成交 变得很卷

二 是因为公布的是单向成交 计算要用官方公布的交易量X2

三 可能是官方没去掉做市商的成交(我猜的)

总结下来第二期 $NB (预估明天发把) 也不会有很大的毛 可能就是损耗成本的翻倍奖励把 当作理财了 NB我刷了6M

中文

$ASTER 火箭发射项目Rocket Launch 一鱼三吃

潜在超级大毛 非常早期

个人认为是BN ALPHA的boost版

目前条件是需要在活动开始前

账户持有最低 100 个 $ASTER代币

满足这个门槛的用户 头两期并不多 可以多刷一点

如果现在还没存的前两期火箭项目是无法参与的 但是可以及时关注第三期 第四期....

奖励将根据每个参与者的 现货交易量 相对于活动期间的总交易量 进行分发(这里大家可以根据24h小时交易量算个大概到手的奖励 至少头两期奖励可以说非常丰厚!!)

刷交易量这里大家根据自己的策略来

我刷$AT大概万2-万3磨损 刷$NB大约万10的磨损

此外官方还会发放额外的奖励 比如第一期$AT还没结束

就先发放了价值4000U的$AT给我 想象空间巨大 别等真卷起来了才加入!!

并且S3有加入现货交易量 你刷火箭项目的同时 S3活动也是一起参与的 一鱼三吃

传送门:asterdex.com/zh-CN/referral…

中文