Sabitlenmiş Tweet

And what a time to enter AbcCVX right now.

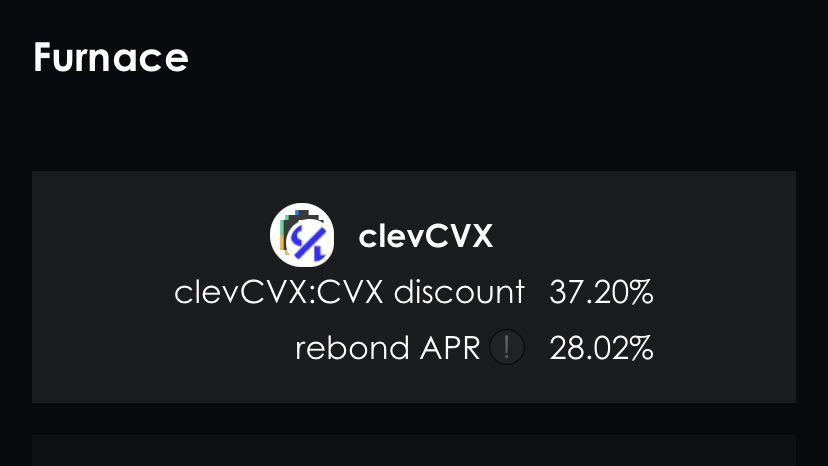

U get to take advantage of the discount on ur way in too, currently its a bit wider than been for awhile.

Result?

Even more CVX working for yah, autocompounding and up to 40% APR.. (veCLEV Max boosted)

Higher than vlCVX, as usual..

This is my vault, this is my yield, this is my boost!

AWat3r@Awater14539727

Want to long $CVX but have commitment issues? Don't want to actively manage a position, but need that good good 30 plus % APY stuff? Autocompound + cash out instantly w/ $afCVX, built on @0xC_Lever tech. Or bring cozy $abcCvx into your home + get big brain yield plus $Clev rewards on top. Shiny.

English