CR@CuratedByR

84 million people saw 'Something Big Is Happening.' Most nodded and kept scrolling. If you actually want to do something about it: here's the financial playbook.

I told you so.. but not with joy

In April 2025 I wrote: "The ease of creating new software also means existing tech products can be copied easily. They will be dismantled like a device and rebuilt by new builders who can do it leaner and cheaper and make it work better for niche segments."

YTD 2026, SaaS companies have been in freefall on the markets. Not a correction, but a structural repricing. The market is finally digesting what was obvious to anyone paying attention: if a product only exists as logic on a screen and AI can rebuild that logic from scratch in days.. what exactly are you paying for?

But here's what most people outside our little X bubble aren't asking: what's next after SaaS?

Because this doesn't stop there.

The disruption people aren't seeing yet

Everyone's focused on software eating software. That's already happening. The next wave is quieter, and hits things people consider real.

Think about office real estate. Not prime, triple-A city centre locations, those adapt. I mean the B and C-grade office parks, the corporate campuses on the edge of town, the floors companies rented because headcount was growing. Remote work cracked the foundation, and now AI is pouring water into those cracks.

If knowledge work becomes something one person does with AI tooling; the work of what used to be 5-10 people, you don't need the space anymore. The companies that survive will be leaner by necessity. The buildings they leave behind won't easily find new tenants, and converting them to housing is slow, expensive, and heavily dependent on local regulation and demand.

Real estate moguls sitting on non-prime office assets are, in my view, in a similar position to SaaS founders in 2023. The fundamentals changed. The valuation hasn't caught up yet.

This is one example. There are dozens of sectors where the same logic applies. Legal support and accountancy, some or most financial advisory. Certain medical diagnostics. Consulting layers that exist purely to synthesise information.. which is exactly what AI does for free.

Nevertheless one new release: a Claude instance trained specifically on legal workflows, a model fine-tuned for a specific industry, and an entire sector faces a repricing moment. We've already seen this. It'll keep happening.

So how do you actually protect yourself over the next 5 years?

First: accept that the index funds you've been told to "just hold" may not be what you think they are.

A global Vanguard World ETF has always stood for being diversified and safe, but it’s important to look under the hood. You're heavily exposed to the mega-cap tech names, which is fine for AI, but also to a long tail of traditional SaaS, digital middlemen, legacy enterprise software, and overvalued "digital transformation" companies that are structurally vulnerable to exactly what's happening. You're also implicitly betting on the same economic model that's being disrupted. Software will become cheaper to make, but software will not become worthless.

So that doesn't mean sell everything because a tracker like that will always rebalance. But for me it means: be intentional.

Here's how I think about building a portfolio for the next 5 years:

1. Get AI exposure, but be realistic about where the upside actually lives

The obvious names are already priced. The companies building the actual intelligence, the ones with the real potential already had their price discovery in private markets.

That said, exposure still makes sense. Just be focused about what you're buying. We don’t know what AI companies will take the cake and I’m not that sure that they will be willing to share. Overall an AI-focused ETF gives you broad exposure to the infrastructure layer. Chips, cloud, data centres, the picks and shovels. You're not getting OpenAI's upside, you're getting a basket of companies that grow as AI adoption grows. That's a reasonable bet. It's not asymmetric, but it's not nothing either.

What I'd look for: beneficiaries that exist outside this circle of obvious names. There’s loads of sectors that can profit off AI automation heavily. Robotics ETF is also ‘only’ up like 10% in a year.

2. Real assets: own things that can't be copied

In a world where digital products get rebuilt overnight, physical scarcity becomes a stronger value proposition, not a weaker one.

Real estate is the obvious play for those with capital, but be selective. Residential in supply-constrained markets. Industrial and logistics (AI needs physical warehouses, data centres, grid infrastructure). Not speculative commercial in B-grade locations.

For those without the capital or appetite for direct property REITs offer exposure to specific asset types without the illiquidity. Look for REITs focused on infrastructure, logistics, or residential. Not office-heavy (I think triple A locations are of great importance here and if you buy a general office REIT you could be doing the same as buying a Vanguard World as mentioned earlier). Not retail-heavy.

The principle: own what can't be replicated by a model running on a server. Oh and yes, AI powered robots could eventually make real estate less scarce, hence why I keep mentioning triple A locations. They will keep their scarcity.

3. The ETF layer: build a "Physical Bunker"

This is where I spent the most time. I ran constant feedback loops; LLMs, Perplexity and scenario modelling to build a shortlist that covers the major trends without pretending to predict which one wins.

The mental model I used: antifragility. Not just protection from downside, but a portfolio that captures upside from AI productivity while sitting on a hard floor of physical assets that software cannot disrupt.

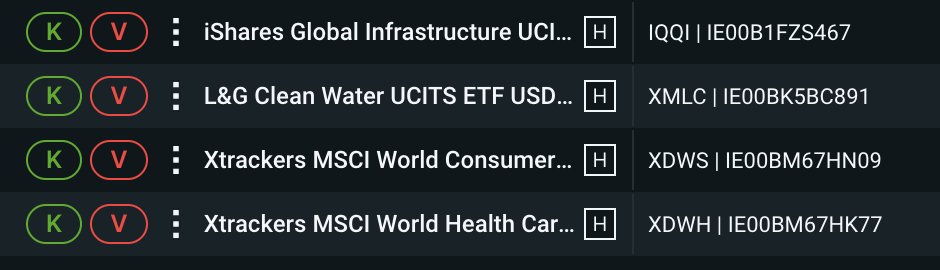

The four I landed on:

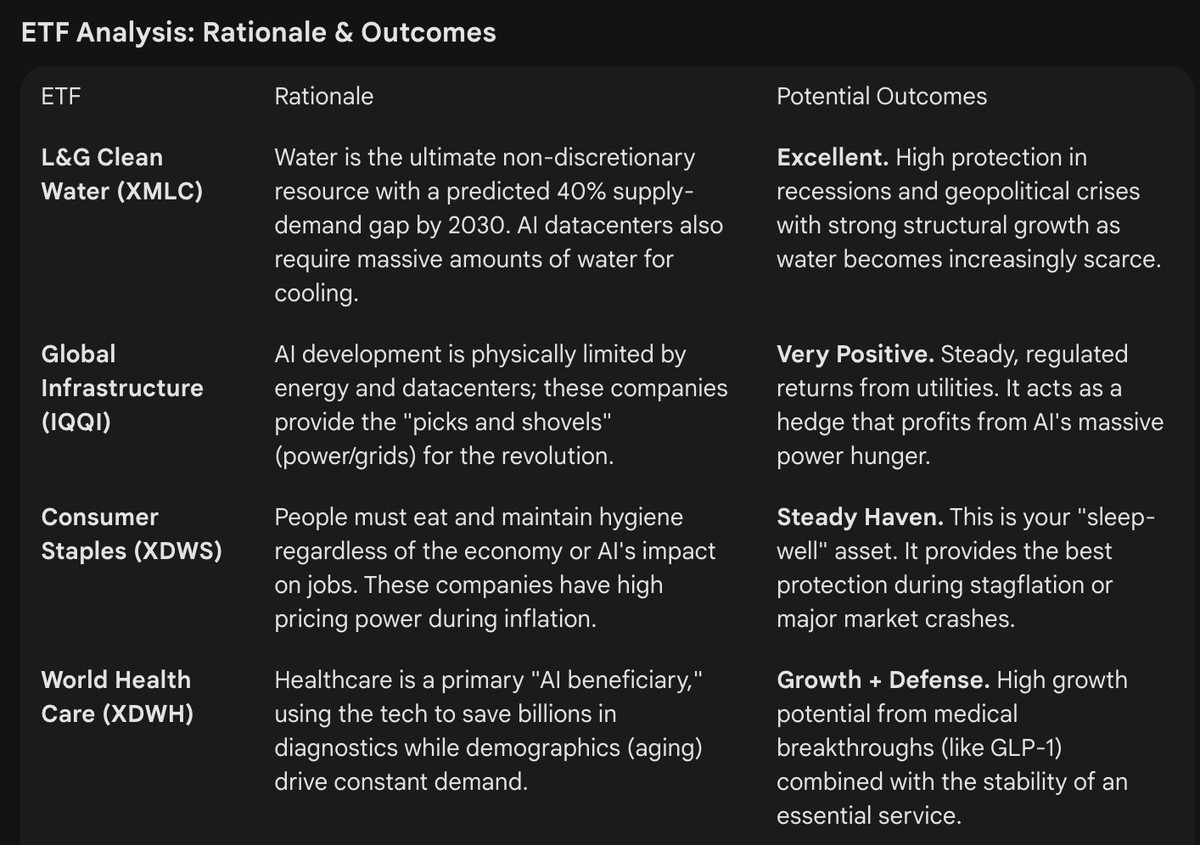

L&G Clean Water (XMLC). Water is non-discretionary. Predicted 40% supply-demand gap by 2030. And something some people miss: AI data centres consume enormous amounts of water for cooling. Even if this doesn’t directly benefit the ETF companies the narrative cannot be unseen.

iShares Global Infrastructure (IQQI). AI development is physically limited by energy and grid capacity. These companies own the infrastructure the intelligence explosion runs on. Steady, regulated returns, with structural tailwinds from something most infrastructure ETFs weren't originally designed to capture.

Xtrackers MSCI World Consumer Staples (XDWS). People eat and maintain hygiene regardless of AI's impact on employment. High pricing power in inflationary environments. This is the sleep-well holding. Best protection in stagflation or mass unemployment scenarios.

Xtrackers MSCI World Health Care (XDWH). Healthcare is a primary AI beneficiary and structurally defensive. Demographics drive constant demand. GLP-1 and AI-assisted diagnostics drive growth. It's one of the rare sectors that benefits from disruption rather than suffering from it.

I also looked at agriculture ETFs seriously. The food shortage thesis is real. But pricing pressure keeps the upside capped, too much structural complexity. Left it out. Obviously with the geopolitical situation a Defense ETF makes sense too, I didn’t include it for now because I also took into account timing/recent results.

Precious metals (gold, silver) deserve a mention here too, the same logic applies. Physical, scarce, and no software can rebuild them. They’ve seen major rallies already.

This ETF portfolio is designed to perform in 3.5 out of 5 major economic scenarios: AI bubble, AI boom, mass unemployment, stagflation, and AGI. In my opinion you cannot hedge for AGI which means we can only plan for 4 scenarios. 3.5 out of 4 is a good score.

4. One more thing: Crypto and AI Agents

Short version, it’s the most speculative part.

Crypto sentiment right now is somewhere between exhausted and absolute despair. However looking at recent OpenClaw developments (The platform for autonomous AI agents running your business) its showing us a world where AI agents could rely heavily on crypto. Using the traditional banking system is difficult, crypto payments make it much easier. I think it will make sense to have a bit of exposure (apart from the Bitcoin-case in general); There is never better timing than during a period of terrible sentiment.

The thread running through all of this: value is shifting. It went from physical to digital, and now back away from things that exist only as logic on a screen. Toward physical scarcity, biological necessity, and the infrastructure that the intelligence revolution actually runs on. The SaaS repricing was only the opening act. Position accordingly.

A portfolio is very personal and clearly there is no *one size fits all* solution, hope this post gives you at least one insight you didn't have yet.

Not financial advice, just my thoughts. None of this is sponsored. Do your own research. Do your own research. Do your own research.