DoubleLine Minutes

5.7K posts

DoubleLine Minutes

@DLineMinutes

A weekly market discussion with DoubleLine's Macro Asset Allocation team recorded Friday afternoon for your Monday morning commute, or anytime in between.

Los Angeles Katılım Ocak 2021

3 Takip Edilen5.9K Takipçiler

DoubleLine Minutes retweetledi

Oil and gasoline have already revived inflation anxiety. Fertilizer points to a broader risk extending into farm input costs and food production.

linkedin.com/pulse/oil-shoc…

English

DoubleLine Minutes retweetledi

DoubleLine Portfolio Manager Ken Shinoda joins @BloombergTV to discuss Fed uncertainty, rising energy prices and DoubleLine’s cautious positioning around AI-related credit risk.

youtu.be/gQxmKG8bFQI

YouTube

English

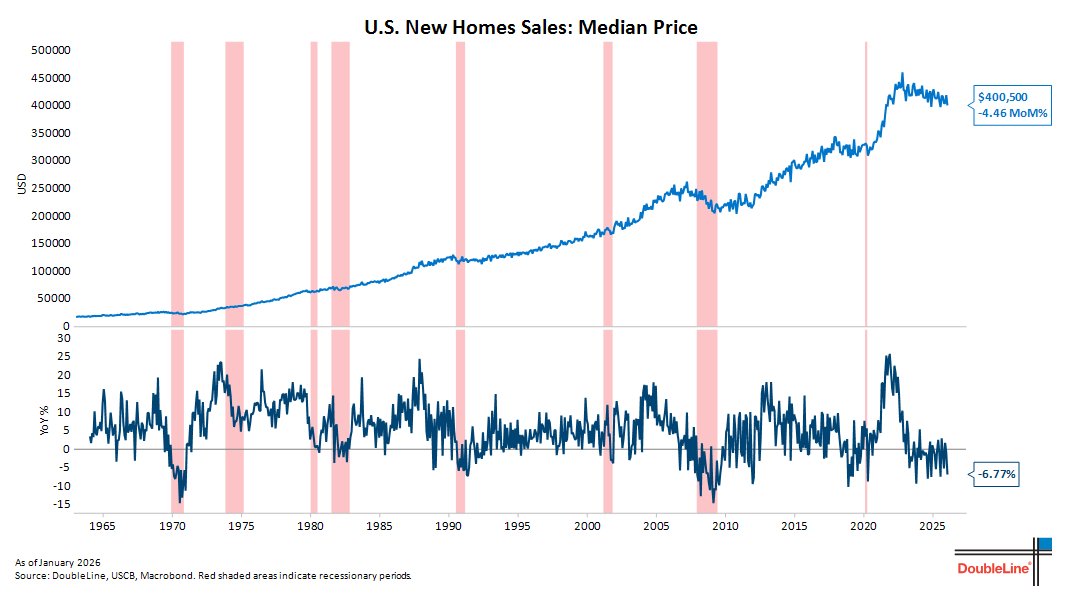

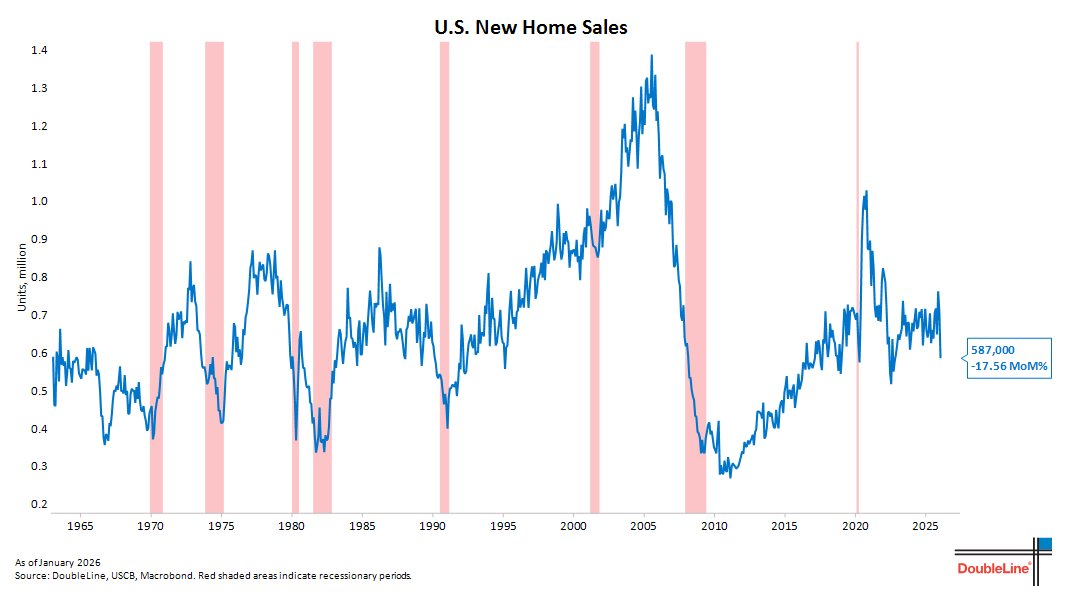

New home sales declined 17.6%MoM in January to 587k SAAR. This is the weakest reading since January 2022. Although the drop was likely driven by extreme weather as new home sales in the Northeast and Midwest were down 44.7% and 33.9% respectively.

English

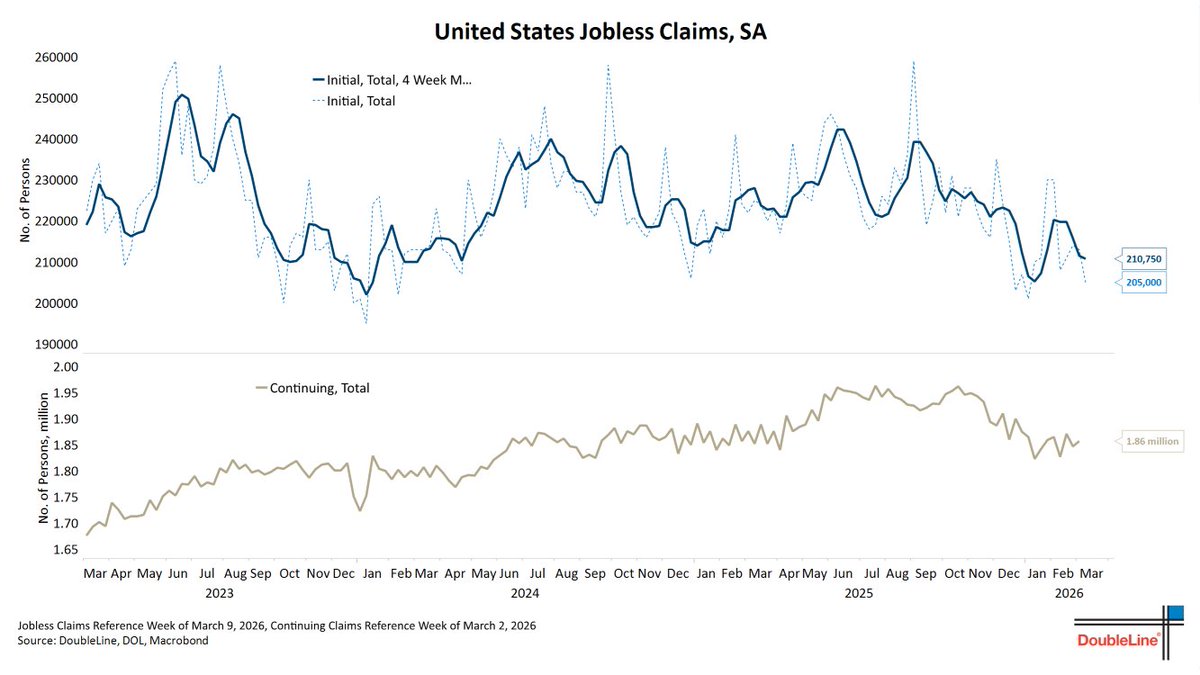

Initial jobless claims for the week of March 14th declined 8k to 205k vs. 215k consensus. The 4-week moving average little changed at 211k. Continuing claims increased 10k to 1,857k vs. 1,852 consensus. The data is not indicating an inflection higher in layoffs.

English

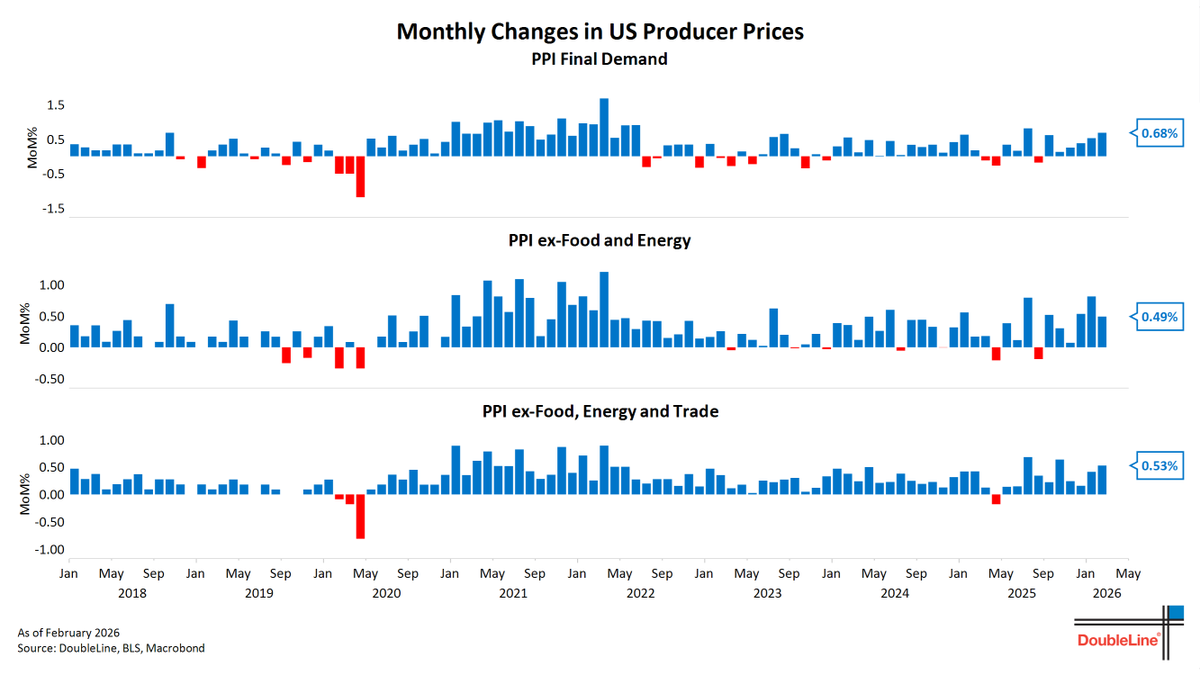

The February producer price inflation data which came in hotter than expected and points to a stronger February core PCE print. Final demand +0.68%MoM vs. 0.3% consensus and +0.5% the previous month. Year-over-year accelerated to 3.39% vs. 3.0% consensus.

Core PPI (ex-food, energy, trade) +0.53%MoM vs. 0.3% consensus and +0.4% the previous month. Year-over-year core PPI increased to 3.50% vs. 3.4% consensus.

English

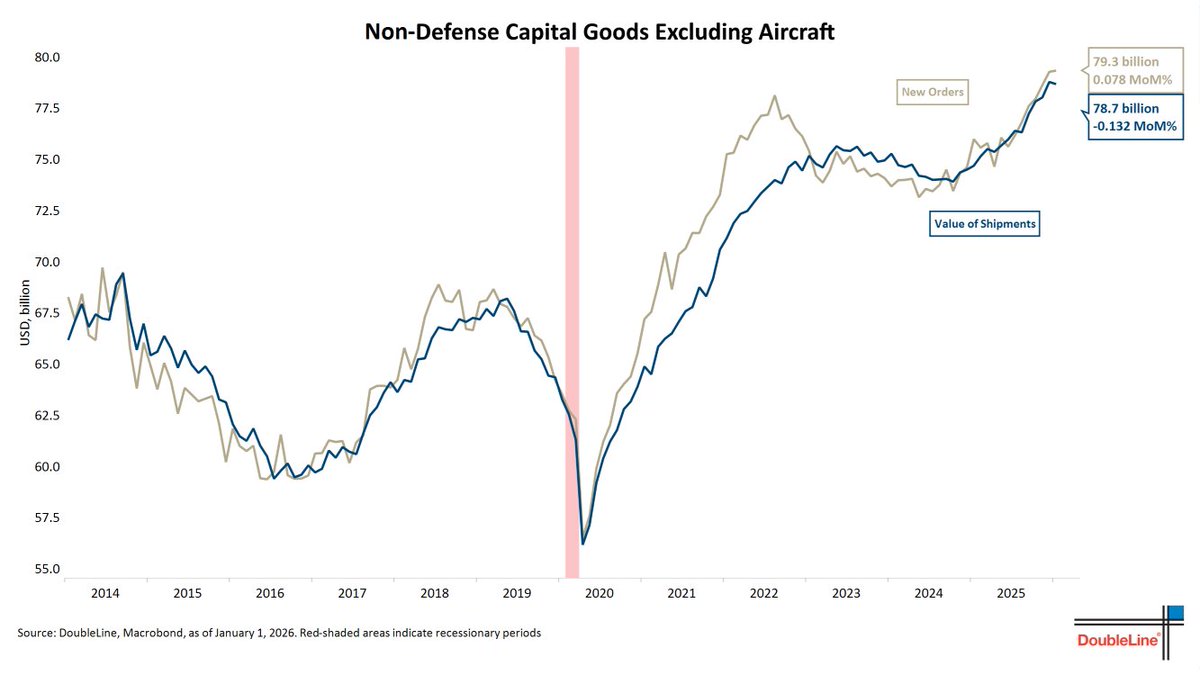

The final release for January showed headline durable goods orders flat MoM. Excluding the volatile transportation segment, orders rose 0.4%MoM. Core capital goods orders (nondefense capital goods orders excluding aircraft) increased 0.1% over the month. Core shipments -0.1%. The level of orders remains above the level of shipments, signaling a better picture for investment growth in the coming quarter.

English

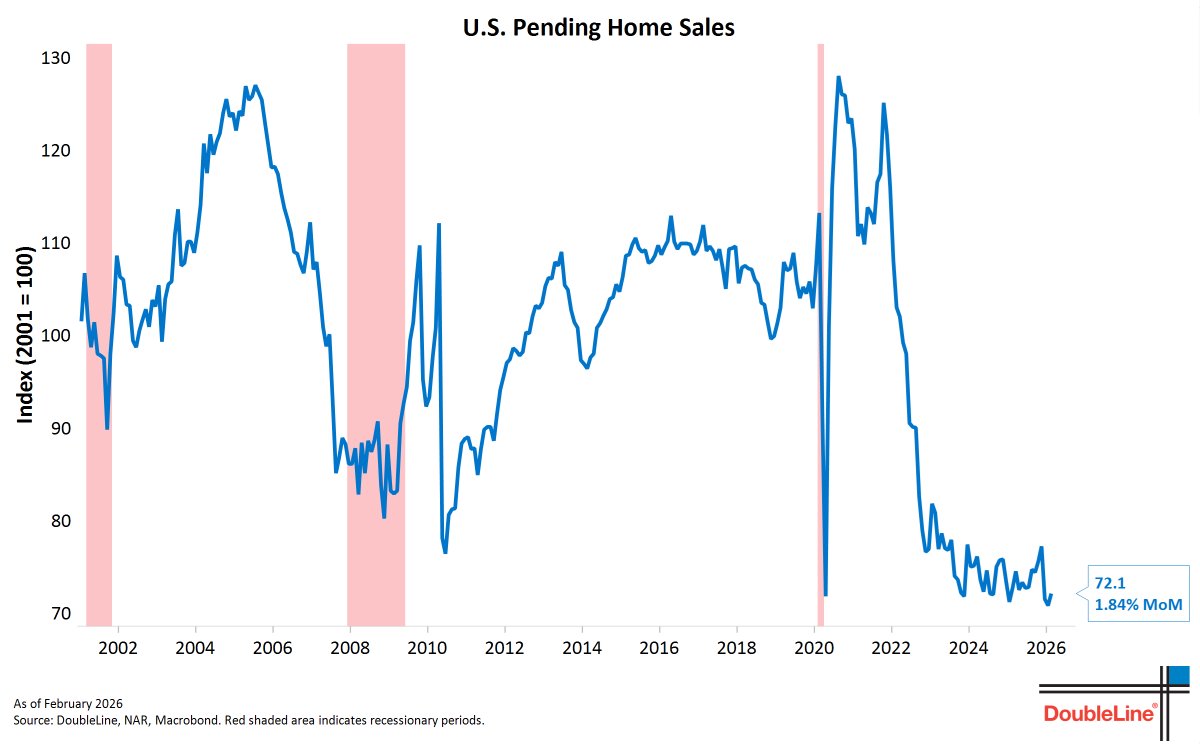

The Pending Home Sales Index rose 1.8%MoM in February to 72.1, slightly above the all-time lows.

“The slight gain in pending contracts appears to be driven by improved affordability conditions. However, those conditions could reverse if higher oil prices lead to an uptick in mortgage rates,” - NAR Chief Economist Lawrence Yun

English

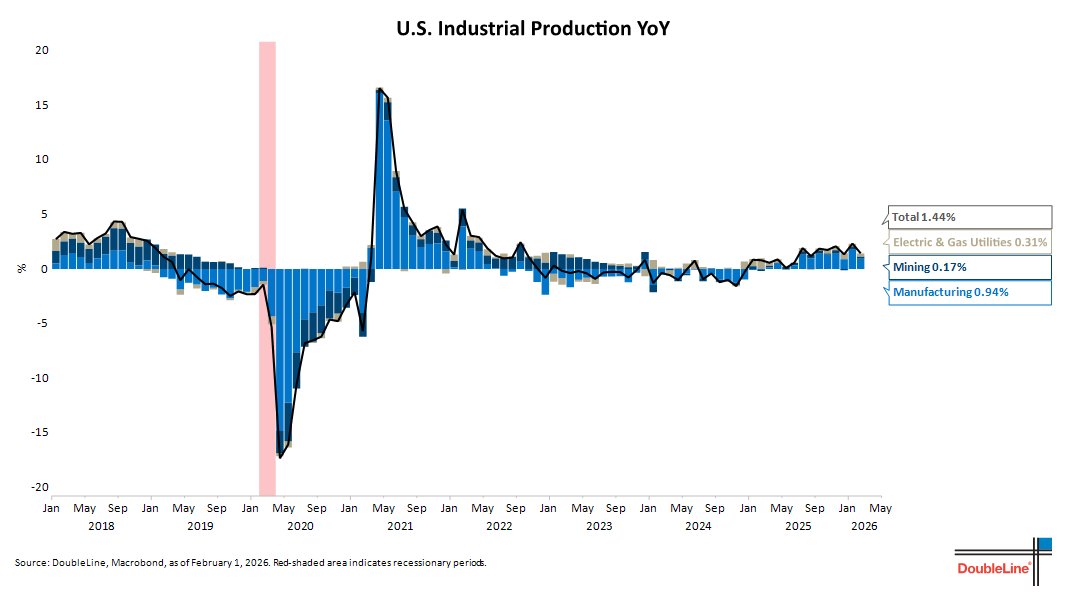

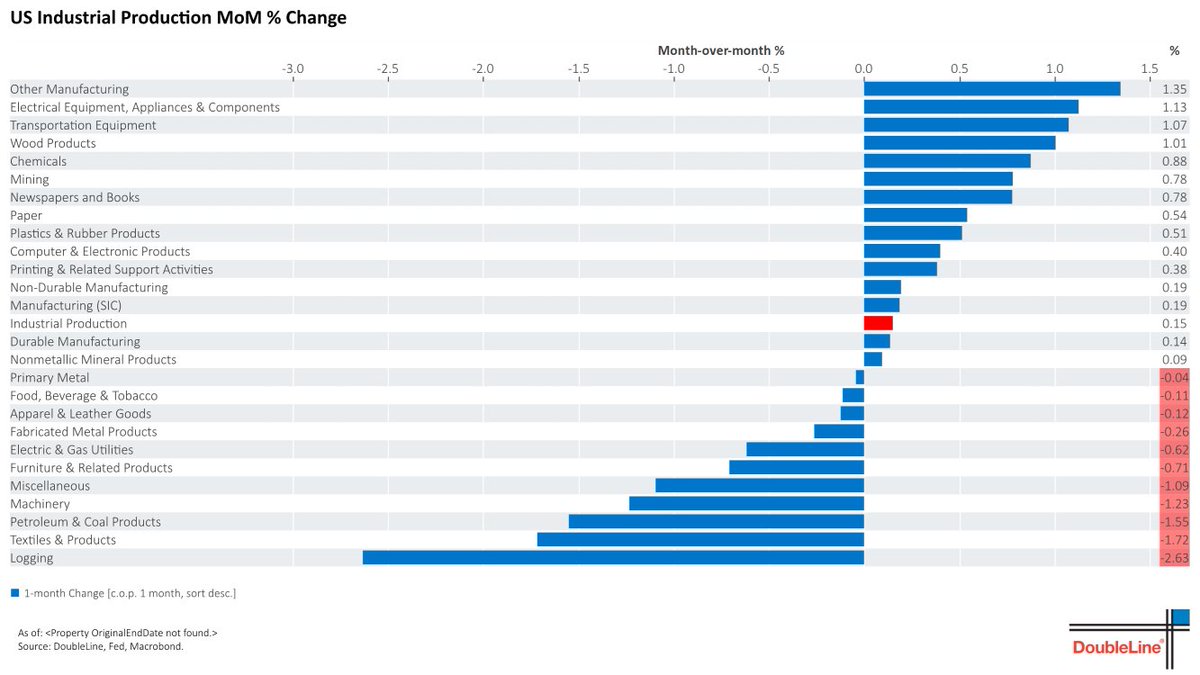

Industrial production rose slightly more than expected in February, +0.2%MoM vs. +0.1% consensus, bringing the year-over-year pace to 1.4%.

Manufacturing, +0.2%MoM vs. +0.1% consensus. Utilities -0.6%MoM, Mining +0.8%MoM.

Capacity utilization stable at 76.3%.

English

Fed funds futures “have priced in about one rate cut for the year,” per Eric Dhall on March 13. “That number had dropped to no cuts at one point this week. That number is going to be very volatile on developments in the Middle East.”

DoubleLine Capital@DLineCap

Oil’s surge is reverberating across markets: higher gasoline, firmer inflation swaps and a meaningful repricing of the 2026 policy path. The front end of the Treasury curve has adjusted in step, reflecting reduced easing expectations. linkedin.com/pulse/crude-re…

English

“Markets are hanging in despite the energy complex,” Ryan Kimmel says. “Seems like a TACO trade on the belief the energy shock will be temporary. If markets start to unhinge, maybe you could see more cuts priced into fed funds futures.”

x.com/i/spaces/1PKqr…

English

For the week ended March 13, @DLineCap's Eric Dhall and Ryan Kimmel survey down but not (yet) correcting stocks, higher yields across the curve led by the front end on inflation jitters and energy surging amid rumor-fed price swings.

x.com/i/spaces/1PKqr…

English

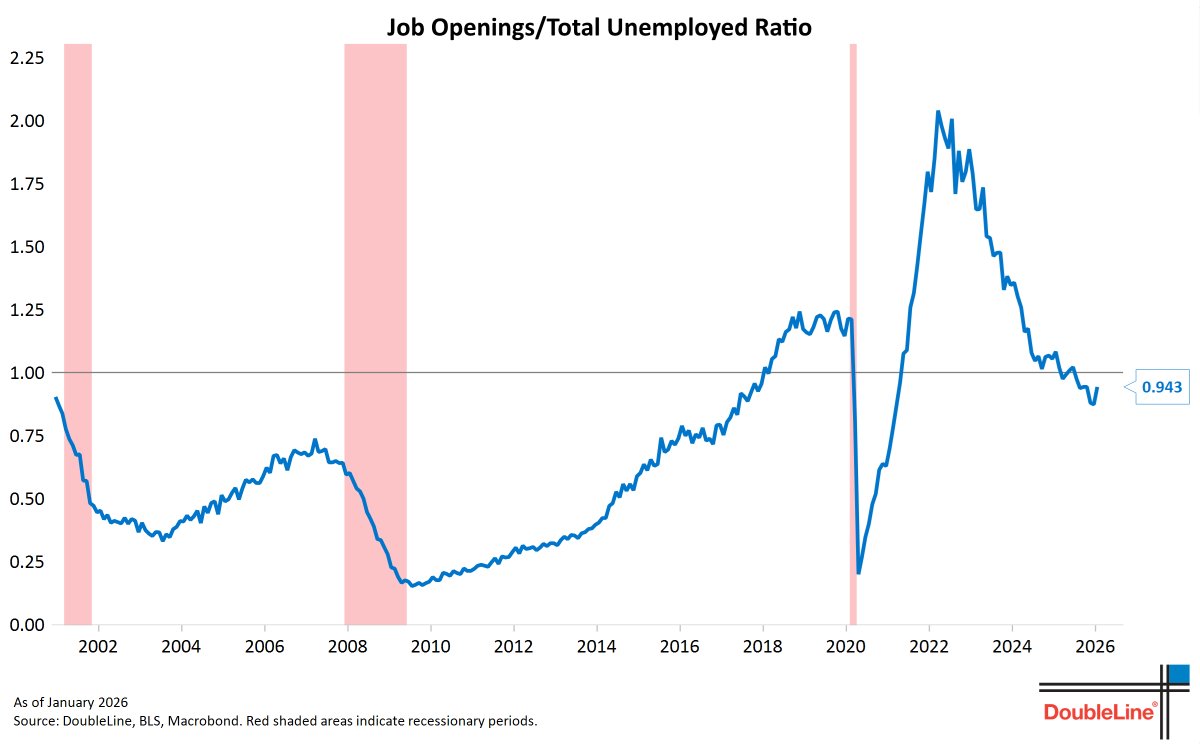

The ratio of the number of vacancies per unemployed job seeker rose to 0.94x. This points to a labor market coming back into better balance.

English

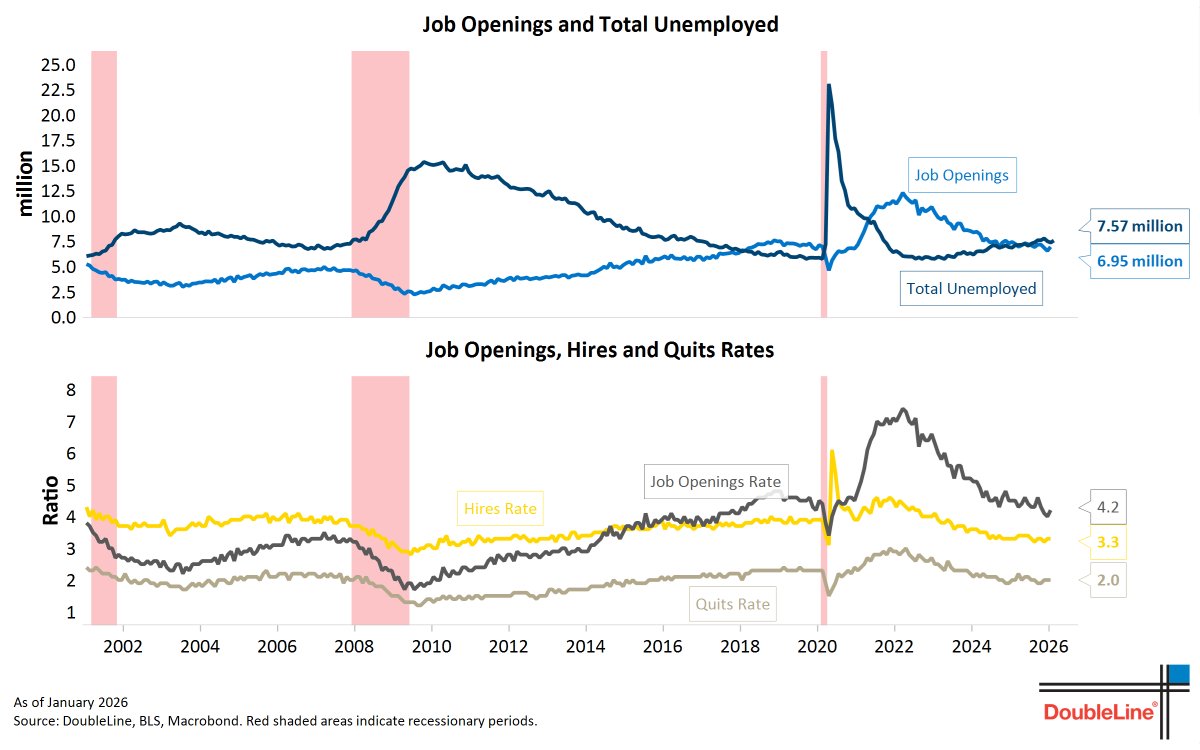

The headline JOLTS job openings data for January came in above expectations. Job openings rose to 6.95m vs. 6.75m consensus and 6.55m the previous month. This brought the job openings rate to 4.2%.

The underlying details showed hiring rates unchanged at 3.3%, but below the 2017-2019 average of 3.8%. The quits rate flat at 2.0%. The labor market continues to exhibit a “low hire low fire” dynamic.

English

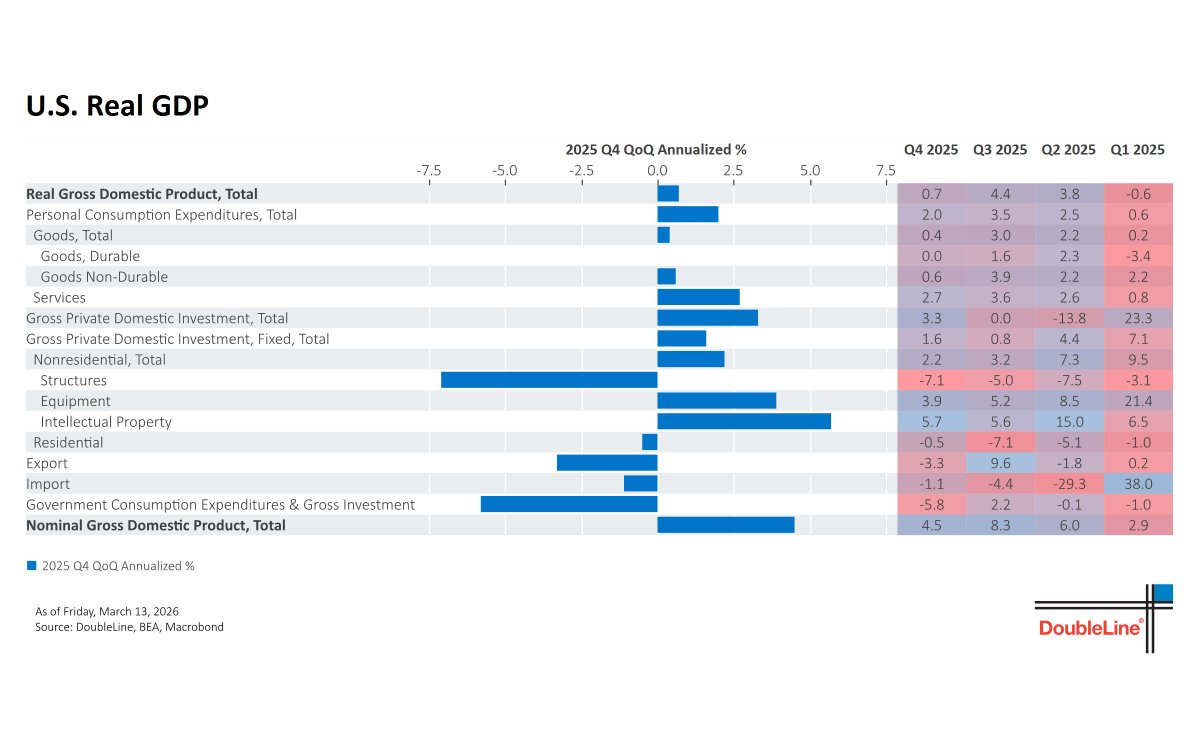

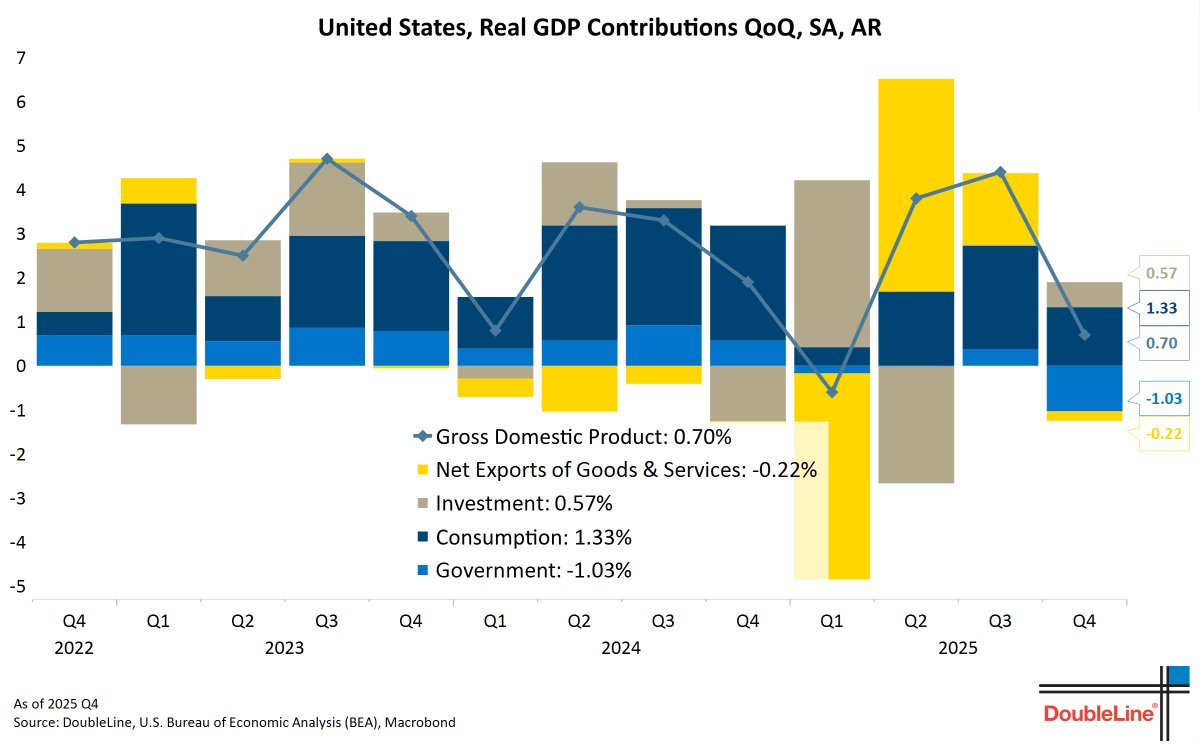

The delayed second estimate of Q4 GDP showed the economy grew by 0.7%QoQ annualized, much slower than the 1.4% original estimate.

Personal consumption revised lower to 2.0% from 2.4%. Investment grew 3.3%, driven by equipment and IP.

Government spending was a big detractor, detracting 1.0% during the quarter.

Real final sales to domestic purchasers strong at 1.9%.

English

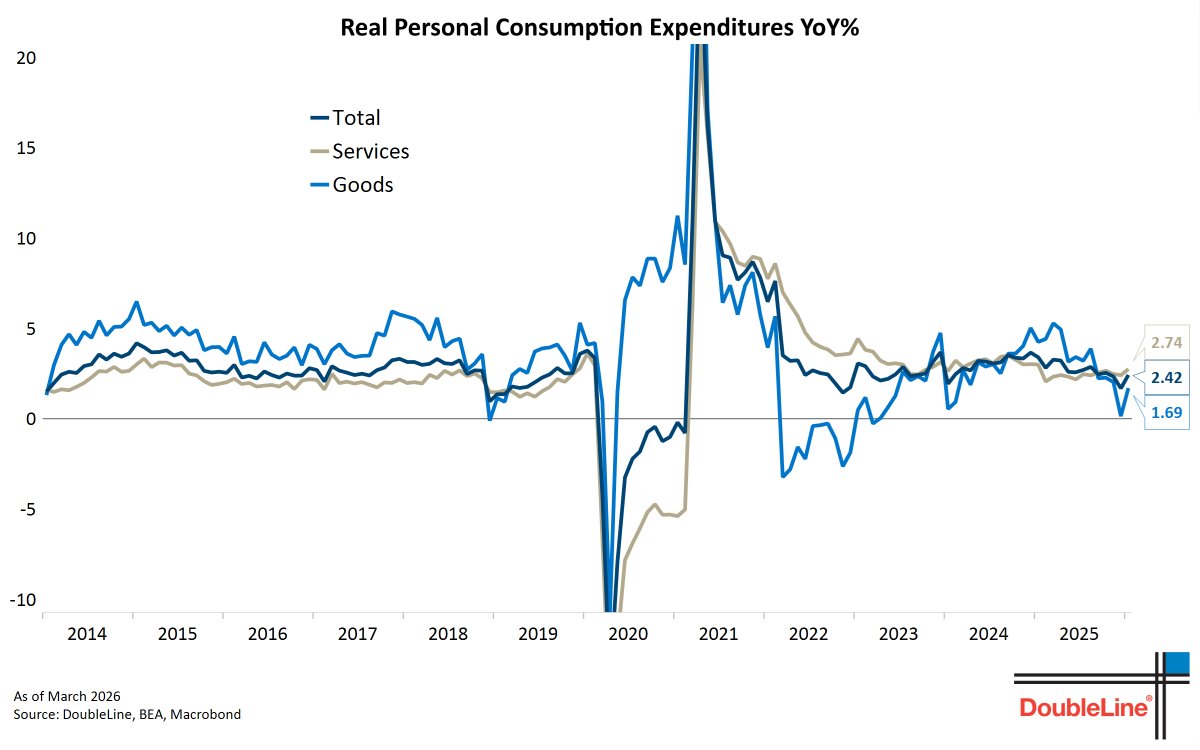

Real spending +0.10%MoM. Real goods spending -0.42%MoM while real services spending rose +0.33%MoM.

Real spending is running at 2.4% year-over-year.

English

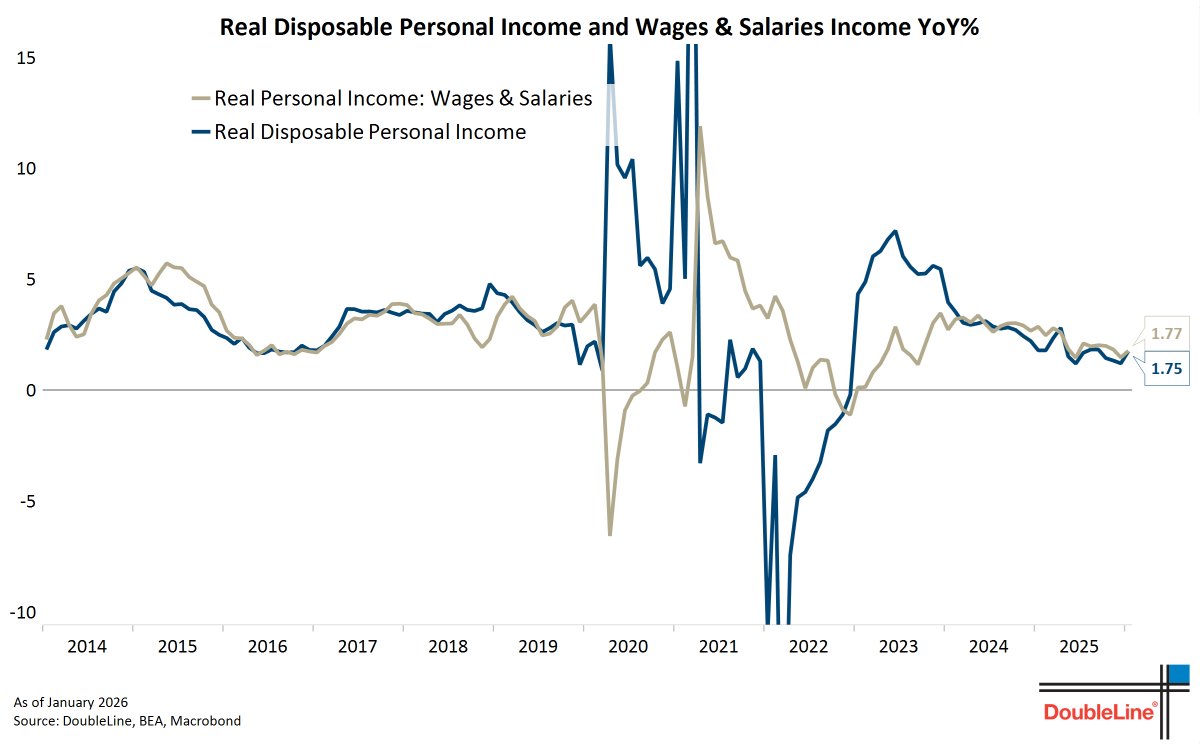

Personal income rose 0.4%MoM in January; wage income increased 0.5%MoM.

On a year-over-year basis, real wages & salaries growth accelerated to 1.8% and real disposable personal income +1.8%.

English