Mike@MikeLongTerm

$GRAB| The Fundamental vs Sentiment 🧵

Not Financial Advice!

Just a long well-researched thread ✍️

In the last 14-15 months, I have seen a very emotional ride when the share price was down/flat and rised very fast and how most retail investors reacted to it, and institutions kept buying more and more.

I have to say, the game has not changed. I will use this thread to address some of the new changes and development, and where I think the business is going long term. And of course, I'm certainly buying this high quality compounder at a massive discount just like other long term before the market gets it! I don't plan to overpay anytime soon.

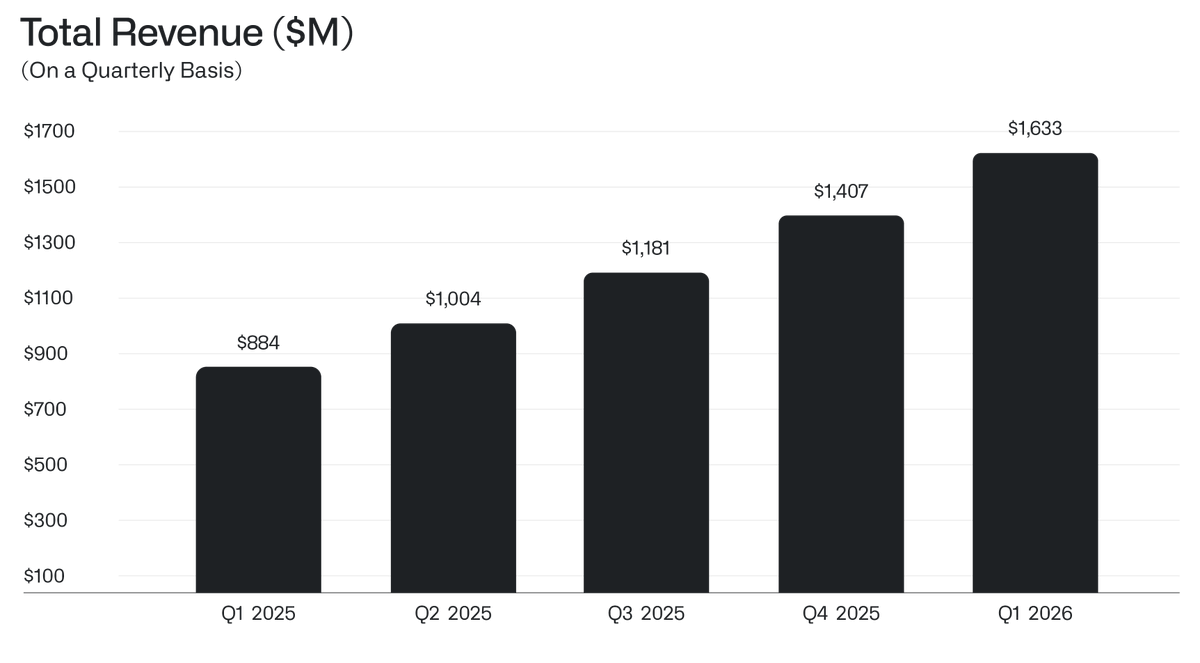

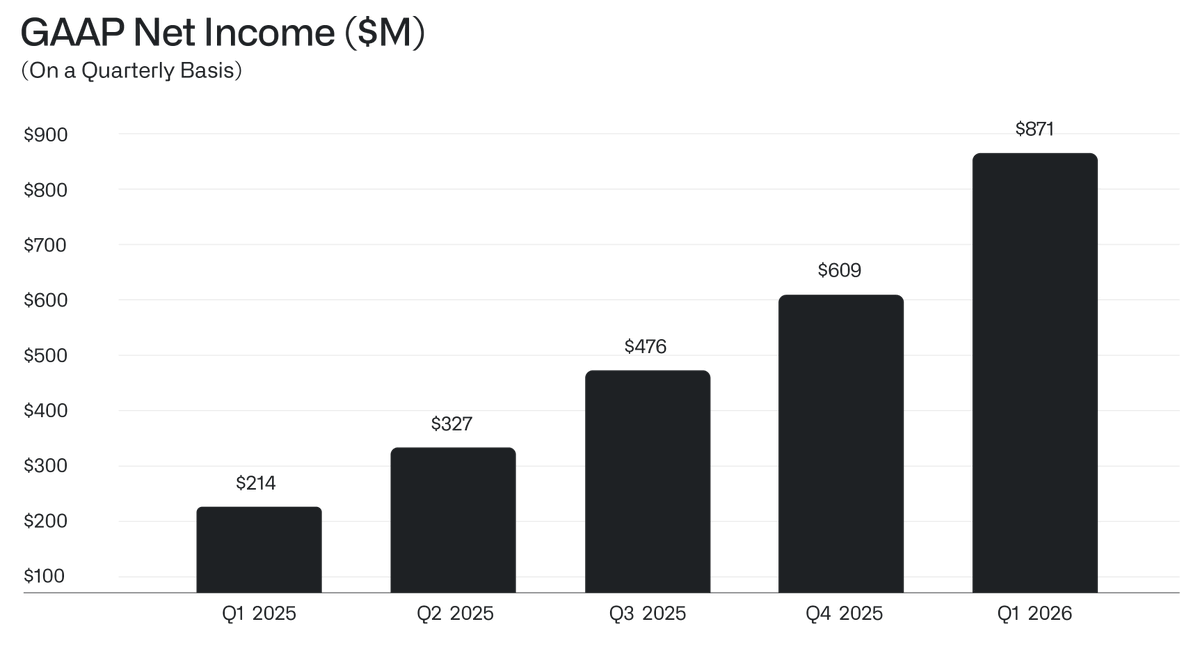

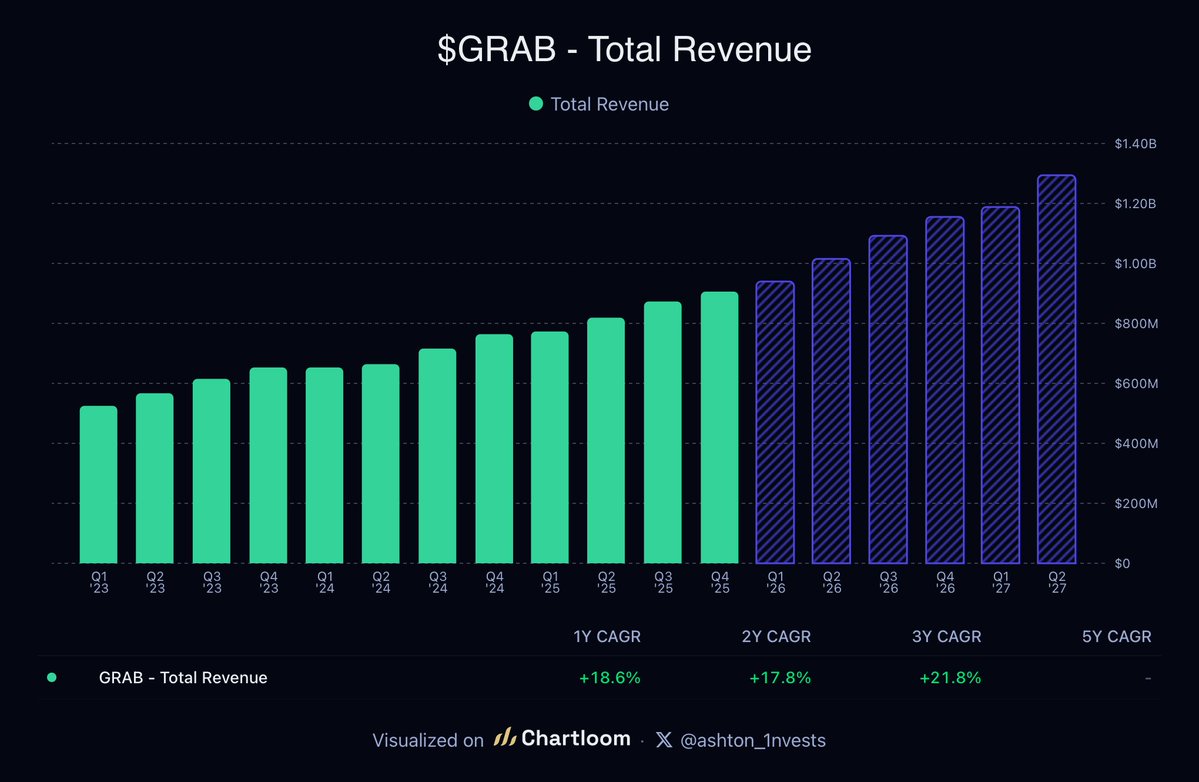

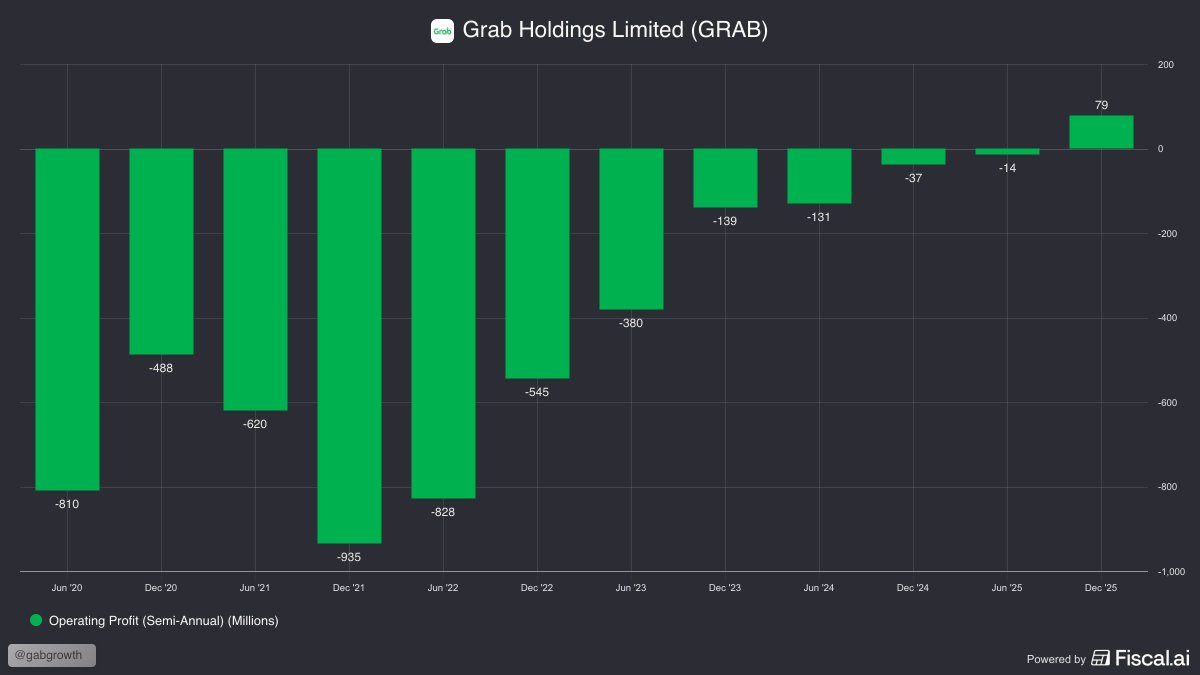

Grab Holdings has transformed dramatically from a ride-hailing focused business into a diversified Southeast Asian SuperApp, achieving its first full-year net profit in FY 2025 alongside positive adjusted free cash flow. This shift stems from strategic expansion across mobility, deliveries, financial services and B2C combined with monetization innovations like the platform/service fee model introduced around 2020. These changes have improved unit economics, scaled the ecosystem, and created a virtuous cycle benefiting consumers, drivers, and merchants through higher volumes and greater transparency.

1. The new regulation in Indonesia

President Prabowo Subianto signed presidential regulation on May 1 2026 that Driver minimum share: 92% of the base fare, where platform commission at 8% maximum. There is no clause or requirement for $GRAB or similar platforms that they cannot add service/platform fees.

Context: around 2020, Grab shifted its monetization by introducing a transparent platform/service fee (separate from base commissions/fares). This decoupled platform earnings from pure commission percentages, allowing compliance with regulatory caps ( Indonesia's recent 8% commission limit on platforms, which does not prohibit separate service fees). You can read the adjustment below, where drivers will get 92% and the service/platform fee will be adjusted to make it sustainable along with minor changes in incentives. Incentives longer term will most likely to attract new drivers and to keep supply sufficient when demand is high.

However, incentives have been declining steadily as % to revenue since 2021. From 13%+ peaks in 2021 to ~10% in 2025 → a reduction of 3 percentage points (or ~20–25% relative decline from highs). This is despite GMV growth (On-Demand GMV scaled dramatically from smaller bases in 2020 to $22.1B in 2025).

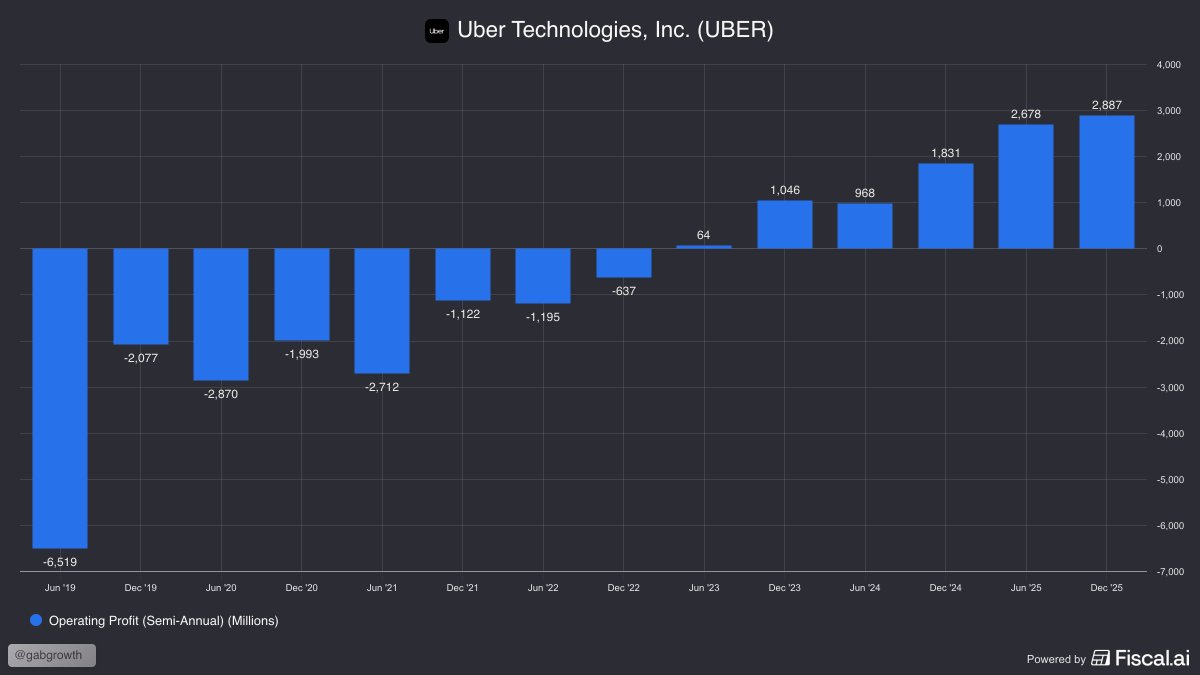

IMO, this will push $GRAB to dominate 95% market share sooner for a very long time, since $GOTO would not last that long anymore with Crack down on its Fin-Arm and now on its On-demand without the scale and balance sheet like $GRAB has.

2. Bottom of Pyramid| The Fundamental

I often talked about this since I started my position on $GRAB. I know the full thesis is 5 Billion people TAM, I absolutely love Anthony's ambition, but I'm also realistic to my investment. My projection is sticking to 800m people TAM. I do not rule out expansion, as I was the only one calling for 2026 expansion and management bought FoodPanda Taiwan.

It is completely doable to reach 350-400m MTUs and 250-300m GrabUnlimited subscirbers within 6 years(long term). GRAB should be able to generate $8-9B revenue per quarter, and GrabFin + Delivery will be a significant % of overall revenue along with Mobility and B2B. I also expect 12-15% revenue generated from $30B Loan Book per quarter by 2032 or $3.6-$4.5B revenue per quarter. Grab-Fin has more than just lending like Insurance, investment, payment, digital banking... but Revenue generated as % from Total Loan book is an easier metric to track this business long term. For now Grab generated 8.4% off $1.18B loan portfolio in Q4 2025. It will get more efficient and profitable over time.

The speed and quality of Grab's MTU growth is the clearest signal that the affordability pivot is working. From 41.9 million MTUs in Q3 2024, the platform scaled to 50.5 million MTUs in Q4 2025 , adding nearly 9 million transacting users in six quarters. Critically, this growth is demand-led: transaction volumes are consistently outpacing both MTU and GMV growth, which means users are transacting more frequently, not just joining the platform.

Every single quarter has reached a new all-time high. Each MTU record has been set in a different macro environment where short sellers claimed Grab would be destroyed or hit $0, Lunar New Year seasonality in Q1, Indonesia macro uncertainty in Q3 , and the platform has powered through all of it. This consistency is the hallmark of a high quality compounding SuperApp growth, not a promotional sugar rush.

Grab already has approximately 119 million Annual Transacting Users as of recent filings, representing ~17% of Southeast Asia's population. The gap between 119M ATUs and 50.5M MTUs is the activation opportunity , re-engaging lapsed users into monthly habitual use.

Indonesia , Grab's largest market with over 200 million people , had only approximately 4% of users as monthly transacting users as of 2025. This single market could contribute 20–40 million incremental MTUs as smartphone and internet penetration deepens.

Vietnam & Philippines are SEA's • fastest-growing digital economies, each with populations of 90–100 million, remain significantly underpenetrated relative to Singapore and Malaysia. Infrastructure investment and localized affordability products are progressively addressing this.

GrabMart, GrabMore (grocery add-on to food orders), GrabFinancial, and Advanced Booking are bringing entirely new user cohorts who may not have engaged with Grab through ride-hailing or food delivery alone.

Consolidation in SEA to 90-95% market share and affordability are a growth multiplier that actually expands margins through scale. Margin has expanded for 16 consecutive quarters, and will continue to expand upward QoQ. You can read my GMV/MTU and other threads to understand more why Grab is winning!

3. From Ride-hailing to a much more diversified sources of revenue or AKA SuperApp

Grab launched in 2012 as a taxi-hailing service (primarily Mobility). Pre-2020, revenue was overwhelmingly concentrated in ride-hailing, with limited diversification. The COVID-19 pandemic accelerated expansion into Deliveries (food, groceries, ...), while Financial Services (payments, lending, insurance via GrabPay, GXS Bank...) emerged as a high-growth, higher-margin pillar. The SuperApp model integrates everything into one platform, driving cross-usage, higher monthly transacting users (MTUs), and lifetime value.

Currently, the market is only seeing $GRAB as ride-hailing service/app, and trading at the lowest P/S in it histroical range. Grab highest P/S was 19.5 from IPO to now at 4.43. If u consider the Equity value, Cash, and assets, Grab is actually trading at negative market cap now with very little debt.

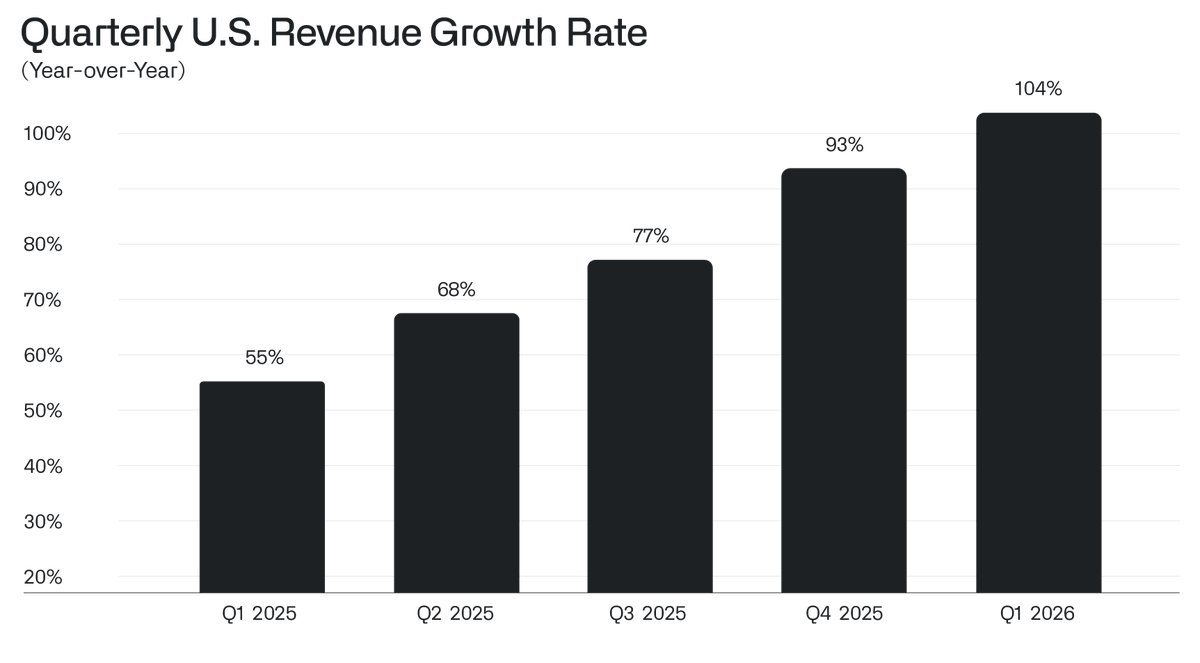

Years ago (2019–2020), Mobility dominated (often >70–80%+ of revenue pre-diversification push). By 2025, Deliveries is the largest segment, Mobility remains core but no longer singular, and Financial Services (minimal pre-2021) now contributes meaningfully with strong growth. On-Demand GMV (Mobility + Deliveries) hit $22.1 billion in 2025 (+21% YoY), with MTUs averaging 47.2 million (+14% YoY) and reaching 50.5 million in Q4. GMV per MTU rose +4% YoY, reflecting deeper engagement across services.

GrabFin revenue will probably a very large % of overall revenue, as much as 30-35%. I was initially projecting it to be 10-15%, but Q4 2025 confirmed a similar directional trend to Wechat on Financial Serivce, and Growing Users, Subscription and Ads are like Amazon business model but asset-light model.

This diversification reduces single-segment risk like this week( regulatory or demand shocks in rides) and leverages the SuperApp flywheel:

one app drives seamless cross-selling ( ride → food delivery → payments/lending/insurance/wealth), boosting retention and monetization.

4. Understanding the structural advantages and competitive moat| Why $GRAB is winning long term

Grab's competitive moat is the interconnectedness of its verticals. With 50.5+ million MTUs, 15 million+ merchant partners, and driver-partners processing 10 million+ transactions daily, the platform generates network effects that single-vertical rivals cannot replicate. Soon $GOTO will add 25-30m MTUs, 3m+ drivers and 14m+ merchants

• More users → more merchant partners → better selection → more users.

• More driver supply → lower wait times and surge pricing → more rides → more driver income → more driver supply.

• More food orders → better AI routing → batched deliveries → lower per-order cost → lower prices → more food orders.

• More GrabPay transactions → better credit data → lower credit risk → more GrabFinancial penetration → more ecosystem lock-in.

Conclusion:

The case for Grab reaching 350–400 million MTUs and 250–300 million GrabUnlimited subscribers is ultimately a base case for Southeast Asia's digital economy reaching its full potential , and for Grab being the digital infrastructure through which that potential is realized. No other platform in the region combines the transaction scale, the ecosystem breadth, the financial services overlay, the AI capability, and the $7+ billion balance sheet that Grab brings to this opportunity.

And this is only 800m people TAM that I stick to. It is entirely possible that $GRAB would expand to 1-2B people TAM within 6 years. This is a high purpose mission for Anthony, I think you should watch this entire video to get to know him more.

The near-term evidence is unambiguous: MTUs are at all-time highs every quarter. GMV/MTU is rising even as user base expands. Transactions are outpacing both GMV and MTU growth. GrabUnlimited subscribers are at all-time highs and represent an ever-larger share of the delivery base. Adjusted EBITDA is compounding at 60% annually. Net profit has arrived. The affordable push , Saver Deliveries, Saver Transport, Group Orders, GrabMore , is re-accelerating both user acquisition and engagement frequency simultaneously.

The SuperApp is now self-sustaining, with strong tailwinds in Southeast Asia's digital economy. Risks remain like regulation, macro may impact near-term price action, but the absolute fundamental is strengthening and the strongest today than before.

A Cash Generating Cow will return capital to shareholders whether short sellers/bears like it or not long term. I believe short sellers will stop manipulating price action at some point, and I wont be able to time it.

Grab decoupled sustainable economics from regulatory caps, passing real savings to consumers while enabling drivers and merchants to earn more in absolute terms through higher volumes. Diversification into high-margin financial services (now the fastest-growing segment) extends that flywheel, delivering micro-lending, digital wallets, and banking to the underbanked millions who power the platform every day.

Anthony knows that Grab only truly succeeds when the communities it serves succeed. Uplifting informal workers, small merchants, and low-income users through economic empowerment isn’t a side mission it is the moat. In a region where the base of the pyramid represents the vast majority of the addressable market, this inclusive model creates the deepest network effects, the strongest retention, and the most durable and high quality compounding growth. The SuperApp doesn’t just serve Southeast Asia, it elevates it. And in doing so, it positions $GRAB SuperApp for the decades-long winner-take-most opportunity that few other platforms can claim.

Not Financial Advice!