Sabitlenmiş Tweet

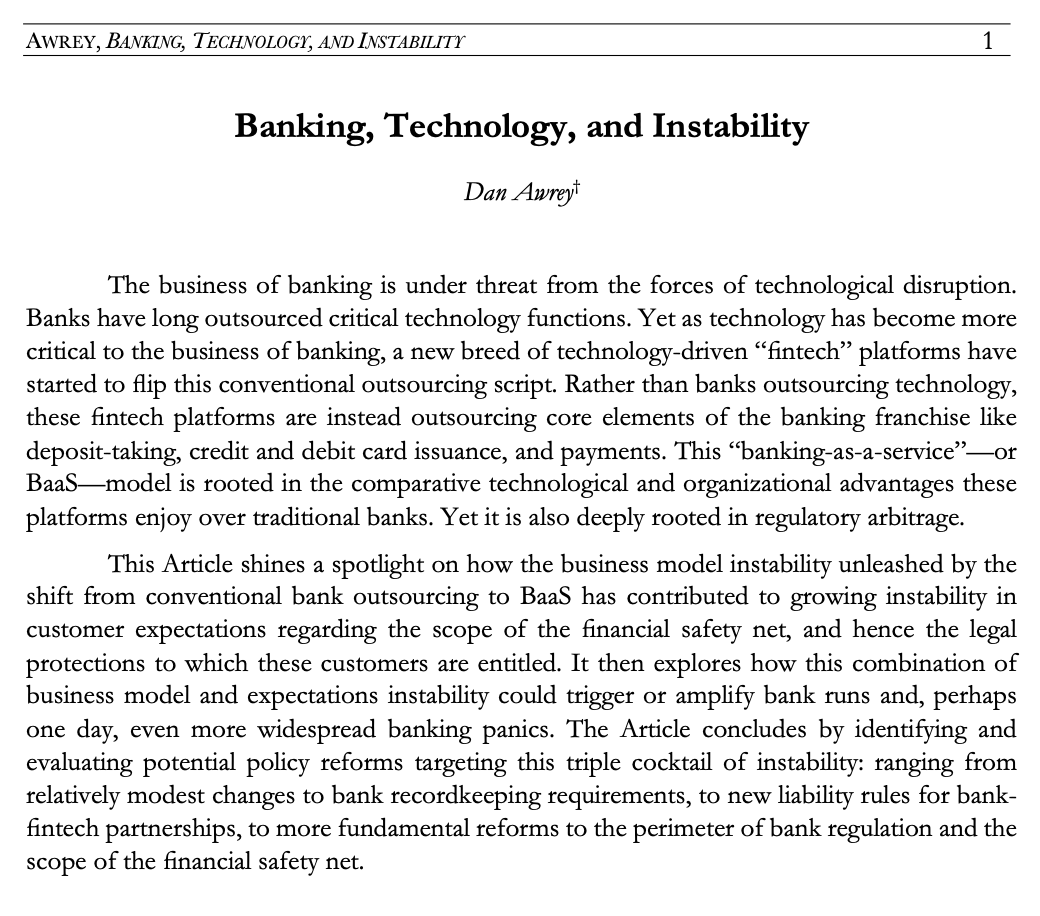

📢👷🏼🛠️ NEW WORKING PAPER exploring the impact of technological disruption on bank business models, consumer expectations, and financial stability. Questions, comments, and suggestions all very welcome: papers.ssrn.com/sol3/papers.cf…

English