Devang B

50 posts

I bought a new stock for my portfolio today. Only the second new position I have started this entire year.

It is a $3.5b small cap non tech company that I have admired for many years, but I was never able to buy it because the valuation always felt too expensive. I think one of the hardest things in investing is accepting that a great business and a great investment are not always the same thing. Sometimes the business is incredible for years while the stock itself is a terrible investment simply because expectations and valuation became disconnected from reality.

Ironically my first purchase this year was $NOW, which at the time was considered one of the worst buys imaginable on this platform and I got totally killed in here. People were acting like the business completely broke overnight. A few weeks later sentiment flipped and suddenly it became a loved companies again. The fascinating part is the actual business barely changed during that period. Mostly the stock price and the narrative changed.

That is one of the biggest lessons over time. Social media sentiment moves much faster than business fundamentals. Investors often confuse volatility with change. A stock declining 25% does not automatically mean the business is suddenly 25% worse.

Another thing I have learned is that patience in investing looks stupid until it suddenly looks disciplined. I only bought 2 new stocks this year because truly great opportunities are actually pretty rare. Most people trade constantly because activity feels productive, but some of the best returns I have ever had came from doing almost nothing for long stretches and then acting aggressively when price, expectations, and quality finally aligned.

What interests me most is not next quarter or even next year. I care far more about what this business can potentially look like 5-10 years from now. Is the moat strengthening? Are the unit economics improving? Does management allocate capital intelligently? Those questions matter infinitely more to me than whether social media currently loves or hates the stock.

I no longer really share my exact buys and sells publicly the way I used to. Not because I am trying to be secretive, but because I do not want people blindly copying me without fully understanding the risks, valuation, time horizon, etc. A stock that fits my portfolio, psychology, and long term expectations may be completely wrong for someone else.

I think social media has created this idea that investing is about copying and cloning instead of thinking. But real investing is much deeper than that. Two people can buy the exact same stock and have completely different outcomes because one understands what they own and the other is simply following a narrative.

🌹

English

@realroseceline Knowing you and reading your posts - Synopsys, Lam Research and KLA? I think Broadcom at 30% lower beats them all

English

There are 3 businesses on this list I really like, any guesses?

Daniel Newman@danielnewmanUV

$QCOM follows $MU and the memory names as the low PE names in semis. When will people start to realize that this cycle is different?

English

@BarrySchwartzBW I enjoy your podcasts! Very decent and I’m sure you guys will do well in the fullness of time

English

bunch of names with negative ytd returns even though earnings are growing - even accelerating - I own all - clients own most.

English

@realroseceline Do you think Domino’s can become the next McDonald’s?

English

The Installed Base — One of the Most Durable Moats in Investing.

The concept is simple: a company sells a piece of capital equipment or a platform. That machine, device, or system becomes deeply embedded in the customer’s operation.

From that point forward, the company generates years — sometimes decades — of high-margin recurring revenue through consumables, parts, software, and services tied directly to that installation.

The customer can’t easily leave. Switching means downtime, retraining, recertification, and massive capital expenditure. The installed base becomes the moat.

Several companies that have mastered this model:

$ISRG — every da Vinci surgical system placed in a hospital is a long-term revenue stream. Instruments, accessories, and services follow every installation. Surgeons train on it, hospitals build workflows around it, and switching is virtually unthinkable.

$GE — jet engines are sold at thin margins. The real business is the decades of parts, maintenance, and services that follow every engine installed on a commercial or military aircraft. One engine. Decades of revenue.

$ASML — every EUV lithography machine placed in a fab locks that customer into ASML’s ecosystem of components, software, and services. There is no alternative. The installed base is global and irreplaceable.

$LRCX — semiconductor fabs are built around Lam’s etch and deposition equipment. Once their systems are qualified and integrated into a production process, the switching costs are enormous. The installed base grows with every new fab built globally.

$IDXX — veterinary clinics and labs run on Idexx diagnostic analyzers. Once placed, those instruments generate a continuous stream of proprietary reagent and consumable revenue. The analyzer is the razor. The consumables are the blades.

$DHR — sells diagnostic and life science instruments into labs, hospitals, and research facilities worldwide. Once embedded, the instruments anchor years of high-margin consumable, reagent, and software subscription revenue.

English

𝐋𝐢𝐟𝐞 𝐡𝐚𝐜𝐤: 𝐭𝐡𝐞 𝐨𝐧𝐞 𝐭𝐡𝐢𝐧𝐠 𝐲𝐨𝐮 𝐜𝐚𝐧 𝐚𝐥𝐰𝐚𝐲𝐬 𝐜𝐨𝐧𝐭𝐫𝐨𝐥 𝐢𝐬 𝐲𝐨𝐮𝐫 𝐚𝐭𝐭𝐢𝐭𝐮𝐝𝐞.

Think about that for a second.

In every situation — no matter how difficult — there is a split second before you react. A window.

And in that window, you get to choose:

Glass half full or glass half empty.

𝐓𝐡𝐚𝐭 𝐜𝐡𝐨𝐢𝐜𝐞 𝐢𝐬 𝐚𝐥𝐰𝐚𝐲𝐬 𝐲𝐨𝐮𝐫𝐬. 𝐍𝐨 𝐨𝐧𝐞 𝐜𝐚𝐧 𝐭𝐚𝐤𝐞 𝐢𝐭 𝐟𝐫𝐨𝐦 𝐲𝐨𝐮.

So if that’s true — if you always have the option to look at the other side, to find the positives, the hidden blessings, the lesson you’ll carry for life — 𝘸𝘩𝘺 𝘸𝘰𝘶𝘭𝘥 𝘺𝘰𝘶 𝘸𝘪𝘭𝘭𝘪𝘯𝘨𝘭𝘺 𝘤𝘩𝘰𝘰𝘴𝘦 𝘰𝘵𝘩𝘦𝘳𝘸𝘪𝘴𝘦?

I get it. It’s not easy. Especially if you haven’t practiced it. But here’s what’s remarkable about the human brain — the more consistently you choose the positive lens, the more natural it becomes. You’re not just changing your mindset. You’re literally rewiring your brain.

At some point, glass half full stops being a conscious choice and starts being your first instinct.

And when that happens? It’s liberating.

𝙏𝙝𝙚𝙧𝙚’𝙨 𝙖𝙡𝙨𝙤 𝙨𝙤𝙢𝙚𝙩𝙝𝙞𝙣𝙜 𝙖𝙡𝙢𝙤𝙨𝙩 𝙢𝙮𝙨𝙩𝙚𝙧𝙞𝙤𝙪𝙨 𝙖𝙗𝙤𝙪𝙩 𝙜𝙚𝙣𝙪𝙞𝙣𝙚 𝙥𝙤𝙨𝙞𝙩𝙞𝙫𝙞𝙩𝙮 — 𝙞𝙩’𝙨 𝙘𝙤𝙣𝙩𝙖𝙜𝙞𝙤𝙪𝙨, 𝙞𝙩 𝙖𝙩𝙩𝙧𝙖𝙘𝙩𝙨 𝙩𝙝𝙚 𝙧𝙞𝙜𝙝𝙩 𝙥𝙚𝙤𝙥𝙡𝙚 𝙖𝙣𝙙 𝙤𝙥𝙥𝙤𝙧𝙩𝙪𝙣𝙞𝙩𝙞𝙚𝙨, 𝙖𝙣𝙙 𝙞𝙩 𝙝𝙖𝙨 𝙖 𝙦𝙪𝙞𝙚𝙩 𝙬𝙖𝙮 𝙤𝙛 𝙧𝙚𝙬𝙖𝙧𝙙𝙞𝙣𝙜 𝙮𝙤𝙪 𝙤𝙫𝙚𝙧 𝙩𝙞𝙢𝙚 𝙞𝙣 𝙬𝙖𝙮𝙨 𝙮𝙤𝙪 𝙣𝙚𝙫𝙚𝙧 𝙚𝙭𝙥𝙚𝙘𝙩𝙚𝙙.

So next time life throws something at you — before you react, pause. Just one second.

And ask yourself:

What are all the positives I can take from this?

Flood your brain with them. Make it a habit.

English

@wealthmatica Maybe it’s cheap but you have to compare apples to apples bc he sold half a billion and bought $10m

English

$PANW CEO bought freaking $10M worth of shares...

Yeah I think it's fair to say Cyber is oversold.

Blossom@meetblossomapp

Massive insider buy: Palo Alto Networks CEO just bought $10 million dollars worth of shares. Total shares bought: 68,000 $PANW

English

@realroseceline So true and timely for you to point out.. I think Meta and potentially others could see significant drawdowns if capex discipline keeps fading

English

$META - Don’t forget who told you first while the market was doing backflips 🌹

Rose Celine Investments 🌹@realroseceline

Fasten your “CAPEX Seatbelt”, $META reports today and Zuckerberg’s will probably announce another massive jump in capital spending and SBC to pay for all those brilliant engineers he’s hiring. The crowd will cheer and analysts will call it “visionary”, the stock might even rip. But real investors know what this means: lower free cash flow, higher risk, and a steeper hill to climb for returns. You’re not buying ambition, you’re buying what’s left after the spending. 🌹

English

@FinanceJack44 Yea but they bought at exceptional prices - these prices are “good” but nowhere near exceptional

English

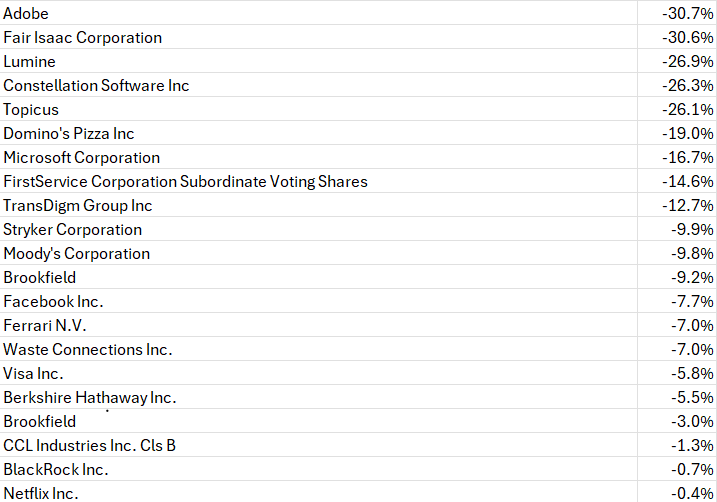

I’ve seen a lot of people dunking on “compounding bros” recently, largely because favorites like $FICO $SPGI and $MA are down big YTD.

Short term movements don't wreck the strategy though.

Many investors have had incredible success using this relatively simple approach:

Chris Hohn: 18% CAGR over 22 years

Warren Buffet: 20% CAGR over 60 years

Dev Kantesaria: 15% CAGR over 19 years

I don't think these guys are too concerned with the current pullback.

English

@DimitryNakhla Watch out for Danaher and Copart - compounders which rarely go noticed and whilst the bottom may not be in, these are levels where double digit compounding and multiple expansion result in a lollapalooza effect

English

10 Quality Stocks Trading Within 15% of Their Lowest P/E Multiple In The Past 10 Years 💵

Stock Lowest P/E (10Y) | NTM P/E

1. $NOW 24x | 27x

2. $VRSK 23x | 26

3. $MA 22x | 25x

4. $DHR 19x | 22x

5. $AMZN 26x | 27x

6. $V 21x | 22x

7. $CPRT 19x | 20x

8. $CSU 15x | 16x

9. $DLO 12x | 13x

10. $MELI 29x | 29x

English

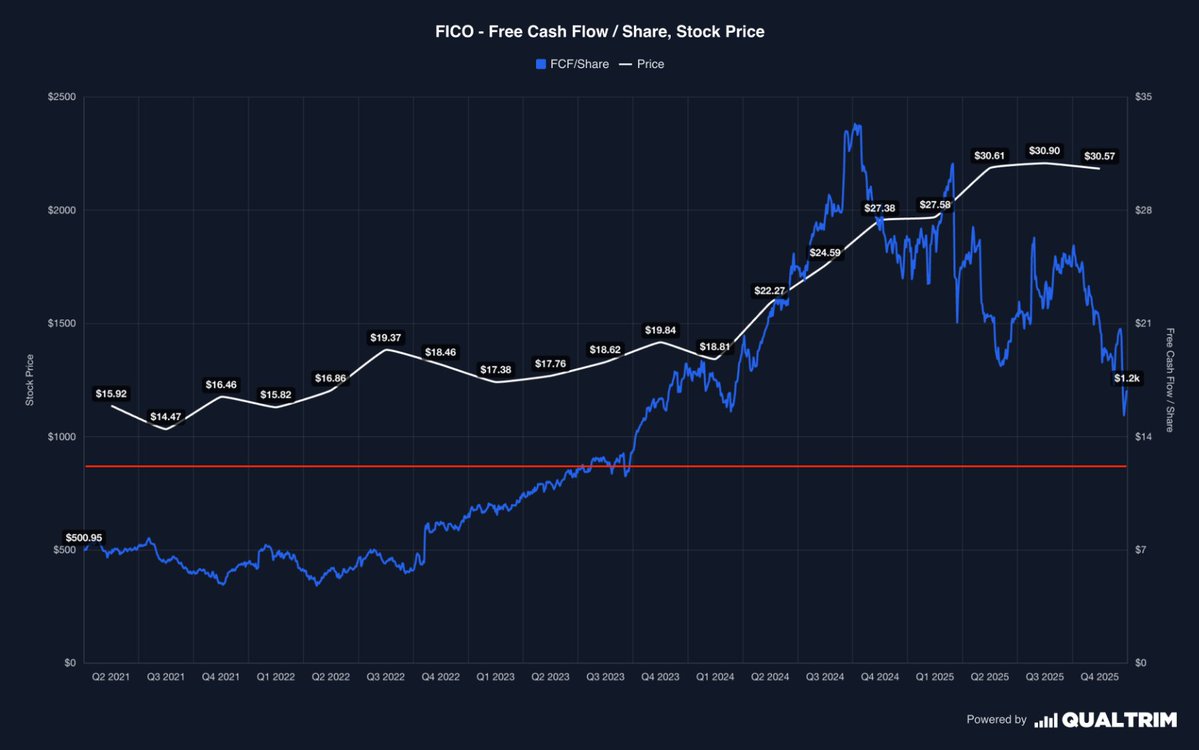

@realroseceline @wealthmatica I think valuation really matters but less so for high quality companies - this being said, FICO is even a good buy at 30x earnings, but it’s the valuation discipline that distinguishes great from good. Don’t get me wrong - “good” is still an exceptional outcome

English

@wealthmatica Why is it an obviously buy at 20.7x earnings but for example not 22x or 23x earnings? Is there really that big of a difference if you buy it and hold it for the next 10 years?

English

OK honestly though...

When does $FICO become an obvious buy?

For me, that's around $935/share.

- Forward P/E: 20.7x

$FICO

English

@stonkmetal How would the returns have been had you built a 20% stake in each of these? I predict very strong

English

I try to own compounding machines at reasonable prices. Here are 5 great compounders that are sadly too expensive for me📈

1. Rollins $ROL (29x forward EV/EBITDA)

2. Heico $HEI (29x)

3. IDXX Labs $IDXX (36x)

4. Mettler-Tolado $MTD (27x)

5. Cintas $CTAS (21x)

Who else?

English

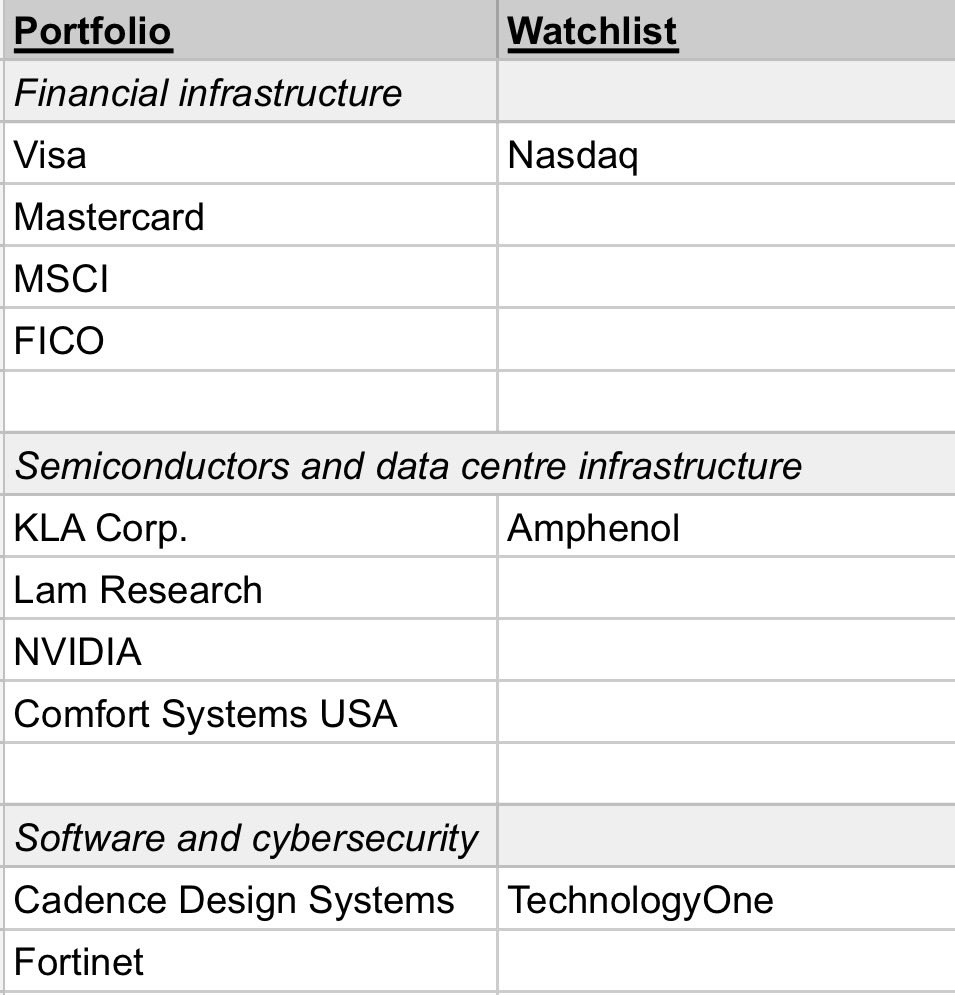

@long_equity Amazing portfolio - just add when Mr Market gets depressive and sell when it gets euphoric

English

Here’s the Long Equity portfolio and the main companies in the watchlist. What would you add or remove?

English

@realroseceline With your note, are we admitting narratives follows price action? Or why don’t we just agree that Mr. Market is overly depressed at the moment providing opportunity to the rational investor?

English

More thoughts on $SE

What spooked the market today was not just that growth is slowing. It was the quality of the growth, and that is perceived to be a much bigger deal. In other words the thing I talk about frequently, the “economics”.

$SE is still growing GMV fast and guiding to 25% next year, which on the surface sounds great. But GMV does not pay shareholders, EBITDA aka profitability does. What really matters is the economics, ie how much profit you generate for every dollar of GMV, and that ratio got worse mainly because logistics costs increased. When logistics eats your take rate, the operating leverage weakens.

For years the bull case was straightforward. Scale the marketplace, improve logistics, monetize better, and let margins expand over time. If GMV grows fast then EBITDA should grow even faster by design.

This quarter the market saw something different. GMV growing, but EBITDA per GMV falling. Then guidance for solid growth next year without an improvement in profitability. That combination made the market nervous because it raises the obvious question. If growth comes back but margins do not, what exactly are we scaling?

Either growth is being subsidized (again), or logistics costs are higher than expected, or competition is forcing $SE to give up economics to defend market share. None of those outcomes are good for long term margins, and long term margins are what ultimately drive valuation (ie $DLO).

The market will tolerate an investment phase if it believes operating leverage is coming later (ie $MELI). What the market punishes is growth that does not convert into profitability. Think of it like a treadmill where you are running fast but not actually going anywhere.

The debate now is whether this is temporary or structural. If logistics costs are elevated because of expansion, then margins can recover once things normalize.

That is what actually spooked the market. It’s not just about growth, but the fear that growth may not be as profitable as assumed.

I am long $SE.

🌹

English

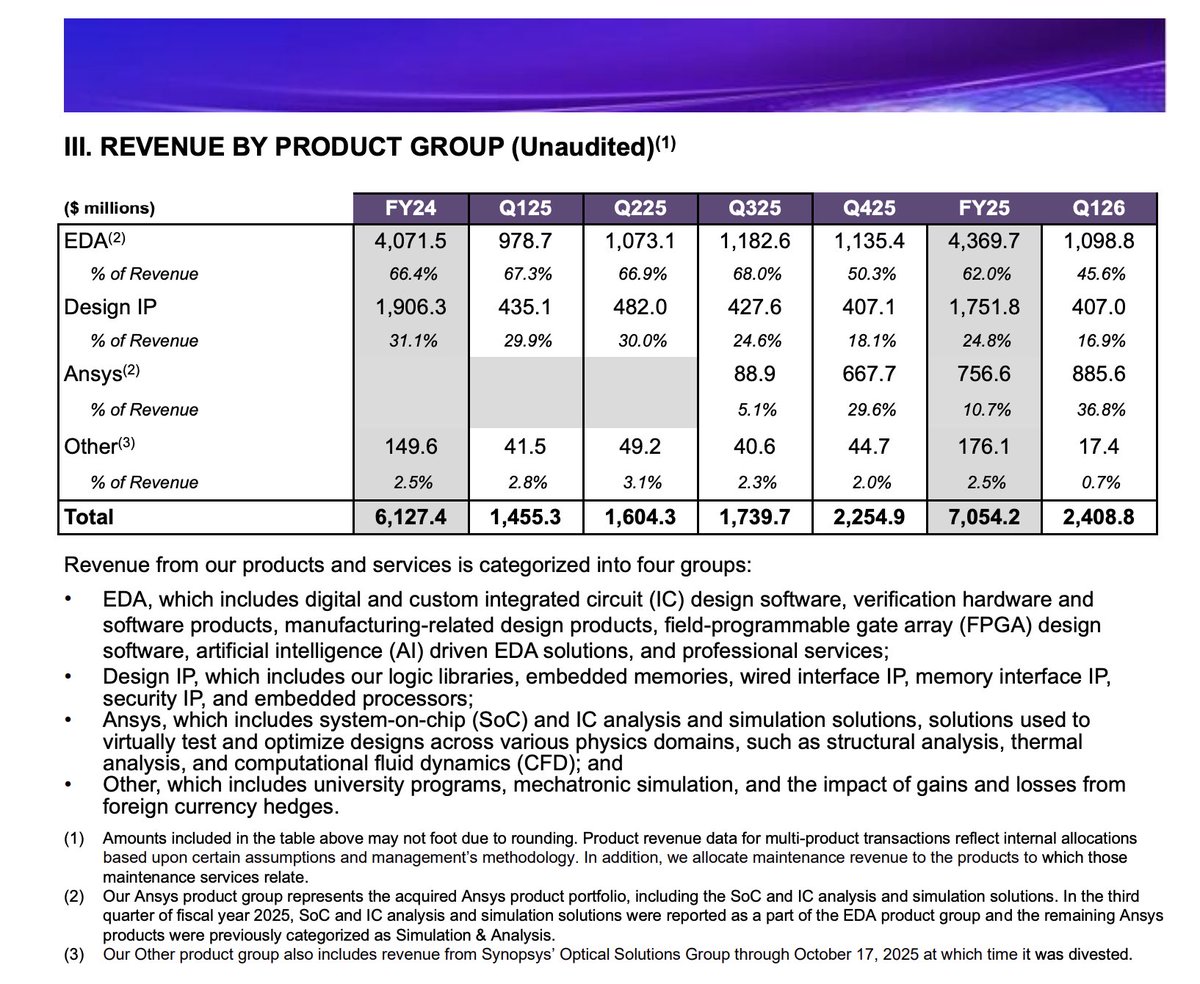

Synopsys $SNPS Q1 2026 Report 🗓️

✅ REV: $2.41B (+65% YoY)

✅ EPS: $3.77 (+24% YoY)

💵 Board of Directors approved a replenishment of the company’s existing stock repurchase program with authorization to purchase up to $2B of stock

English

Moody’s $MCO Q3 2025 Report 🗓️

✅ REV: $2.01B (+11% YoY)

✅ EPS: $3.92 (+22% YoY)

Dimitry Nakhla | Babylon Capital®@DimitryNakhla

7. Moody’s $MCO (Wed AM) 🗓️ REV Est: $1.95B (+7%) 🗓️ EPS Est: $3.68 (+15%) 💵 NTM P/E: 31x 💵 NTM FCF Yield: 3.25% $MCO analytics segment has been its primary growth engine over the past decade

English

@realroseceline A company which can compound at 12-15% over the long run, with a management that’s incredibly modest, adaptable and pensive should never be sold

English

$COST is an incredible business with a strong moat and great economics, but at the end of the day, it’s just a business. It’s not changing the world or curing cancer. It will keep compounding steadily, but if I ask myself whether I’d buy the whole thing at 50x earnings, the answer is no.

English

At 22x, $ZTS is at the low end of its decade-long multiple range, raising the question:

How much further can its multiple compress?

My view: most of the compression is likely behind us, with potential for multiple expansion driven by upward guidance and positive revisions 📈

Dimitry Nakhla | Babylon Capital®@DimitryNakhla

A quality valuation analysis on $ZTS 🧘🏽♂️ •NTM P/E Ratio: 22.52x •10-Year Mean: 30.85x •NTM FCF Yield: 4.02% •10-Year Mean: 3.24% As you can see, $ZTS appears to be trading below fair value Going forward, investors can receive ~37% MORE in earnings per share & ~24% MORE in FCF per share 🧠*** Before we get into valuation, let’s take a look at why $ZTS is a great business BALANCE SHEET✅ •Cash & Short-Term Inv: $1.74B •Long-Term Debt: $5.23B $ZTS has a strong balance sheet, a BBB+ S&P Credit Rating & 13x FFO Interest Coverage RETURN ON CAPITAL✅ •2020: 19.9% •2021: 24.1% •2022: 23.1% •2023: 25.7% •2024: 28.8% •LTM: 30.8% RETURN ON EQUITY✅ •2020: 50.5% •2021: 48.9% •2022: 47.2% •2023: 49.8% •2024: 51.1% $ZTS has strong return metrics, highlighting the financial efficiency of the business REVENUES🆗 •2014: $4.79B •2024: $9.26B •CAGR: 6.81% FREE CASH FLOW✅ •2014: $0.45B •2024: $2.30B •CAGR: 17.72% NORMALIZED EPS✅ •2014: $1.57 •2024: $5.92 •CAGR: 14.19% *you’ll notice stronger CAGR in FCF & EPS mainly due to margin expansion, which should continue (e.g. net income margins — from 2014 to 2024 — grew from 12.2% to 26.9%, respectively) SHARE BUYBACKS✅ •2014 Shares Outstanding: 502.03M •LTM Shares Outstanding: 449.50M By reducing its shares outstanding ~10.5%, $ZTS increased its EPS by ~11.7% (assuming 0 growth) MARGINS✅ •LTM Gross Margins: 71.5% •LTM Operating Margins: 37.5% •LTM Net Income Margins: 27.8% ***NOW TO VALUATION 🧠 As stated above, investors can expect to receive ~37% MORE in EPS & ~24% MORE in FCF per share Using Benjamin Graham’s 2G rule of thumb, $ZTS has to grow earnings at an 11.26% CAGR over the next several years to justify its valuation Today, analysts anticipate 2025 - 2026 EPS growth over the next few years to be less than the (11.26%) required growth rate: 2025E: $6.32 (7% YoY) *FY Dec 2026E: $6.85 (9% YoY) 2027E: $7.53 (10% YoY) 2028E: $8.30 (10% YoY) $ZTS has an excellent track record of meeting analyst estimates ~2 years out, so let’s assume $ZTS ends 2028 with $8.30 in EPS & see its CAGR potential assuming different multiples 30x P/E: $249.30💵 … ~18.3% CAGR 28x P/E: $232.68💵 … ~16.0% CAGR 26x P/E: $216.06💵 … ~13.5% CAGR 24x P/E: $199.44💵 … ~10.9% CAGR 22x P/E: $182.82💵 … ~8.2% CAGR As you can see, $ZTS appears to have attractive return potential IF we assume >24x earnings (a multiple below its 10-year mean & more importantly, a multiple justified by its sustainable moat & exemplary capital allocation) Today at $146💵 $ZTS appears to be an attractive consideration for investment with a decent margin of safety A modest upward revision in growth estimates could drive meaningful multiple expansion for $ZTS — As shown in the P/E chart, its valuation is nearing a fundamental bottom, suggesting a higher likelihood of multiple expansion than further compression #stocks #investing ___ 𝐃𝐈𝐒𝐂𝐋𝐎𝐒𝐔𝐑𝐄‼️: 𝐓𝐡𝐢𝐬 𝐢𝐬 𝐍𝐎𝐓 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐀𝐝𝐯𝐢𝐜𝐞. 𝐁𝐚𝐛𝐲𝐥𝐨𝐧 𝐂𝐚𝐩𝐢𝐭𝐚𝐥® 𝐚𝐧𝐝 𝐢𝐭𝐬 𝐫𝐞𝐩𝐫𝐞𝐬𝐞𝐧𝐭𝐚𝐭𝐢𝐯𝐞𝐬 𝐦𝐚𝐲 𝐡𝐚𝐯𝐞 𝐩𝐨𝐬𝐢𝐭𝐢𝐨𝐧𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐬𝐞𝐜𝐮𝐫𝐢𝐭𝐢𝐞𝐬 𝐝𝐢𝐬𝐜𝐮𝐬𝐬𝐞𝐝 𝐢𝐧 𝐭𝐡𝐢𝐬 𝐭𝐰𝐞𝐞𝐭. 𝐓𝐡𝐞 𝐢𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐜𝐨𝐧𝐭𝐚𝐢𝐧𝐞𝐝 𝐢𝐧 𝐭𝐡𝐢𝐬 𝐭𝐰𝐞𝐞𝐭 𝐢𝐬 𝐢𝐧𝐭𝐞𝐧𝐝𝐞𝐝 𝐟𝐨𝐫 𝐢𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐩𝐮𝐫𝐩𝐨𝐬𝐞𝐬 𝐨𝐧𝐥𝐲 𝐚𝐧𝐝 𝐬𝐡𝐨𝐮𝐥𝐝 𝐧𝐨𝐭 𝐛𝐞 𝐜𝐨𝐧𝐬𝐭𝐫𝐮𝐞𝐝 𝐚𝐬 𝐢𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐚𝐝𝐯𝐢𝐜𝐞 𝐭𝐨 𝐦𝐞𝐞𝐭 𝐭𝐡𝐞 𝐬𝐩𝐞𝐜𝐢𝐟𝐢𝐜 𝐧𝐞𝐞𝐝𝐬 𝐨𝐟 𝐚𝐧𝐲 𝐢𝐧𝐝𝐢𝐯𝐢𝐝𝐮𝐚𝐥 𝐨𝐫 𝐬𝐢𝐭𝐮𝐚𝐭𝐢𝐨𝐧. 𝐏𝐚𝐬𝐭 𝐩𝐞𝐫𝐟𝐨𝐫𝐦𝐚𝐧𝐜𝐞 𝐢𝐬 𝐧𝐨 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞 𝐨𝐟 𝐟𝐮𝐭𝐮𝐫𝐞 𝐫𝐞𝐬𝐮𝐥𝐭𝐬. 𝐈𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐜𝐨𝐧𝐭𝐚𝐢𝐧𝐞𝐝 𝐢𝐧 𝐭𝐡𝐢𝐬 𝐭𝐰𝐞𝐞𝐭 𝐡𝐚𝐬 𝐛𝐞𝐞𝐧 𝐨𝐛𝐭𝐚𝐢𝐧𝐞𝐝 𝐟𝐫𝐨𝐦 𝐬𝐨𝐮𝐫𝐜𝐞𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞𝐝 𝐭𝐨 𝐛𝐞 𝐫𝐞𝐥𝐢𝐚𝐛𝐥𝐞, 𝐛𝐮𝐭 𝐢𝐬 𝐧𝐨𝐭 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞𝐝 𝐚𝐬 𝐭𝐨 𝐜𝐨𝐦𝐩𝐥𝐞𝐭𝐞𝐧𝐞𝐬𝐬 𝐨𝐫 𝐚𝐜𝐜𝐮𝐫𝐚𝐜𝐲.

English