English

Dev

583 posts

Weak results from #kceil anticipated as iran war has caused damage for a lot of companies.

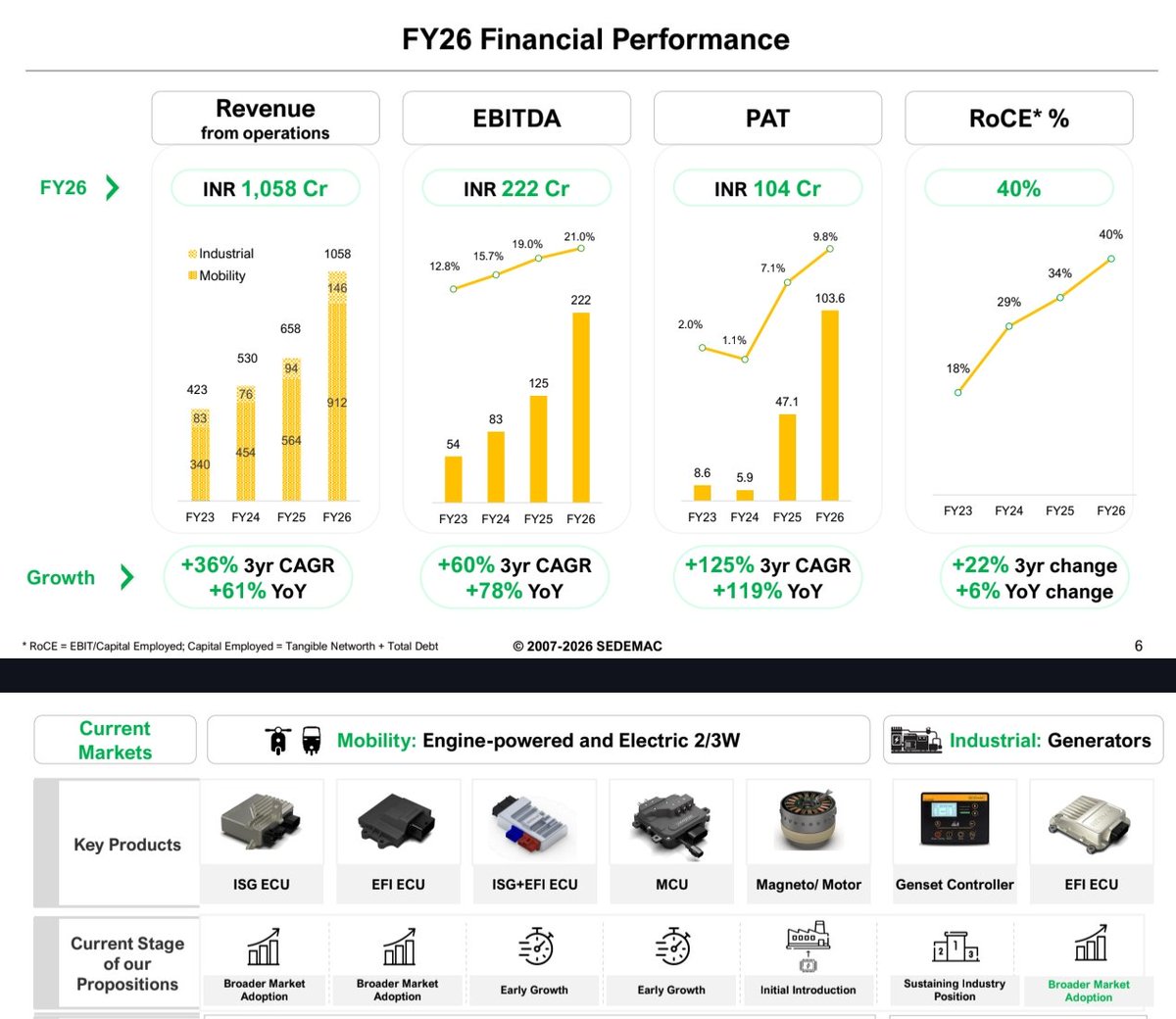

#SME #KCEIL #KayCeeEnergy Kay Cee Energy & Infra H2FY26 Earnings Call Highlights 👉 FY27 & Future Outlook ▫️ Better revenue growth expected in FY27 – significantly higher than FY26 💠H2 FY26 impacted by ~₹50-60 Cr delayed supplies due to geopolitical tensions/war-related disruptions in Middle East 👉Management also confirmed repeat orders continue from RVPNL despite past allegations (no departmental action taken; cancelled tenders re-floated for all players including Universal & Rajesh Power Services) 👉Delayed material has already started reaching India (50% executed in May) and the balance will be executed in the next 2-3 months. 💠 H2 FY26 revenue was deliberately protected at the cost of top-line (81 Cr vs 114 Cr in H2 FY25) to safeguard margins; full impact of the deferred material (supply + service portion) will flow into FY27 💠 No specific numerical guidance given to avoid investor fixation irrespective of market realities ▫️ EBITDA margins to be maintained at 10-12% 💠 Emphasised priority on margin protection over aggressive revenue push. They rejected the option of chasing top-line at the cost of 30-40% EBITDA shrinkage by sourcing expensive local material 👉 Backward integration (new manufacturing unit for hardware, CP/CVT, transformers) expected to add ~1-2% margin initially (captive use first, later sales to others) 💠Helps reduce supply-chain disruptions (currently 5-7% of raw material is imported. Unit expected to start commercial production by September-December 2026 👉 Current Order Book / Projects and Future Pipeline ▫️ Unexecuted Order Book: ₹481 Cr (as on 31 March 2026). 💠 Execution timeline: 12-18 months (majority in next 12-13 months). 💠 Out of 481 Cr, ~₹350 Cr was earlier in JV (now largely completed); current book is almost entirely standalone KC Energy orders. 💠 Majority with RVPNL (Rajasthan) + private players (~₹73 Cr). Fixed-price contracts are minimal (only small 4-5 Cr orders); most have price-variation clauses. ▫️ Bid Pipeline: ~₹300 Cr+ tenders already quoted; expected to finalise in next 1-2 months. 💠 Diversification efforts underway – bidding in Assam, Bihar, and other states to reduce Rajasthan concentration ▫️ No major funding constraint once retention money is released. 👉 Other Notable Points ▫️ Working Capital & Liquidity • Other current assets rose (₹102 Cr → ₹160 Cr) due to SD/EMD/retention deductions as per tender terms. • ₹50-60 Cr retention money expected to be released in next 2-3 months (55-60% of total locked amount) → will improve cash flow and reduce borrowing needs. • Bank facilities adequate (fund-based ~₹50-65 Cr utilised ~₹40-45 Cr; non-fund ~₹100 Cr). No funding issue for executing current order book or bidding aggressively. • Debt levels stable 👉Key Challenges & Management Stance 💠Revenue shortfall in H2 FY26 entirely attributed to ERS supply delays (not demand or execution failure). 💠 Rajasthan tender delays/cancellations (common across industry) due to government processes/land/ROW issues – not company-specific. 💠Competitive intensity exists but margins protected through selective bidding (only tenders with decent gross margins). 💠New manufacturing unit in Kota near completion (sheds/flooring done; machinery installation starting shortly). ▫️ Strategic Focus 💠Relationships with key clients (RVPNL, PowerGrid, private players like Wonder Cement – no BG required in private) 💠ERS (Emergency Restoration System) – alternative Indian steel options exist but aluminium preferred for faster installation; no major requirement expected in next 5 years

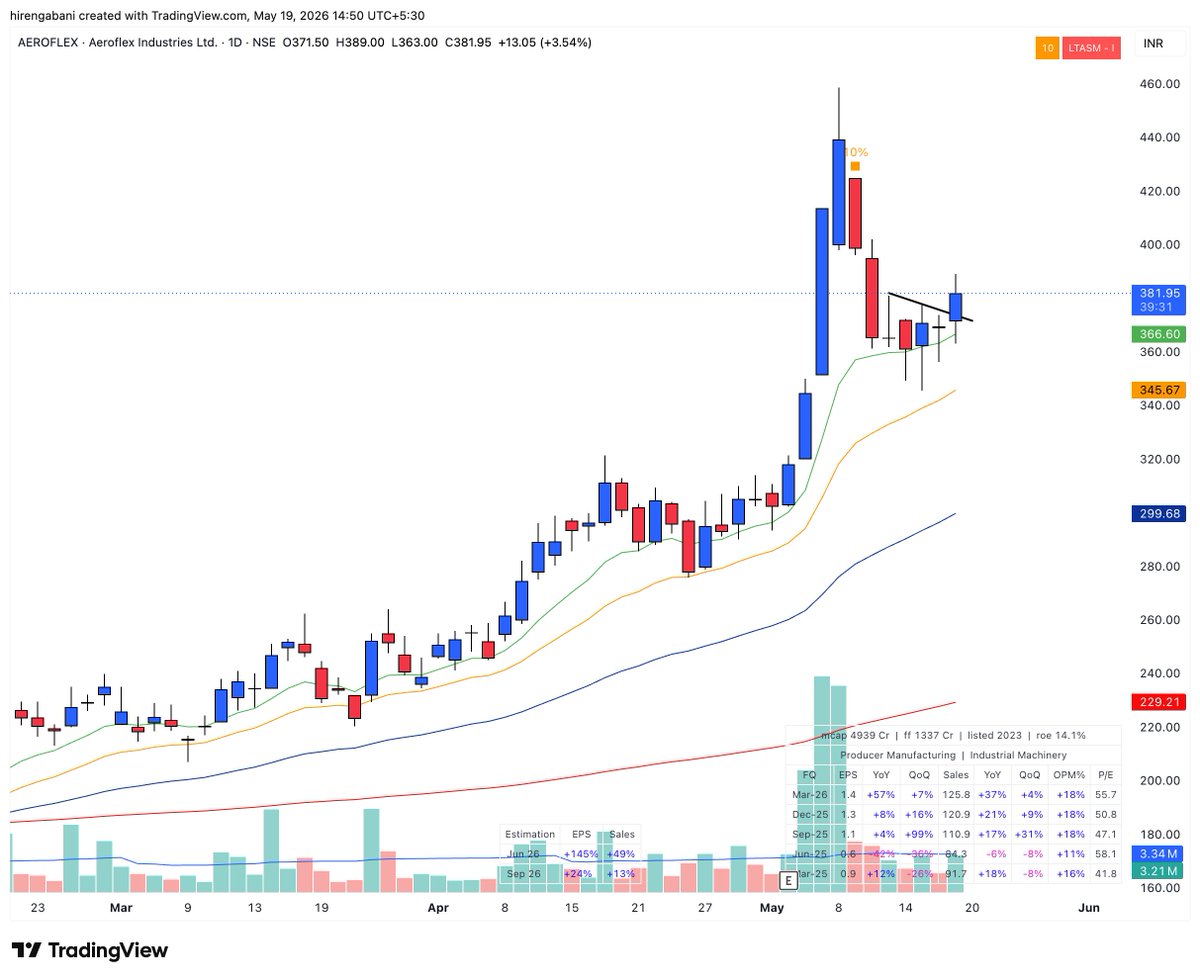

Have you seen a stock which has kept going up after a QIP in the next 2-3 months ? Can you share some examples please..Thanks Examples of pullbacks: 1.Yatharth 2.Anantraj 3.KCEIL 4.Phantom 5.Vintage coffee n many more Looking for examples of rally post QIP

What do you think KCEIL’s results will look like? 🤔📊 Will the numbers surprise on the upside? 👀 #KCEIL #Results #StockMarketIndia #SMEStocks