@KobeissiLetter Soon Global Market will see ATH but Yield Bullrun will start after this correction .

People are slowly ignoring Yield but will come in talk soon after all Market Hit ATH .

@WatcherGuru Soon we will see ATH in Global Markets and Bond will make Top soon for some time .

Small correction is already completed in global Markets.

BREAKING: The final draft of the US-Iran agreement has been reached with the mediation of Pakistan, which is expected to be announced within the next few hours, per Iranian State media.

BREAKING: Newly released Fed meeting minutes show that the "majority" of officials thought rate hikes may be needed if inflation persists.

In a sudden turn of events, it appears that the market and the Fed are bracing for potential rate hikes.

IT Sector are FALLING.

Metal Sector are FALLING.

Sensex Sector are FALLING.

Nifty 50 Sector are FALLING.

FMCG Sector are FALLING.

Financial Sector are FALLING.

Realty Sector are FALLING.

If every sector is falling…

Then where is the money going? 👀

The IT Sector is not a Contra Bet Investing.

Avoid investing in this theme. I am not expecting any bull run in the next 2-3 years.

Every Rise can ve eventually sell out.

Every Market phase, leading sectors are different:

1) 1997 to 2000 - IT sector

2) 2003 to 2007 - Reality and power

3) 2009 to 2014 - Pharma

4) 2015 to 2018 - Financials

5) 2018 to 2021 - Chemical and IT

6) 2021 to 2025 - PSUs/ EV / Power

7) 2026 onwards - _________?

I have zero tolerance for regurgitated drivel passed off as wisdom. ( But it works well in India though). So I yesterday came across somebody from US saying foreign investors don't like India because it does not have AI.

Somebody else from Singapore wrote that taxation has caused FIIs to flee India.

Both are nonsense.

Let's keep it short:

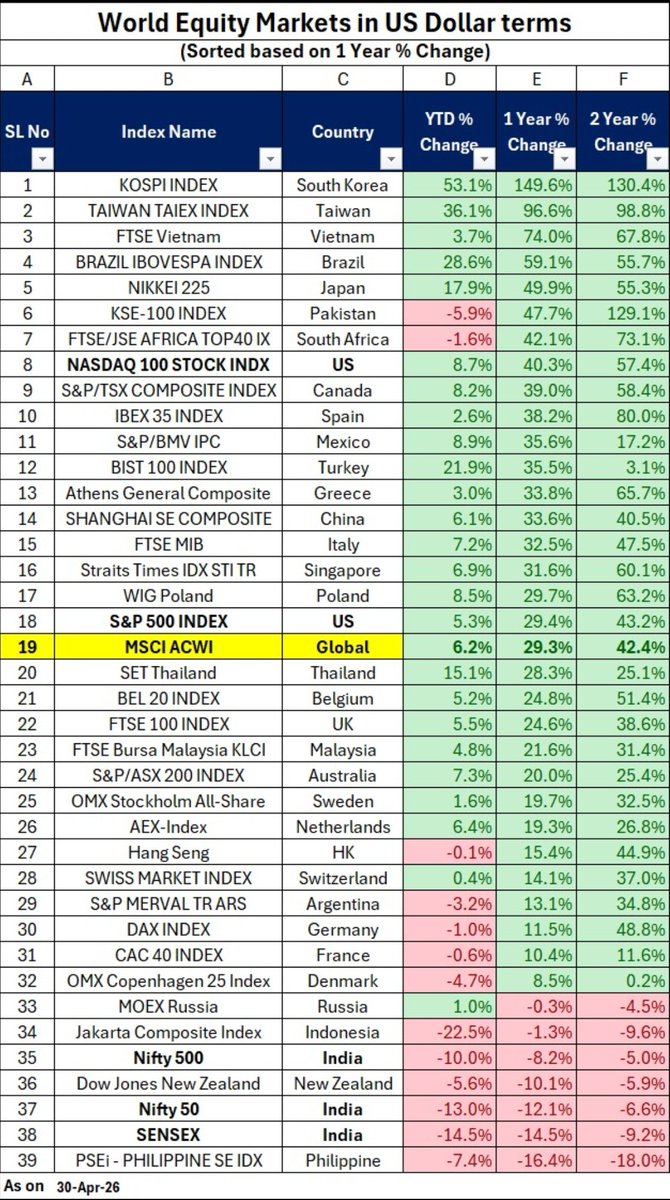

See image 1. Market performance. How many markets in that do you see " have AI"? US, the cradle, ranks at 18. NDX at 8. What AI does Brazil have? Vietnam? SAF? Spain? Greece? Turkey? Italy? Pakistan?

And look at their performance. Better than the US.

Folks just dish out tripe, that's considered Socratic sense in a market population today that has rid itself of all nuanced thought.

India doesn't have tech, AI or whatever else. But it NEVER had tech. Yet, markets did well for a couple of decades. How so? Domestic economy, right? But that's supposedly doing very well, based on GST , 8% growth,etc. Yet why is India at the bottom? Now that's coming up in my next article.

So FIIs never bought India because of tech. Their exit has nothing to do with tech either ( look at how well non tech markets have done as in the image).

I just detest such under- analysed paan dukaan level trash. Even if it comes from US or Singapore.

Views should be data driven. Not based on false positives, which itself is based on recency bias.

I have given you the data. Chew over it.

FIIs selling because of taxes is another bs. See Image 2. They have bought, they have sold, through CG taxes. markets have gone up and down irrespective ( negligible correlation as I have said many times). Yet, laments are written in pink papers by fund managers. Real Reasons are deeper. But some other time...

We have become a seriously low IQ market if we stop applying even basic test of data to peddled codswallop.

Why CPUs are the next bottleneck?

Demand for CPUs from AMD, Arm and Intel is spiking mainly because AI workloads are shifting from “GPU-only training” to AI agents and inference at scale that lean heavily on CPUs, creating a structural shortage and new pricing power.

Core reasons demand is exploding

AI data center build‑out: Cloud providers and enterprises are in an AI arms race, pouring billions into new data centers, which need racks of server CPUs alongside GPUs and custom accelerators. These AI-driven data centers are “swallowing” enormous numbers of high‑performance CPUs from AMD and Intel, and driving licensing demand for Arm’s architectures.

From training (GPU) to inference (CPU-heavy): Training large models is GPU‑dominated, but running them in production (inference), orchestrating requests, and managing memory and networking is far more CPU‑intensive. Intel’s recent earnings explicitly highlighted customers moving away from GPU‑only configurations toward setups where CPUs play a much larger role in AI inference and “agentic” systems.

Agentic AI and RAG need lots of “brains around the GPUs”: New “agentic” AI systems, where multiple AI agents coordinate tasks, plus retrieval‑augmented generation (RAG) pipelines, involve heavy scheduling, I/O, database calls and orchestration logic—all CPU‑bound activities. Analysts argue that these workloads can multiply CPU demand several‑fold because every GPU cluster needs a much fatter layer of host CPUs to avoid bottlenecks.

Why this hits AMD, Arm and Intel specifically

AMD (EPYC, x86 servers): AMD’s EPYC data center CPUs are direct beneficiaries of the surge in AI‑oriented server demand, with record data‑center revenue growth (over 30% YoY in late 2025) tied to AI and cloud build‑outs. As customers expand CPU footprints for AI inference and agents, analysts see a path for AMD to keep taking server share from Intel over time.

Intel (Xeon, data center CPU “comeback”): Intel just reported a sharp rebound in data center and AI CPU revenue (22% YoY), surprising the market and showing strong demand even amid supply constraints. Commentary from management emphasized that AI is moving “from foundational models to inference to agentic,” which requires more CPUs per GPU than older architectures, helping drive a “CPU renaissance.”

Arm (architectures for efficient CPUs): Arm does not sell CPUs directly in the same way, but licenses power‑efficient architectures used by hyperscalers (e.g., custom data center chips) and edge devices. As AI inference and agentic workloads move to energy‑sensitive environments (cloud, mobile, edge), Arm’s efficient designs become more valuable, boosting its licensing and royalty outlook, which investors are pricing into the stock.

Structural shortage and pricing power

Real CPU shortage: Reports now describe a genuine CPU crunch: demand from AI workloads and server refresh cycles is so strong that even lower‑tier Intel chips (“scrap” or downgraded dies) are selling at full price, which is unusual in normal cycles. PC and server OEMs like HP and Dell are already seeing a clear mismatch between CPU supply and demand, with rising costs and stretched lead times.

Price hikes and margin expansion: Intel and AMD have both moved to raise CPU prices roughly 10–15% in early 2026 for server and consumer products, something they can do only because demand is outstripping supply. This pricing power is a big part of why their stocks are reacting so strongly: higher ASPs plus strong volumes boost revenue and margins simultaneously.