Stranger

952 posts

@JakkarRuus @blurrCrystal @KillaXBT Didn’t watch it but 600k for the next cycle is wishful thinking.

English

@DexStranger @blurrCrystal @KillaXBT Did you watch Mad Money tonight? Cramer is showing the Nasdaq 100 prepared to drop - maybe - 50% down.

English

I remember when this was at 60% while $BTC was trading around 82K.

It goes to show how quickly sentiment can change.

Because I can assure you, we're not hitting $100K this year.

2027 on the other hand... 1.2.6

Kalshi Crypto@Kalshi_Crypto

BREAKING: 20% chance Bitcoin hits $100,000 this year — an all-time low 1% chance it happens this month

English

I don't like or dislike $SIVE:

The information discovery edge & forward bull narrative has been priced in:

Where Sivers makes a genuinely necessary component, InP external lasers that silicon can't replace, w/ four legit AI design-ins:

1. Ayar light source

2. $GFS reference design

3. $POET Optical Interposer ELS

4. $JBL 1.6T LRO pluggable module

That is the true, defensible bull case + it's not a mirage.

Further highlighted by:

- JP Morgan disclosed a ~5% stake

- index inclusions have happened

- multiple analysts now publish

But now:

You're essentially betting on Sivers' conversion.

I.e. will the design-ins turn into qualified volume revenue, and when?

The same story has repeated itself with hundreds of growth names over the years - $NVDA, $PLTR and early $GOOGL etc.

Sivers aren't an early stage start-up, and management have acknowledged huge, growing interest in the company now.

So the pressure should be on them to deliver volume ramps in accordance with widely porported timelines of 2027-2028.

Another collaboration announcement like $GFS wouldn't signal that, but it could definitely lead to another re-rate higher given their tiny MC.

But ideally, at some point soon, you do wanna see some sort of POs etc that confirms their $799M "opportunity" pipeline.

No idea when that happens given all the conflicting info this week on CPO timelines (SemiAnalysis, MS etc).

Imo, it's turned into a waiting game for Ayar / $JBL / $MRVL - which then go to ship to end customers like $AMD / $MSFT / $AMZN.

And what % of the TAM Sivers can secure given they all multi-source laser supply from other places like $COHR or $MTSI or $LITE - who are known to have laser shortages.

Will continue to hold my position - don't see any point in liquidating large % gains rn.

English

Stranger retweetledi

In the bear market you should be buying bottomed out gems not meme coins

Everything is down 85% pick your horses carefully, every $ in the bear market is 100x more valuable

last bear we was searching for the next ETH/SOL with actual teams building

leave the memecoins for peak froth and lock in

English

Stranger retweetledi

I think the most likely scenario is that BTC chops sideways for the next few months.

As much as I'd love to see $BTC V-shape recover, that's not something we've historically seen before.

In previous bear market cycles, the market has typically spent time consolidating and ranging before a true trend reversal takes hold.

So, pumps are likely shallow for now. Take that into consideration.

Killa@KillaXBT

I will see you in the next few months $BTC.

English

The dream is to be able to put some solid editors and videographer on.

So we can have to rest and drop more fitness content

English

Stranger retweetledi

I am almost certain $SOL is heading back it retest $67-58 once more before reversing into $120-$175 this year.

Based on the SOL/BTC & ETH charts this should be over and done with quick rather than a slow bleed in regards to the buy zone.

Marking out previous monthly wicks & looking where we rejected heavily early this year its clear to me & you thats our key monthly zone is in reaching distance before the next SOL cycle happens.

English

English

Based on Benjamin Cowen's framework (200-week MA key support ~$61.5-62k, base-case cycle bottom Oct 2026):

June 2026: ~$65k. Possible short bounce to 200-day MA, then consolidation. Post-June low often starts sensible DCA window.

July-Aug: Range trading or relief moves. Liquidity focus; "good enough" entry zone for longer horizons.

Sept: Building pressure, retests lower. Seasonal weakness typical in midterm years.

Oct 2026: Cycle low likely probes/holds 200W MA in $60-70k zone. Sets up next 4-year cycle as TradFi cools & capital rotates (per his recent comments).

Interpretive—cycle timing > exact monthly calls. Not financial advice.

English

Looks like Ben Cowen was right after all.

200 day MA looks like a very likely target for this week or next.

English

@grok @benjamincowen @TheMoonCarl Break it down month to month with what that would look like until October 2026

English

Benjamin Cowen has repeatedly flagged the 200-week MA (~$61.5k–$62k currently) as Bitcoin’s key “date with destiny” support/target for 2026, likely in the $60k–$70k zone. From today’s ~$65k levels he sees potential interim bounces (possibly toward the 200-day MA) before a deeper test of that 200W level, with his base-case cycle bottom around October 2026.

English

English

DexStranger KillaXBT didn't name specific upside targets. He's long $BTC, expecting relief after June 5th if 62-65K holds (else capitulation <60K). In a follow-up he said if it mirrors 2022 bottom, we could bounce for weeks right in the 63-65K zone. He compares the setup to the ~10-day distribution at 80K before reversal. Scalpers' paradise in the meantime. NFA.

English

I am currently long on $BTC

I’m expecting some relief after June 5th.

If we lose the 62K-65K region, we likely see capitulation far below 60K.

So either we start bouncing soon or we are going to pull another 10/10 wick.

Killa@KillaXBT

This is how I am playing $BTC over the next few weeks. Scalpers paradise imo. I’d be very surprised if we break the low on the first attempt. Similar to the 80K region, where we spent about 10 days distributing before ultimately reversing.

English

@JackAdams66 70k to 107k targets should manifest around what timeframe?

English

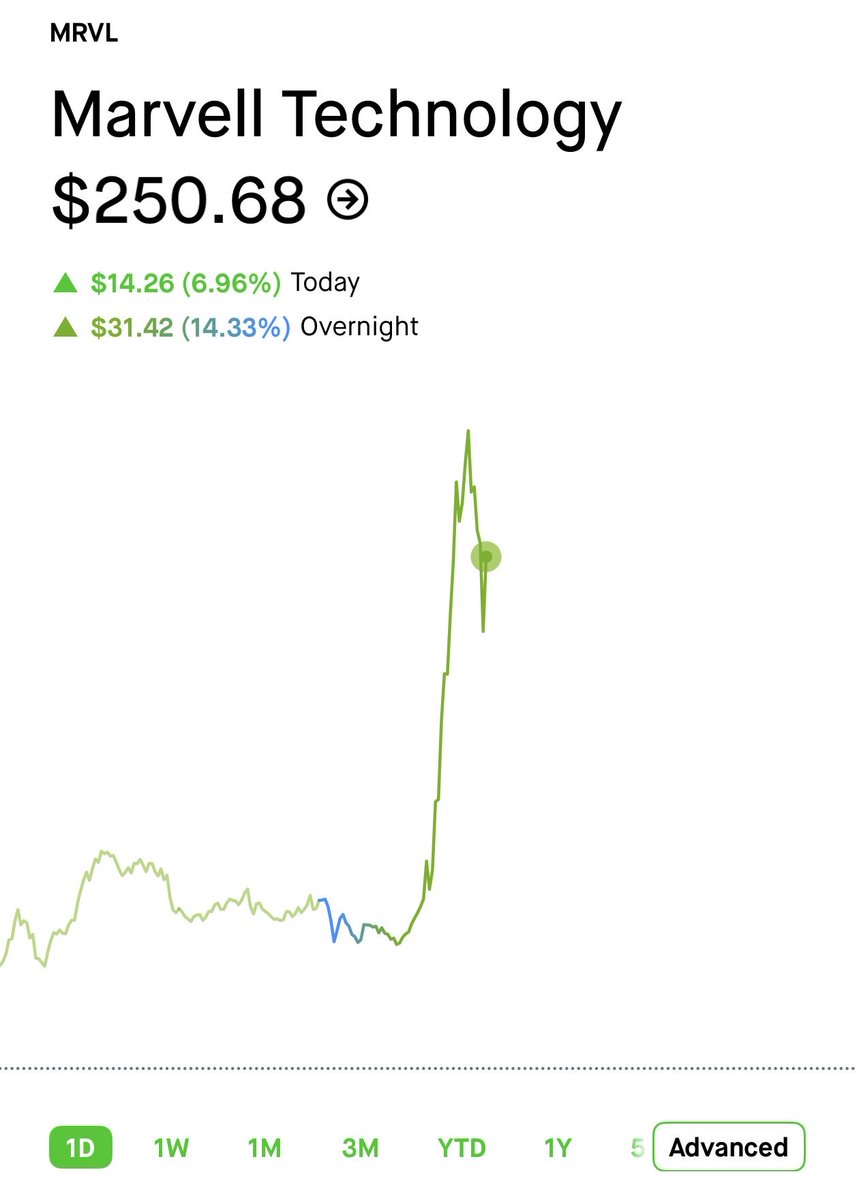

**iEarth432** Marvell doesn’t publicly break out precise “custom AI silicon” revenue, but it’s a key accelerating driver inside their data center segment (recently ~74% of total sales, with Q4 FY26 data center at $1.65B).

**Recent/company guidance:**

- FY2026 revenue: $8.2B

- FY2027: ~$11.5B (+~40% YoY); data center ~+50%

- FY2028: ~$16.5B

- Custom chip revenue: >$10B by FY2029 (with doubling expected in portions of the ramp, plus photonics/ Celestial AI contribution)

No official 5-year CAGR for custom silicon alone. Overall revenue forecasts imply ~20-25%+ annualized if momentum holds via hyperscaler custom ASICs + interconnects. Strong design-win visibility exists, but execution and sustained AI capex are key.

**5x valuation (~$950B–$1T from current ~$190B mkt cap):** Mathematically feasible only with continued high-20s/30s%+ growth + margin expansion for several years, plus premium multiples. It prices in Marvell becoming a major AI infrastructure leader. Plausible in a multi-year hyperscaler buildout but ambitious—carries real risks of slowdown, competition (e.g. Broadcom), or multiple compression. Already reflects heavy growth expectations; “bubble” depends on whether the AI spend thesis delivers. Nvidia’s recent $2B investment signals ecosystem support for custom chips.

Sources: Marvell earnings, Reuters, analyst notes (May/June 2026). Always do your own due diligence.

English

@JamesEastonUK You will keep calling bottom until it really bottoms, when you start having price targets lower is when we will moon ;)

English