Doublea759

14 posts

COMPUTER USE IS GA.

I’ve been using it for months.

If you haven’t found a use case yet, you’re looking in the wrong place.

Start with the ugly work:

- authenticated sites

- on-prem apps via VM

- legacy screens with no API

- portals nobody wants to rebuild

- repetitive data entry

That’s the battlefield.

English

@Mr_Neutral_Man @atelicinvest Got it, thank you!

Btw, I agree with your posts 100% and believe the large public apartment REITS are a no brainer. Might not be home runs but very limited downside. doubled my investment last wk.

Would love mgmt to get more aggressive with property sales / stock buybacks.

English

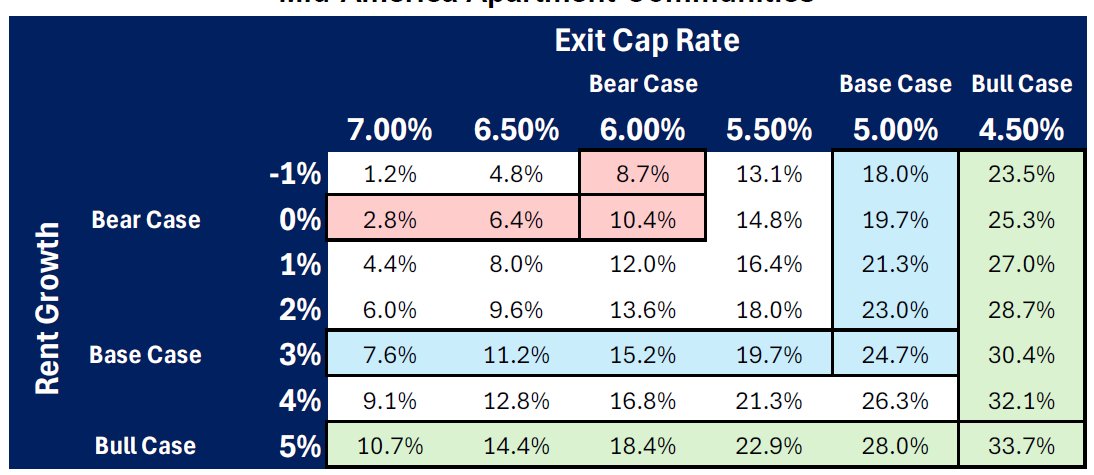

It should say NOI rather than rent

We’re really getting into the weeds

But obviously there is cashflow retained and dividends received

These are around 60% EBITDA margins (noi less sg&a) REITs, not quite 1 for 1

On the run, but 3% exp increase is probably 1.2% NOI decline. Could ge wrong with my math.

English

Arguing with strangers on Twitter that you can allocate $100 to $1,000,000,000 to real estate by buying publicly traded REITs

Better valuation, transparency, liquidity, 1 bps transaction cost, better asset quality. Can put $100mm to work in 5 trading days.

Willing to die on this hill until est IRR drop to 8-10%

Weiss Advice@YonahWeiss

Poorly explain what you do for a living. Go.

English

@Mr_Neutral_Man @atelicinvest I love all your posts. Having trouble understanding this one. Entry and exit at a 6.5, how do you have 6.4 irr at 0% rent growth? Assuming 50% NOI margins and 3% expense growth, that’s 3% NOI decrease per year. Debt is accretive, but at such low LTV would est. lower IRR?

English

Sensitivity analysis - You'll need cap rate to expand to 7.0% and rent to go negative 1% for 3 years in a row for the IRRs to be 1.2%

Overall IRR have come down a bit due to recent price increase, but generally in the right ball park

Again ppl will argue, MF REITs won't trade at 5.0% cap rate and my LPs put their trust in me to make that call

English

@Barchart @AskPerplexity can you adjust this chart for inflation?

English

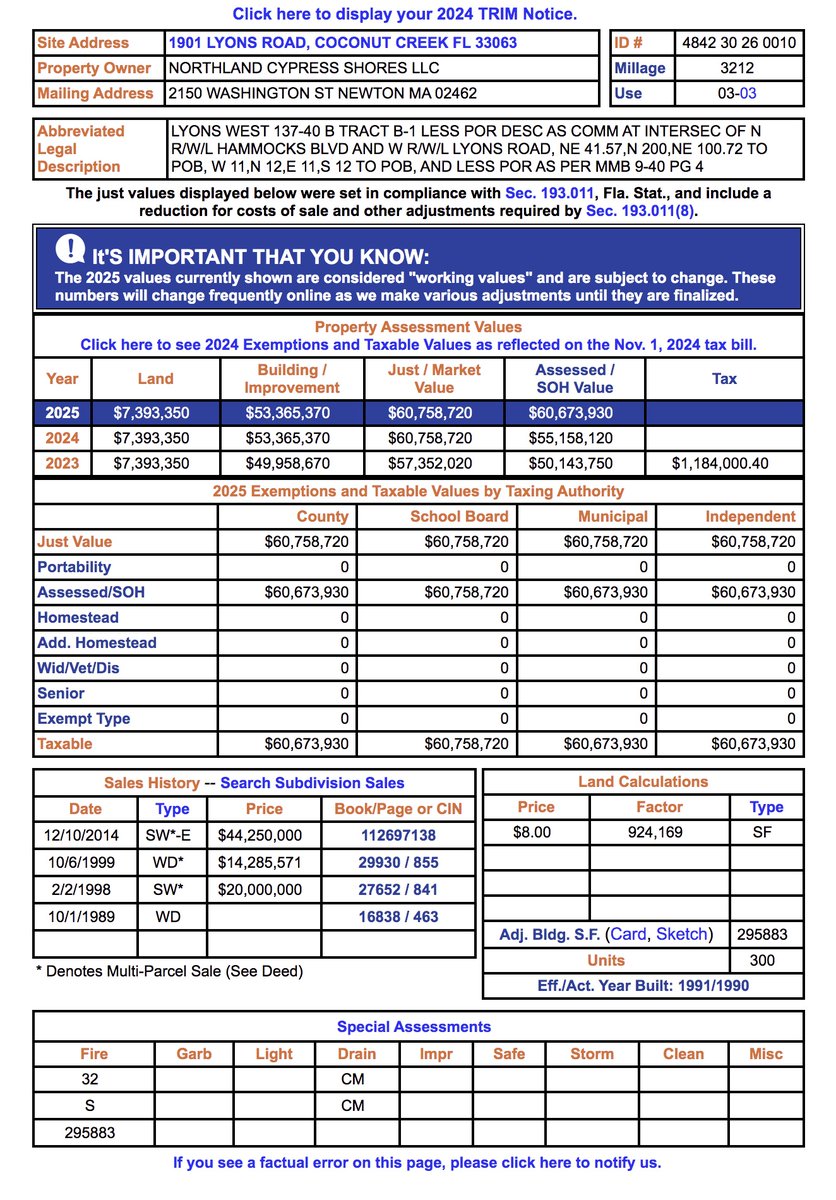

@kristinbjornsen I love all your tweets but not sure I understand this one. Northland is a major PE firm that has owned this asset for ~10 years. CBRE underwrote a 10 year Fannie loan likely at a min 1.25x DSCR based on their historical financials. Seems okay? Probably also I/O so DSCR >1.25x

English

northland investment corp just refinanced a loan for the cypress shores apartment complex in coconut creek. loan was set to mature jan 1 2025. principal amount increased from $35.4M to $54.8M.

and it's now.... a *balloon* mortgage? does fannie know? 🎈🪡

northland.com/portfolio/

English

@alpha_eos @multifamilyman_ Bonds have almost always offered a higher yield than equities dividends. Companies/properties can grow their earnings over time. Bonds cannot.

10yr is probably a better investment than class B/C office, but long-term growth potential exists in many RE asset classes

English

@multifamilyman_ lol.. 10yr at 3.72% - headed to 4%.. investors buying highly illiquid, high risk assets at 4.5%.. good luck with that.

English

Money is pouring back into multifamily.

Equity deployment (funds) mandates now matter.

The clock is ticking.

Demand to acquire is putting pressure on cap rates.

Deals are back in the 4.5% range right now.

There was little deal flow across the country for 1H24, but sellers have taken notice of aggressive pricing and entered the market.

Deal flow has nearly doubled.

English

@ParcFinancial @multifamilyman_ Fannie/freddie lending at 4.5% fixed 5yr or 7yr for 65% LTV and 1.35x DSCR

English

@multifamilyman_ Borrow at 7% into a 4.5% yielding asset ? In what planet does that make sense ?

English

@kurtjordan87 @multifamilyman_ Every public REIT has said deals are trading sub 5% cap on most recent earnings calls

English

@moseskagan This mathematically should not change LP returns, and, in the event the deal doesn’t do well, is better from a tax perspective.

The only way this order changes LP returns is if the pref doesn’t accrue on unpaid capital and unpaid pref (a gotcha in my eyes).

English

My ~favorite operating agreement "gotcha":

Sponsor made order of distributions:

1. Return of capital

2. Payment of pref

3. Split of profits

Result: Amount of pref earned by LPs radically reduced (vs. the standard order, which is: pref, return of capital, split).

English

@sweatystartup Someone in commercial real estate in SF told me the obviously high vacancy rates can’t be corrected by lowering rents because lending terms commonly preclude it.

Is that true and if so isn’t it another reason to expect a sudden collapse at some point?

English

If interest rates stay here for 24 months, there will be a 30-40% price correction on commercial real estate.

In-place 8 cap deals with 40% expense ratio on tertiary storage. 6-7 cap on class A product.

Multi will get crushed. 6-7 cap pricing on class A.

Equity will be totally gone on a lot of deals acquired since 2020.

A lot of forced sales.

Not as bad as 2008, but a lot of variable debt coming due in the next 24 months that owners can’t cover or replace at new rates.

Wild times coming!

English

@Liam_Dougherty @RVParkGuy I have always seen pref compound on capital and unpaid pref, so $7.36 (8% * $92 capital) + $0.36 (8% of $8 unpaid pref) = $8 pref in year 2

English

@Doublea7591 @RVParkGuy The pref return accrued would be $7.36 in the second year (8% of 92).

It becomes clearer using more extreme #'s. I.e $20 pref/distb.

Year 1 get $20 now capital account/units outstanding reduced 20%.

Year 2 pref is $16 (20%x 80).

Vs $20 in other waterfall of pref->RoC

Toronto, Ontario 🇨🇦 English

What say you, savvy deal makers?

I recently had an investor ask me to switch the order of distributions, with the first $ being classed as return of capital rather than the preferred return. They said there’s a tax advantage.

After thinking it over & talking w/ legal & CPA...

English

@RVParkGuy 8% Pref. Buy $100 deal. At end of year 1, you distribute $8. You are left with either $100 of capital and $0 of unpaid pref, or $92 of capital and $8 of pref. Either way, next year’s pref is 8% of $100 (92+8=100)

English

@RVParkGuy They are mathematically identical (assuming standard contract language, i.e. compounding pref). Pref compounds on capital and unpaid pref. Example...

English