Draupnir

27 posts

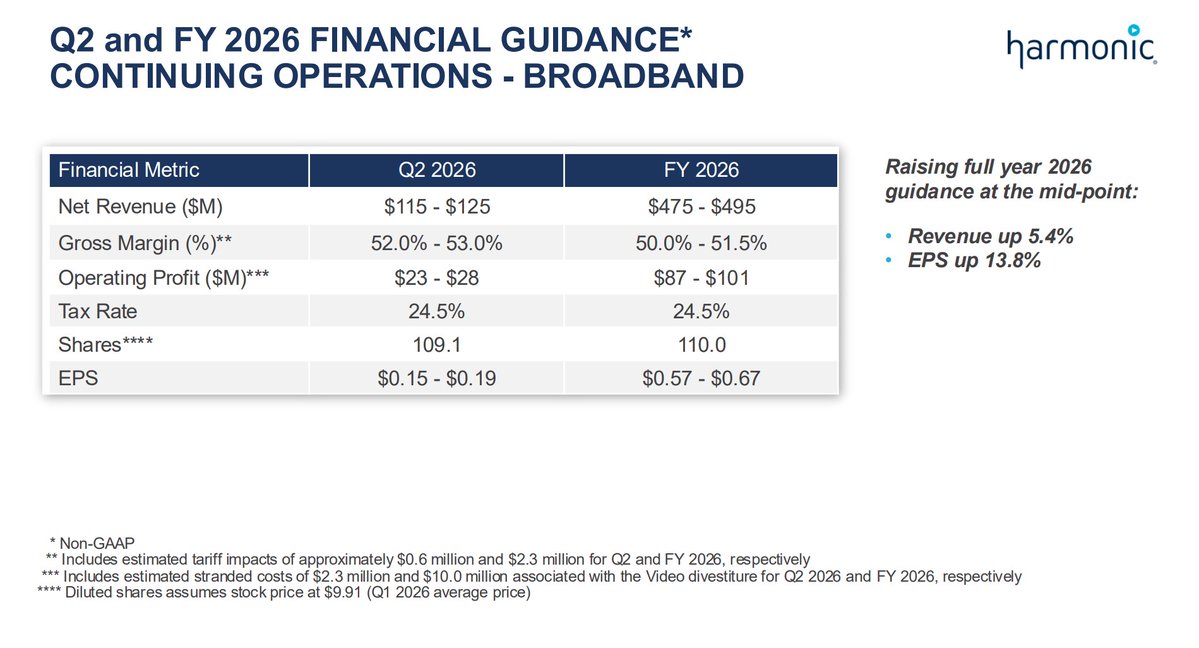

$HLIT (~$1.65B) controls more than 95% of the software that every major US cable company needs to upgrade their network for the AI era. Every time you stream, video call, or ask an AI app a question, that data runs through a cable line owned by Comcast, Charter, or Cox. Upstream traffic is now growing 21.7% a year and the old cable standard cannot keep up. The fix is called DOCSIS 4.0. It takes cable from 1 Gbps to 10 Gbps with much faster upload speeds. Every Tier-1 operator is being forced to upgrade or lose subscribers to fiber. There is only one company that sells the software to run those upgraded networks at scale. HLIT. Comcast, Charter, Cox, and Altice all run its cOS platform. 150 customers and 45.7M cable modems live on it today. Charter alone has committed $5.5B to this upgrade through 2027. Every single node they deploy requires an HLIT license. Q1 revenue grew 43% YoY and beat the top of guidance by 16%. Backlog hit $582M, up 87% YoY and 1.2x full year revenue guidance. The biggest cable upgrade cycle in history is already booked. The chips and the lasers get all the attention. The toll booth between AI demand and your living room is hiding in plain sight. Full deep dive in the comments. $HLIT $CMCSA $CHTR $CALX

NEW TRADE: ALL IN $HLIT. Currently -2% lower than my own entry btw. They make broadband software for companies like Comcast, Charter, etc. I spent 2 hours researching the ticker here on 𝕏 and think it could be a good one. THESIS: Huge pull-forward demand to future-proof for an agentic AI world. Similar to $NOK but for broadband networks. Citrini shouted it out yesterday after hours x.com/citrini/status… which caused the +15% jump Agentic AI usage patterns will look quite different than previous networking demands (mostly one-way like video). So there's a huge push to modernize quickly. Their CableOS software is the easiest way to do it. The company is legit: - 98% market share - Revenue is up 87% YoY, 43% QoQ - 52% gross margins - Guidance raised to $475M - $495M - $43M in stock repurchases - Lots of insider, hedge fund, and robinhood buying - Stock price peaked at $157.50 back in 2000 🤯 They also sold their legacy low growth video business to focus on the high-margin software. Good focus. Catalyst is... price momentum honestly. Similar to $BAND over the last few weeks. Crossing fingers its the start of a multi-day run. I hate chasing. NGL I broke this rule here. Had to listen to my gut. Also worth experimenting with my own rules. Different markets demand different rules and not chasing this year has left me missing several good plays. We'll see how good my gut still is. My doctor says its healthy. --- As a reminder: this is my challenge account where I restarted with $35k to go all-in swing trading 1 stock at a time to $10M again. Now at $61k. As always, please do your own research with your own independent thinking and risk tolerance and decide your own buys and sells. (sorry for the delay, was dealing with a power outage and had to run to a cafe)

Here's a new take on a popular name that I haven't seen touched on AT ALL on X so far. First, some background: $IQE / $IQEPF is a compound semiconductor wafer supplier. £448M market cap. $IQE makes advanced epitaxial wafers. The foundational material that makes semiconductors function at extreme frequencies and precision. Without IQE's wafers, the chips powering modern defense, photonics and AI infrastructure don't exist. Here's what nobody is connecting. $IQE is embedded inside every major U.S. defense prime. Let me emphasize this again. $IQE is a SOLE (not SINGLE) SOURCE vendor to all the Prime Aerospace and Defense companies in the United States. They CANNOT use LandMark as it is a supply chain risk. 🔹 RAYTHEON ($RTX) 15+ year direct partnership. Greensboro NC facility officially qualified for IR photodetector epiwafers powering advanced ISR systems. Multiple Premier Supplier Excellence and EPIC awards. Embedded. Qualified. Awarded. Not transactional. 🔹 BAE SYSTEMS GOLD TIER supplier to BAE Electronic Systems. The highest classification BAE awards. BAE builds defense, aerospace and security technology directly for the U.S. DoD. One of the most demanding qualification processes in defense. IQE passed it at the top level. 🔹 LOCKHEED + NORTHROP IQE's InP and GaAs wafers flow into Lockheed and Northrop platforms via $MACOM and Qorvo - integrated into RF and photonic systems inside the most advanced U.S. defense platforms in existence. Every major U.S. defense prime. One supplier. Indium Phosphide is not a commodity. It's a controlled, high-precision material. There are almost no qualified alternative suppliers at IQE's level. Qualification cycles take years. The moat is structural. The U.S. government knows this. The InP executive order was about defense supply chain security, protecting allied-nation suppliers of critical compound semiconductors. IQE's Welsh and U.S. fabs sit squarely inside that framework. Explicit government policy support for IQE's core business. $MACOM didn't just sign LTAs with IQE. They invested £45M directly - a 10% market cap injection from a company that needs IQE's InP supply to exist. Supply chain insurance dressed as equity. Debt repaid. Capex funded. Capacity redirecting to high-margin photonics. 🔹 $LITE (Lumentum) - flagship customer, LTA locked in. Lumentum is critical to the NVIDIA optical interconnect buildout. NVIDIA's photonics push flows through Lumentum. Lumentum's supply chain flows through IQE. Direct line from IQE wafers to the most important AI infrastructure buildout on the planet. The smart money noticed. 🔹 Point72 - Form 8.3 under UK Takeover Code. Steve Cohen's fund disclosed. 🔹 Artisan Partners — 12.99%. Multi-year conviction. 🔹 Lombard Odier — 200-year-old Swiss private bank. 🔹 T. Rowe Price — long duration institutional money. The Point72 Form 8.3 matters. Filed under Rule 8.3 of the UK Takeover Code — required during offer periods or takeover speculation. Point72 isn't just holding. They're disclosing under takeover rules. Someone knows something. The full picture: → Every major U.S. defense prime. One supplier. → InP executive order protection → $MACOM £45M strategic anchor → $LITE LTA → Point72. Artisan. Lombard Odier. T. Rowe. → £448M market cap This doesn't trade here once the market figures it out. The catalyst is Thursday. $IQE FY2025 results May 28. Defense positioning. MACOM investment. Photonics ramp. All formally presented post-fundraise for the first time. Thursday is the moment. $IQE $RTX $MACOM $LITE $MTSI

This one might be unpopular, but here goes: 🧵 $SIVE has run 1,200% in under a year. Management called the April raise "only 2.5% dilution." Here's why that framing is misleading — and what the filings actually show: 1. The 2.5% figure comes from Sivers' own April 16 press release (MFN.se). What they didn't headline: the denominator already includes ~41M shares of warrants, options and convertibles that don't show up in the basic share count. The 2.5% is technically accurate. The framing is not. 2. Do the math yourself: 8.62M new shares ÷ 2.5% = ~345M fully diluted shares. Basic count post-raise: ~304M. That 41M gap is real latent dilution sitting above the stock right now. Source: Sivers April 16 directed issue press release. 3. It gets worse. At the June 15 AGM (source: Sivers AGM notice, sivers-semiconductors.com), management is asking shareholders to authorize: → 7M new stock options (P11 program) → Power to issue 15% MORE shares (~46M) with NO further shareholder vote needed 4. Key dates the bulls aren't pricing in: 📅 June 15 — AGM. 15% blank-check authorization vote. 📅 Mid-July — 90-day insider lock-up expires. Board members, CEO, CFO free to sell. (Source: April 16 press release) 📅 Mid-October — 180-day company lock-up expires. New issuance open season. 5. Also confirmed in the AGM notice: a USD $12M convertible loan from Bootstrap Europe at 10.85% interest, maturing Dec 2029. At ~55 SEK/share it's deeply in the money. Conversion = more shares, no vote required. 6. Meanwhile (source: EFN.se, May 18): → Largest shareholder Achilles Capital: 18.2M shares in March → 0 today → CTO sold 42M SEK of stock outside FI disclosure requirements → Three board members leaving simultaneously → Foreign ownership jumped from 15% → 48%, primarily retail via custodian accounts 7. The fully diluted P/S at ~55 SEK: ~70x. Revenue 2025: SEK 307M (restated). Net loss: SEK 223M (also restated wider, source: Sivers 2025 annual report). Don't get me wrong, the CPO/InP thesis certainly seems to be real. However, the current price embeds perfect execution on a pre-revenue photonics ramp while insiders exit and the cap table expands. Read the filings. As always, NFA/DYOR.

To be honest I do believe $SIVE can reach 80b market cap. It's in an exploding market and its peers have done it.... So what prevents them?

This one might be unpopular, but here goes: 🧵 $SIVE has run 1,200% in under a year. Management called the April raise "only 2.5% dilution." Here's why that framing is misleading — and what the filings actually show: 1. The 2.5% figure comes from Sivers' own April 16 press release (MFN.se). What they didn't headline: the denominator already includes ~41M shares of warrants, options and convertibles that don't show up in the basic share count. The 2.5% is technically accurate. The framing is not. 2. Do the math yourself: 8.62M new shares ÷ 2.5% = ~345M fully diluted shares. Basic count post-raise: ~304M. That 41M gap is real latent dilution sitting above the stock right now. Source: Sivers April 16 directed issue press release. 3. It gets worse. At the June 15 AGM (source: Sivers AGM notice, sivers-semiconductors.com), management is asking shareholders to authorize: → 7M new stock options (P11 program) → Power to issue 15% MORE shares (~46M) with NO further shareholder vote needed 4. Key dates the bulls aren't pricing in: 📅 June 15 — AGM. 15% blank-check authorization vote. 📅 Mid-July — 90-day insider lock-up expires. Board members, CEO, CFO free to sell. (Source: April 16 press release) 📅 Mid-October — 180-day company lock-up expires. New issuance open season. 5. Also confirmed in the AGM notice: a USD $12M convertible loan from Bootstrap Europe at 10.85% interest, maturing Dec 2029. At ~55 SEK/share it's deeply in the money. Conversion = more shares, no vote required. 6. Meanwhile (source: EFN.se, May 18): → Largest shareholder Achilles Capital: 18.2M shares in March → 0 today → CTO sold 42M SEK of stock outside FI disclosure requirements → Three board members leaving simultaneously → Foreign ownership jumped from 15% → 48%, primarily retail via custodian accounts 7. The fully diluted P/S at ~55 SEK: ~70x. Revenue 2025: SEK 307M (restated). Net loss: SEK 223M (also restated wider, source: Sivers 2025 annual report). Don't get me wrong, the CPO/InP thesis certainly seems to be real. However, the current price embeds perfect execution on a pre-revenue photonics ramp while insiders exit and the cap table expands. Read the filings. As always, NFA/DYOR.

Where does $SIVE sit in the AI supply chain? This is the part most people miss. Sivers doesn't sell directly to Nvidia or Amazon. They sit upstream of the companies that sit upstream of those hyperscalers. The chain looks like this: Sivers ships InP CW-DFB laser arrays → to companies like POET, Ayar Labs, O-Net, and Enablence, which package those lasers into External Light Source (ELS) modules → those ELS modules feed optical engines built by Celestial AI (just bought by Marvell), Ayar's TeraPHY chiplet, and Lightmatter's Passage → those optical engines plug into ASICs designed and packaged by Marvell, Broadcom, and Alchip → which become AWS Trainium, MSFT Maia, META MTAI, Google TPU, and Nvidia Rubin clusters Four layers up the chain from the GPU. That's why nobody saw them. And that's exactly why they matter. The laser is the input that nothing else in the stack works without. You can swap optical engine vendors. You can swap packaging vendors. You cannot swap the laser source without a 2–3 year requalification cycle that nobody has time for in a 2027–2028 ramp window. That is what supply chain analysts call a chokepoint. @aleabitoreddit calls it "the kingmaker for CPO." The structural position is real. The only debate is whether Sivers specifically captures the volume, or whether Lumentum and Coherent eat the share from above. More on that later. $NVDA $META $MSFT $AMZN $GOOG $AVGO $LITE $COHR $MRVL $POET

The $LITE comp - $SIVE / $SIVEF Lumentum was a sleepy optical components supplier for a decade. Trading at 1–2x EV/sales. Nobody cared. Then the AI buildout started, and the EML laser - the specific component Lumentum was the dominant supplier of became the non-substitutable bottleneck for current-generation 800G and 1.6T optical transceivers. Nvidia secured all the EML capacity it could before everyone else figured out it was a chokepoint. Lumentum went from ~$3B market cap to $50B in eighteen months. A 15–20x re-rating. Nvidia followed up with a direct $2B equity investment to lock down capacity. Same playbook with $COHR ($2B) and $MRVL ($2B). Three $2B checks written to control the optical layer of the AI stack. $SIVE is the same trade. One node upstream. One generation earlier. $LITE = EML lasers = current-gen pluggable transceivers (the bottleneck of today). $SIVE = CW-DFB laser arrays = next-gen co-packaged optics (the bottleneck of 2027–2028). This is exactly what @aleabitoreddit called out when he started building his position. His words: "$SIVE sits in the silicon photonics CW DFB laser bottleneck of the next gen photonic architectures spearheaded by $NVDA. This is compared to how $COHR / $LITE EML lasers are the current optical transceiver bottleneck." The critical asymmetry: Nvidia has paid $2B EACH into $LITE, $COHR, and $MRVL to lock down current-gen optical capacity. They haven't done it yet with Sivers. The pattern says they will - or someone else will get there first. Marvell could take a 10–20% stake in Sivers for ~$300M and effectively secure their billion-dollar CPO program supply chain. Broadcom could acquire the entire company for what amounts to a rounding error against their $1T+ market cap. The trade isn't "buy at $130M before anyone notices" - that window closed in March when this thing did 20x in twelve months. The trade now is whether the next leg is another 3–5x as CPO volume materializes, plus the embedded acquisition optionality.

I want to give everyone the full breakdown on $HLIT because this is one of the most compelling setups I have come across in a long time. Harmonic spent 35 years building broadband expertise and just completed a full transformation from a hardware company into a pure play broadband software platform. The video business just sold to MediaKind for $145 million. What remains is one of the most defensible software moats in the market. The product is called cOS. And here is why it matters. Every cable operator in the world runs physical CMTS hardware. Massive proprietary boxes costing hundreds of thousands of dollars per node that have to be physically replaced every few years. Truck rolls. Technicians. Capital expenditure that never ends. The economics for operators are brutal. cOS virtualizes the entire cable access network in software. Buy the platform once. Run it on standard cloud hardware. No proprietary boxes. No replacement cycles. Software updates deploy remotely. Capacity scales with a license not a truck roll. Once an operator converts the switching costs are enormous. You do not rip out the software layer running your entire broadband network. That is why cOS commands greater than 95% market share in virtualized CCAP deployments. Every major US cable operator is already a customer. Now here is the catalyst that makes this a must own right now. DOCSIS 4.0. The largest infrastructure upgrade in cable history. AT&T fiber now passes 28 million plus homes. Frontier is aggressively overbuilding. T-Mobile fixed wireless is accelerating. Every month Charter or Comcast delays DOCSIS 4.0 they lose broadband subscribers to fiber offering symmetric gigabit at comparable prices. This upgrade is not optional. It is a survival imperative. Charter committed $5.5 billion to DOCSIS 4.0 upgrades with full network completion in 2027. Comcast mid ramp targeting 5 Gbps symmetric by 2026. Cox committed multi gig to 65% of its footprint by 2028. Every single one of those deployments requires a Harmonic cOS license. Mandatory decade long capex cycle. $HLIT is the only production grade platform in the market. There is no alternative. And AI is pulling the cycle forward faster than anyone expected. Consumer AI proliferation is driving upstream bandwidth demand at 20% annually per Harmonic’s own operator data. That rate makes mid split upgrades insufficient within 18 months. DOCSIS 4.0 becomes mandatory ahead of schedule and $HLIT revenue comes with it. Q1 confirmed the ramp is here. Revenue $121.7 million. Up 43% year over year. Beat the top of guidance by 16%. Largest quarterly beat in company history. Operating profit up 115% year over year. Backlog at $582 million up 87% year over year. That is 1.2x full year revenue guidance already sitting on the books before a single new order is added. Full year guidance raised to $475 to $495 million. Free cash flow estimated at $110 to $130 million for the year. Gross margins running at 52% today and expanding as the software mix grows. Pure play broadband software companies with 50% plus gross margins trade at 4 to 6x EV/Revenue. $HLIT currently trades at 3.5x forward revenue. The re rate has not happened yet.

When the current cycle is over, sites like Yahoo Finance will not be showing photos like this one...