TheGreatestDane

9 posts

Really hoping this is just bad social media bait from the white house.

They posted a pixelated image of Trump, who looks like he is ready to press a red button (nuke?).

Two interesting names worth watching:

$BWXT: $20B market cap. Sole-source manufacturer of naval nuclear reactors and fuel for the US government. The pure play.

$HON: $143B conglomerate. Quietly operates the NNSA's primary nuclear weapons components facility in Kansas City and manages Sandia National Labs. Buried inside a mega-cap, basically unnoticed.

One builds the deterrent. The other builds the warhead components. Both are US government sole-source contracts.

Hoping it does not escalate further, but these names stand to benefit even if the US decides to ramp up their possibilities.

$BWXT $HON

The White House@WhiteHouse

English

$ASTS has a path to becoming a trillion dollar company and the math isn’t complicated.

Let me show you exactly how it gets there.

Start with Starlink as the benchmark.

Starlink took 5 years, over 10,000 satellites, and tens of billions in capital expenditure to reach 10 million subscribers and roughly $10 billion in annual revenue.

SpaceX is now targeting a $1.75 trillion IPO valuation with Starlink’s implied value sitting around $1.17 trillion on that subscriber base.

10 million subscribers. $10 billion revenue. $1.17 trillion implied value.

$ASTS is targeting 5 billion mobile subscribers globally. Not 10 million. 5 billion. And the business model is structurally superior to Starlink in every way that matters for scale.

Starlink competes with carriers. They built their own hardware, their own dish, their own subscriber acquisition funnel. Every customer has to buy a $600 terminal, cancel their existing provider, and switch to a new service.

Customer acquisition is expensive and friction is high. That is why after 5 years and 10,000 satellites they have 10 million subscribers.

$ASTS does not compete with carriers.

They partner with them. AT&T, Verizon, Vodafone, Rakuten, Orange, TELUS, and 50+ operators worldwide have already signed agreements.

Those carriers collectively cover 3 billion existing subscribers whose phones are already hardware compatible.

No new device. No new plan. No new anything. The carrier offers satellite coverage as a simple add-on and the existing customer base opts in. Zero customer acquisition cost on $ASTS’s side.

Starlink charges $120 per month per residential customer. $ASTS operates on a wholesale model where carriers pay per subscriber. A $5 per month add-on to an existing carrier plan is not a stretch.

Carriers charge $15 to $30 per month for international roaming today. A dead zone coverage add-on in rural America, at sea, or in the air is a premium feature people will pay for without thinking twice.

Now run the math.

1 billion subscribers at $5 per month is $60 billion in annual revenue. That is 20% penetration of the 5 billion subscriber target. That is 33% penetration of the 3 billion already on partner carrier networks.

Starlink is valued at $1.17 trillion on $10 billion in revenue. That is roughly a 117x revenue multiple. $ASTS generating $60 billion at a fraction of that multiple tells you everything you need to know.

At 15x revenue on $60 billion that is a $900 billion market cap. At 20x that is $1.2 trillion. At Starlink’s implied multiple it is multiples beyond that.

But let’s stay conservative. Even at 10x revenue on $60 billion that is a $600 billion market cap from a $35 billion market cap today.

That is 17x from here on a scenario that requires 20% penetration of an addressable market where the distribution is already built and the hardware is already in billions of pockets.

Now look at this realistic time line.

BlueBird 6 is already in orbit. The largest commercial communications array ever deployed in LEO, exceeding 120 Mbps peak data speeds.

Commercial service activating this year across the US, UK, Japan, and Canada. $3.9 billion in cash on the balance sheet fully funding the constellation buildout. Zero dilution risk on the launch campaign.

The 2025 revenue was $70.9 million. 2026 guidance is $150 to $200 million as commercial billing starts and government contracts ramp. The revenue line is just starting to move. The subscriber base is not priced in at all.

Starlink needed 10,000 satellites and 5 years to get to 10 million subscribers fighting for every single one. $ASTS needs 45 to 60 satellites and already has 3 billion potential subscribers sitting in their partners’ existing customer bases waiting for the switch to flip.

The constellation is almost complete. The carriers are signed. The phones are compatible. The revenue is starting.

$35 billion market cap. $1 trillion is the destination. The satellites are going up now.

English

‼️ You don’t need 20+ stocks to be successful in this market.

You just need a couple you deeply understand.

$ASTS $AAOI $KRKNF $NBIS

are my current holdings that will bring generational wealth 🤝🏼

English

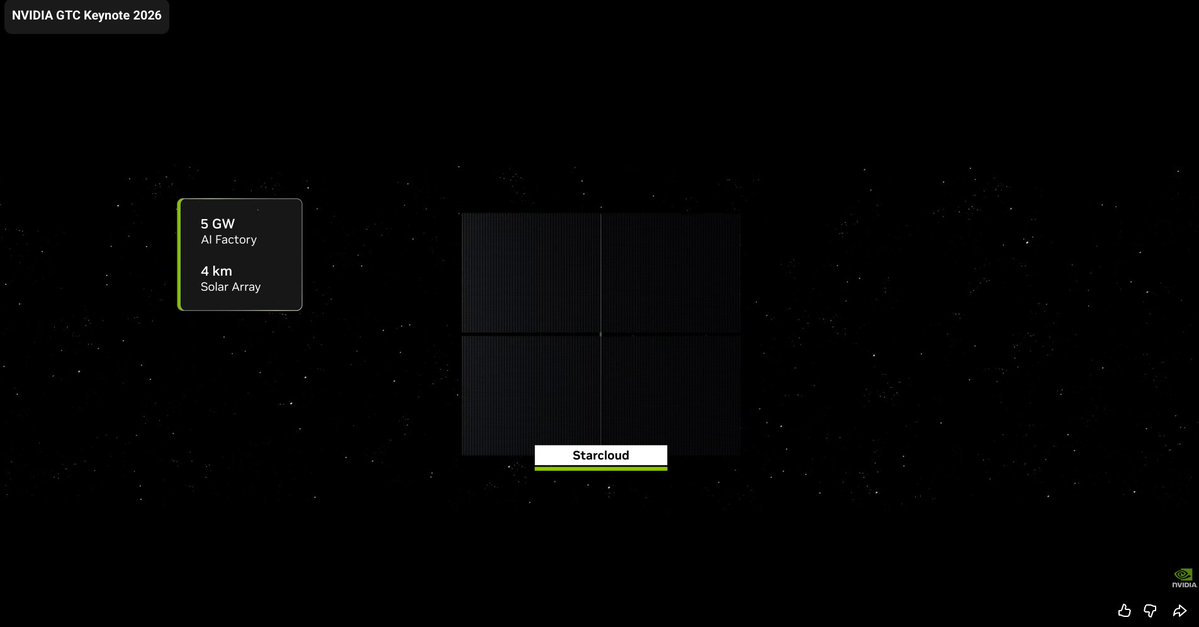

BREAKING: NVDA JUST SHOWED SATELLITES AT NVDA GTC KEYNOTE 2026

Orbital datacenters may be more relevant than most people realise.

Wonder who is positioned to benefit from this shift?🤔

$NVDA $ASTS

PhotonBull@PhotonBull

NVIDIA GTC is next week. Everyone is talking about CPO and photonics. Nobody is watching for orbital datacenters. NVIDIA already has an Orbital Datacenter System Architect job posting live on their site. It's been up for a while. If Jensen mentions space compute on that stage, most people will be caught off guard. They shouldn't be. Now ask yourself: if orbital datacenters become real, who has the satellites large enough to actually host compute in LEO? $ASTS. They operate the largest commercial satellites ever launched. More surface area, more power, more capacity. NVIDIA doesn't build hardware in space. They will need a partner. Watch GTC closely. $NVDA $ASTS

English

@AlmaCap114204 Jensen mentioning photonics would be absolute 🔥🔥🔥

English

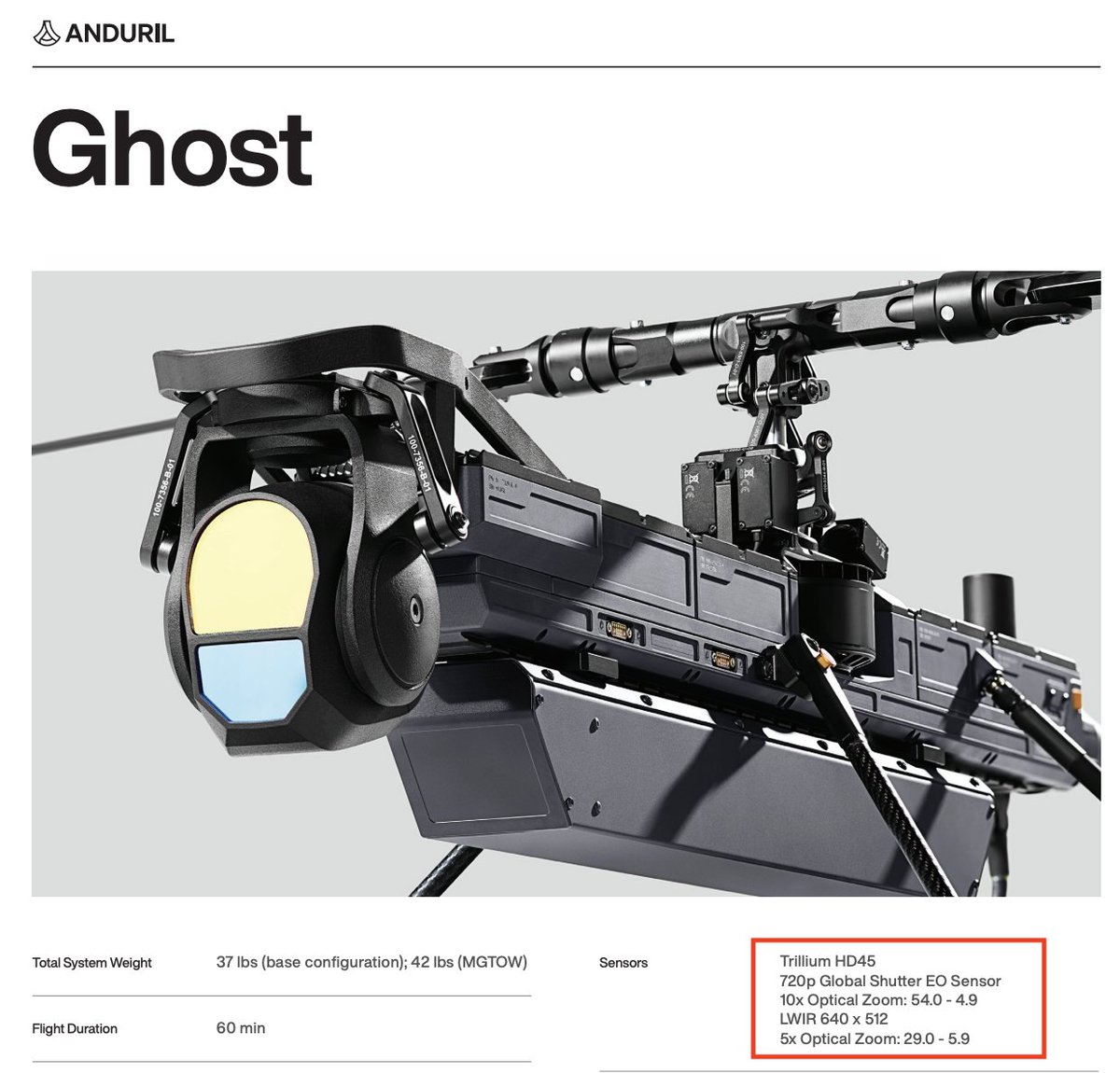

$LTRX - The Hidden Anduril/ONDAS Play Trading at a Fraction of Comps

The Anduril supply chain keeps expanding. Here's one nobody's talking about.

Lantronix just dropped a partnership with Safe Pro Group this morning. Most will scroll past it. Here's why that's a mistake.

The Connection Nobody's Made:

Safe Pro Group is the company Ondas Holdings poured $14M into back in October. $ONDAS now has a $5B market cap trading at 100x+ sales.

But here's the real alpha: In December, Trillium Engineering selected LTRX Edge AI modules to power their gimbaled imaging systems for military drones.

Pull up the Anduril Ghost spec sheet. The sensor listed? Trillium HD45.

Connect those dots. LTRX appears to be in Anduril's supply chain. And now they have a direct relationship inside the ONDAS ecosystem too.

The Valuation Gap Is Absurd:

$ONDS - $5.0B market cap, ~$50M rev, 100x P/S $RCAT - $1.6B market cap, ~$40M rev, 40x P/S

$KRKNF - $1.6B market cap, ~$100M rev, 16x P/S

$OSS - $250M market cap, ~$30M rev, 8x P/S

$LTRX - $270M market cap, $118M rev, 2.3x P/S

$LTRX has more revenue than $ONDS, $RCAT, and $OSS combined. Trades at a fraction of the multiple.

Why the Disconnect?

$KRKNF is known as the Anduril sonar/battery supplier. That connection drove a 250%+ run.

$LTRX has the Anduril imaging connection through Trillium and nobody is talking about it. They also have Red Cat for the Army SRR program.

Three nodes in the defense drone ecosystem. One stock trading at legacy industrial multiples.

The Setup:

5x P/S (half of $KRKNF) = $590M = 2x

10x P/S (still below comps) = $1.2B = 4x

English

You need to own these stocks:

$ASTS

$ABVX

$SATS

$KRKNF

- Mikael Kemström

Čeština

Mkay folks, know what a lot of investors tend to miss? ASYMMETRIC opportunies.

Companies like Kraken Robotics and AST SpaceMobile are quietly building the kind of foundational infrastructure that becomes incredibly valuable long before the market prices it in.

ASTS is putting together a game-changing communications network in space, while Kraken is delivering the subsea sensing, autonomy, and power tech that powers modern naval ops and keeps us aware of what's happening underwater.

What really gets me excited is Kraken's partnership with Anduril. As Anduril ramps up its autonomous undersea platforms, Kraken's sonar and subsea power solutions get pulled right into a much bigger defense ecosystem with real production scale and deployment muscle. Just the other day we saw Trump announce the desire to increase the defense budget from $1T to $1.5T…

On top of that, the new manufacturing facility in Nova Scotia is a big deal. It seriously reduces execution risk, boosts capacity, and sets Kraken up perfectly to handle growing demand from NATO and allied navies. We're watching the company shift from "development story" to "serious industrial scaler" RIGHT in front of us.

And yet, Kraken still trades at a huge discount compared to peers such as Ondas Holdings, which often gets sky-high multiples just for its future autonomy potential. Even though it's still burning cash with limited revenue. Kraken, is already generating real revenue with incredible margins as a defense tech supplier, with actual customers, a solid backlog, and now manufacturing scale to back it up.

Once it uplists to the TSX (and eventually Nasdaq), better liquidity and more institutional eyes could spark real peer comparisons. This can set the stage for the same kind of re-rating we've seen in other defense infrastructure names when the market finally wakes up to their true strategic importance.

Shout out to @transhumanica for their detailed analysis that covers both companies.

transhumanica.com

$ASTS #ASTS

$KRKNF #KRKNF

English

$HIMS will reach all-time highs in the future.

But, there will be bigger red days coming soon.

When the dip comes, buy it and you'll be a millionaire and set your family up for life.

English