Sabitlenmiş Tweet

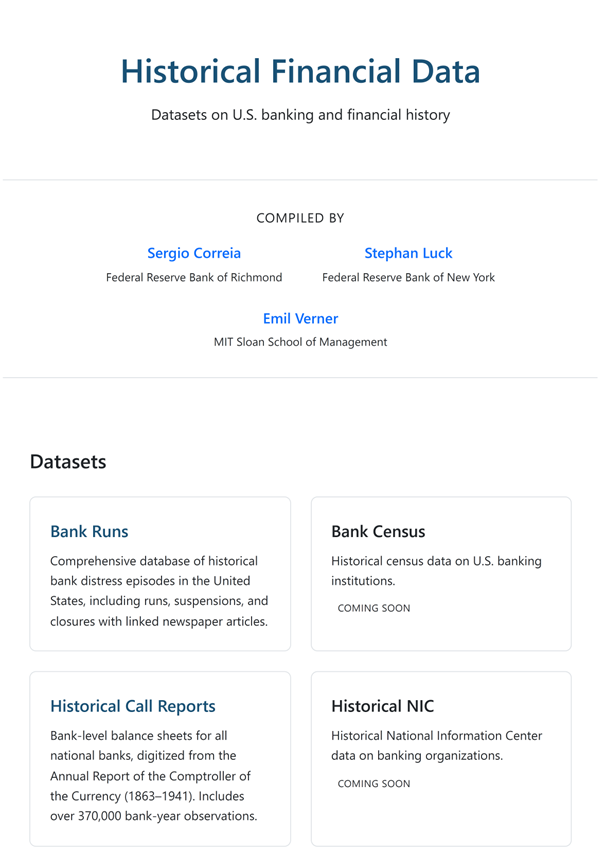

New paper on bank runs with Correia and Luck:

"Bank Runs With and Without Bank Failure"

Questions:

- What are the determinants of runs?

- When do bank runs result in bank failure?

- Can runs trigger the failure of healthy banks and amplify small shocks into large crises?

- Are runs themselves the initial cause of financial distress or are they a symptom of deeper fundamental solvency problems in the financial system?

What we do:

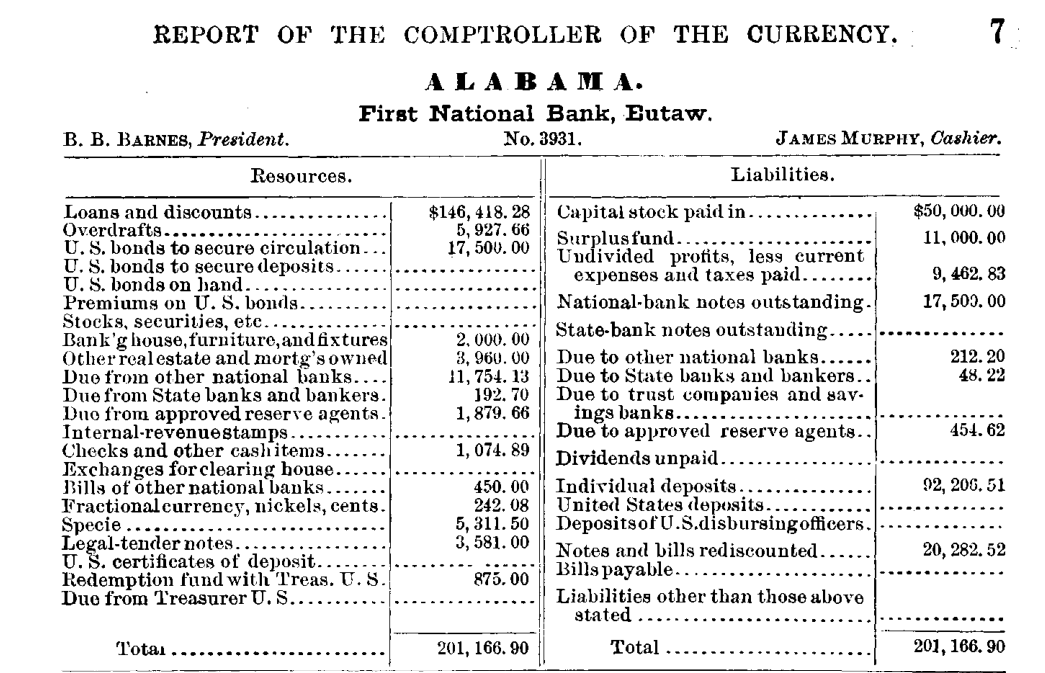

- Apply LLMs to historical newspapers to uncover over 4,000 runs on individual banks in the pre-FDIC US banking system from 1863 to 1934. Capture the most famous runs (Bank of the US

- Merge data on runs and other bank-level events discussed in newspapers (suspensions, failures) to bank-level fundamentals (harder than it sounds!)

What we find:

(1) Runs are considerably more likely in weak banks, but can also occur in strong banks, especially in response to negative news about the real economy or the broader banking system.

(2) However, runs typically only result in failure for banks with weak fundamentals [see figure below]. Strong banks survive runs through various mechanisms, including interbank cooperation, equity injections, public signals of strength, and suspension of convertibility

(3) At the local level, poor fundamentals necessary for runs to translate into large declines in lending. Moreover, bank failures (with and without runs) translate into substantially larger declines in deposits and lending than runs without failures.

Overall takeaways:

- Poor fundamentals are key for whether runs pass through into failure and have severe consequences for the broader economy.

- The findings temper the view that small shocks can result in large jumps to bad equilibria via runs on demandable debt.

Full paper here. Comments welcome. Given the methodology and evolving AI tools, we expect to make refinements to the runs database over time. Any input is welcome.

static1.squarespace.com/static/58f6b1c…

English