Sabitlenmiş Tweet

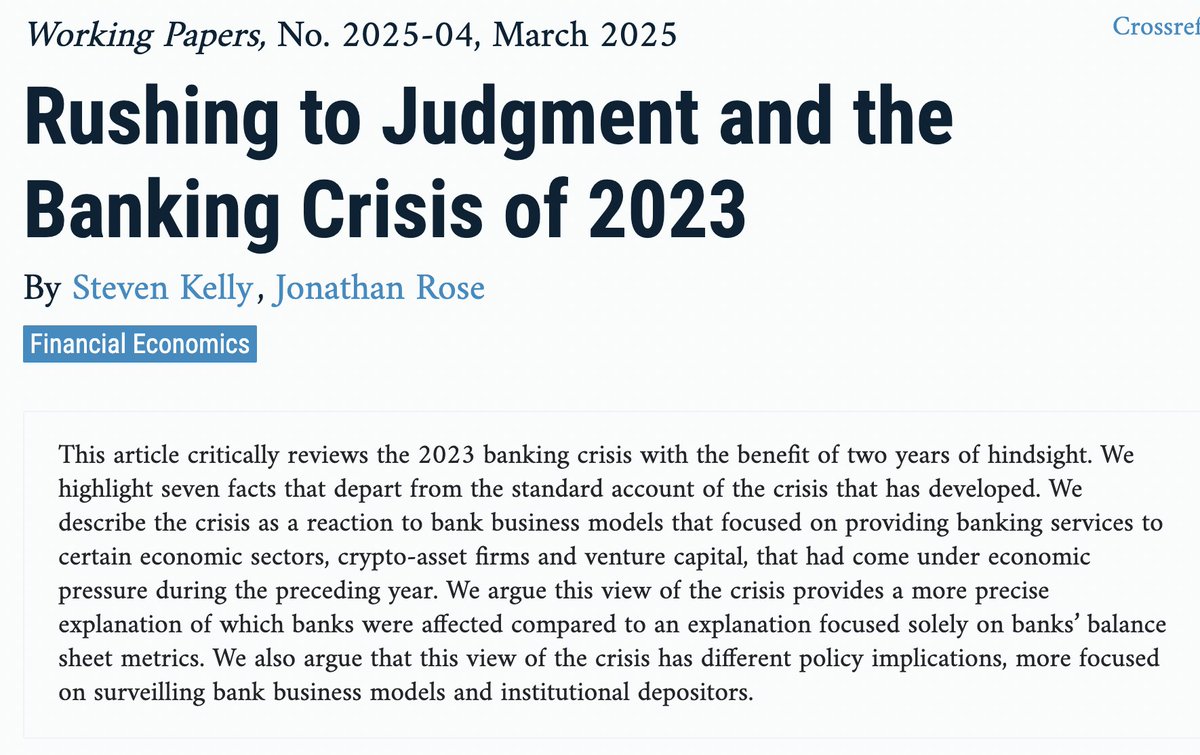

New paper: "Rushing to Judgement and the Banking Crisis of 2023"

At the two-year anniversary of the crisis, @thejonrose and I present 7 facts that are overlooked in the standard account of the crisis: chicagofed.org/publications/w…

English