@BrentAHensley1 @SantiagoAuFund However, there are clear implications for fx, that’s how a lot of the costs will be borne. DM will experience stagflation the risk of it imo. That has implications, too, however fast.

English

Eric Fine

506 posts

@EricFine123

EM economist and bond investor for 30+years Disclosures: https://t.co/Gl2tsi0aNn.

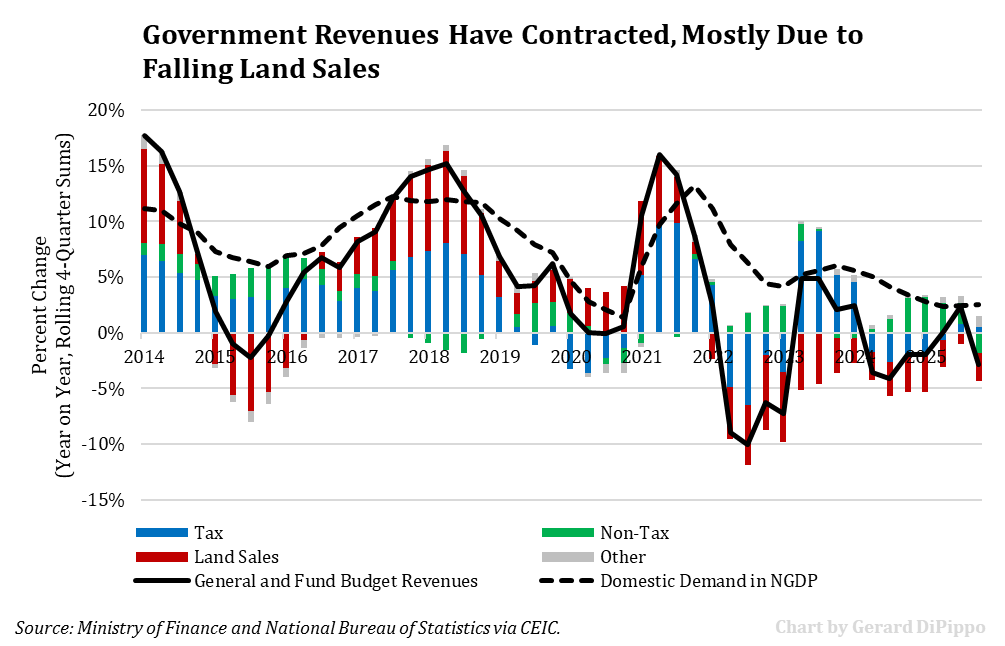

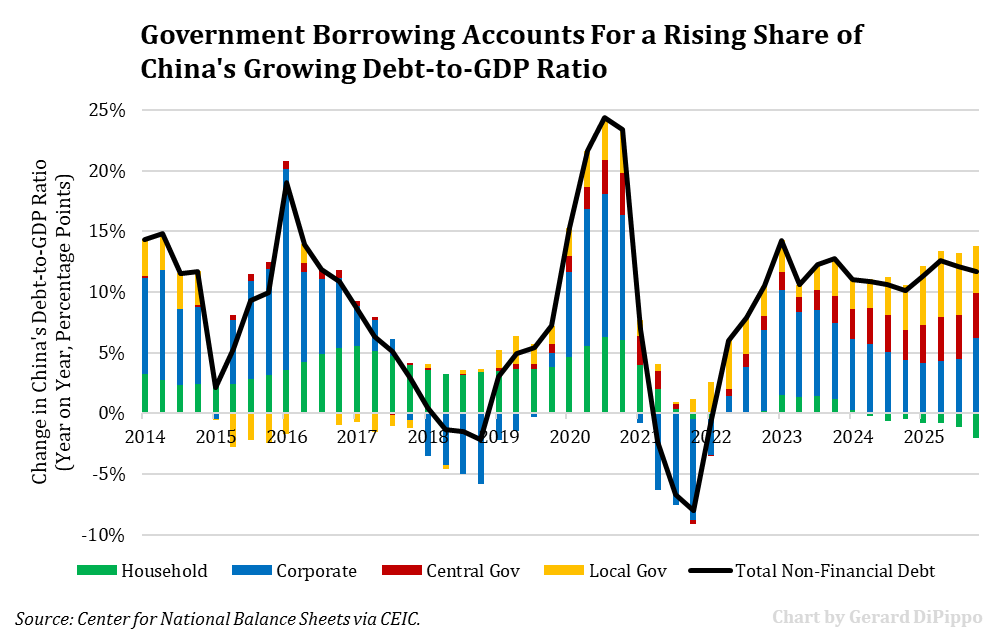

Frugal ‘Iron Rooster’ Budget Signals Pain for Growth and Consumers @Lingling_Wei wsjchina.cmail19.com/t/d-e-ghjlryd-…