$FRMO market cap roughly equal to its look through $TPL ownership. Cash, MIAX etc all for free. Not sure if the value ever gets unlocked, but can’t see much downside from here.

English

Escape Velocity

577 posts

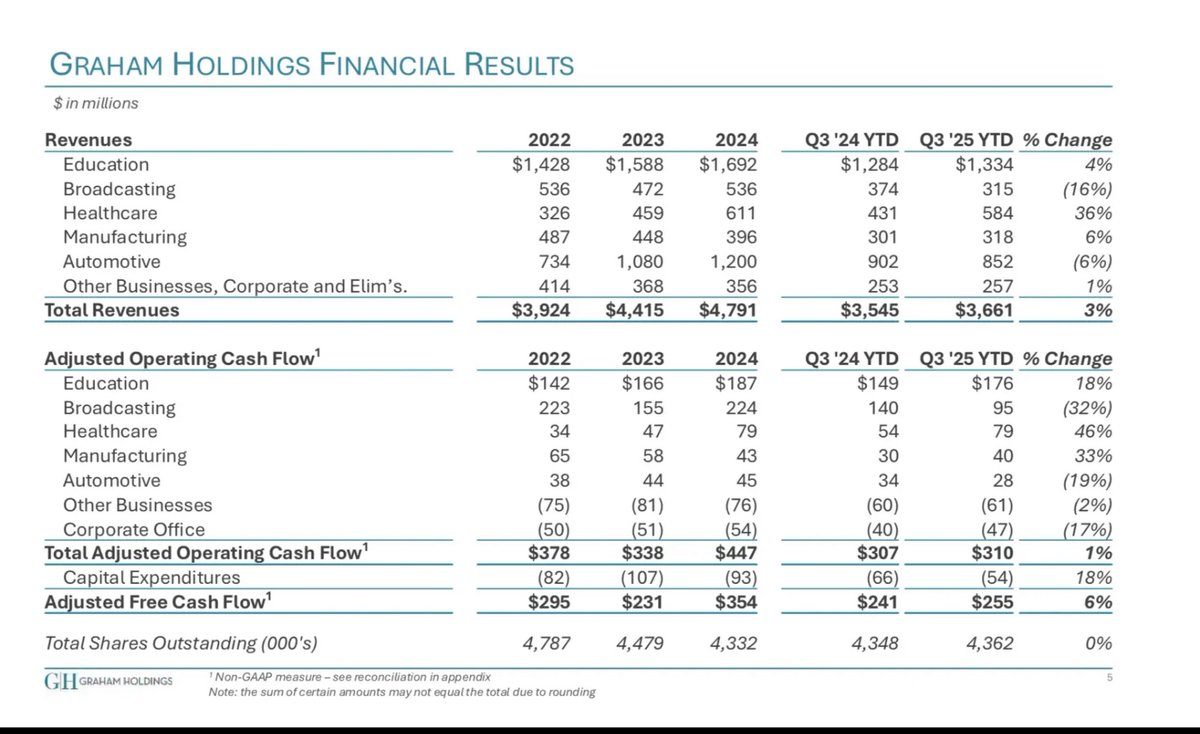

@F_Compounders The multiple for $GHC is irrelevant because they have a securities portfolio where mtm changes flow through to the income statement. It was really cheap a few years ago but is about what it’s worth now.

Lawsuit key would be to use the recent proxy vote results to try to shift a legal argument from the "Business Judgment Rule" to the "Entire Fairness" standard, which is much harder for the $UNF board to win. Rather than doing this, $UNF should engage w/ $CTAS to get best deal.

How is this $CTAS offer for $UNF at $275/shr different from the same offer they made a year ago? Going to be tough sledding to push this through with the dual-class share structure.