Sabitlenmiş Tweet

Why Do Markets Go Up? factorinvestor.com/blog/why-do-ma…

Manhattan, NY 🇺🇸 English

Ehren Stanhope

2.9K posts

@FactorInvestor

Chief Investment Strategist and Co-Head of Investments. Researcher of Financial Markets https://t.co/V6c32YhRIG. Avid Reader. Proud New Orleanian. Father. Husband.

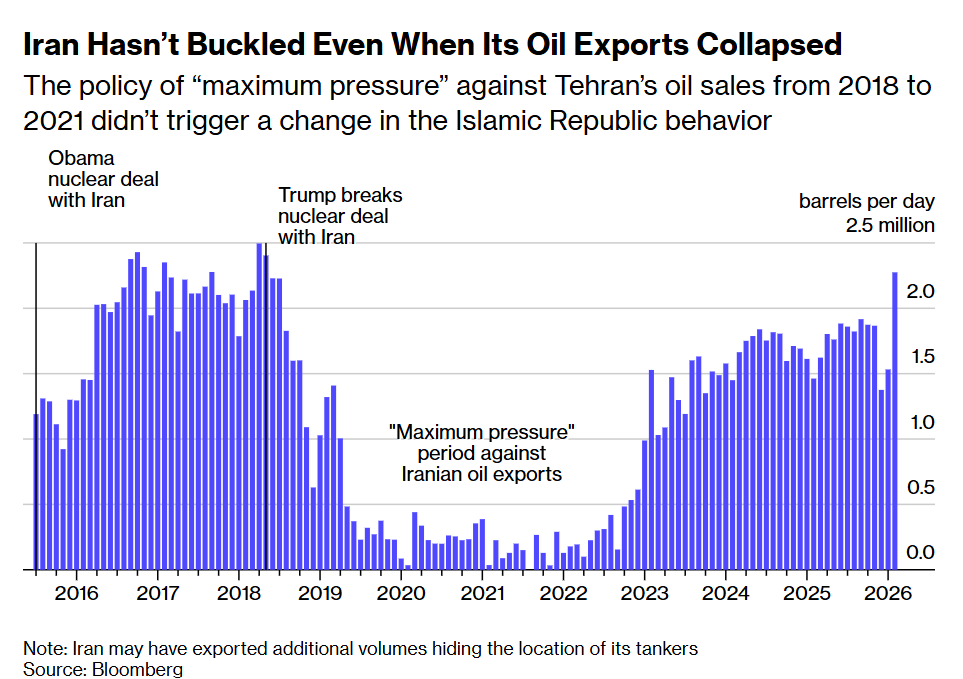

With both sides now coming to the negotiating table, we could see volatility calm down as we move into Spring... HOWEVER... the WH will likely continue to apply kinetic pressure to facilitate negotiations with China (and Iran via proxy) on a path forward. It will take some time for the world to parse through the economic impact of intensified global competition, which will almost certainly impact supply chains, trade, and the global security apparatus. In 2026, we have seen two dramatic security shifts - a reincarnation of the Monroe doctrine with VZ in the Western Hemisphere, and a rewriting of the status quo in the Middle East with Iran. A third will manifest at some point. With Japan set to re-militarize and US-Sino negotiations set to begin, expect a reset in Asia as well, though hopefully much more subtle! While volatility may decline, one can argue it will settle in at either a higher absolute level or with greater dispersion within equity indexes until a clearer path is well-established.

This is Wild. Deutsche Bank has developed an index that helps to predict the next TACO by Trump. It has proven effective in previous big Trump pivots. The "Pressure index" combines one-month change in approval ratings, one-year inflation expectations and performance of the S&P 500 & t-bill yields. The higher it goes, the greater the chances of 🌮

The most challenging thing about this market environment is that global macro factor correlations are trending towards 1, which means portfolio diversification is disappearing beneath the risk models. Look at a chart of stocks, gold, silver, bonds. It’s all correlated since the conflict in Iran broke out. Oil is the only diversifier, and as we saw yesterday, that has its own risks. Really tough time to allocate with conviction.

Volatility set to continue this week as: 1. Despite the President's Friday tweet, kinetic actions are likely accelerating. 2. Degrossing and repositioning is rampant across asset classes. 3. Markets struggle to price in both an economic growth shock (recession) and an energy supply shock - obviously inter-related. 4. Equities are waking up to the possibility of a prolonged impaired growth trajectory. 5. Rates actually matter now to bellwethers given AI-related debt issuance. There is currently an asymmetric downside to being early back into risk assets. Important to note in this regime that bonds are no longer risk-free given inflation risks. We've been discussing this structural shift for a few years with clients. There will be an entry point, but it probably won't be a flash point as has existed in previous crises with the Fed swooping in to the rescue. They are hamstrung here in what I call Policymaker Purgatory.

This is going to be a challenging week in financial markets ahead. Investors will be forced to reconcile with either prolonged conflict or prolonged disruption in the flow of critical commodities. Either gets you to the same place, some version of extreme risk: existential (the Gulf States raison d’etre), economic (everyone loses during kinetic conflict), and inflation (lock in of critical energy, AI, and agricultural commodities). This conflict too shall pass, but on what timeline and what long-term impact to financial markets, nobody knows.

The Federal Reserve received grand jury subpoenas from the Justice Department on Friday that threaten a criminal indictment relating to Chair Jerome Powell’s testimony last summer about the central bank’s building renovation project Powell statement: federalreserve.gov/newsevents/spe…

Pretty interesting: Companies that have adopted AI aren't hiring fewer senior employees, but they have cut back on hiring juniors ones.

CNBC just dragged a "gold expert" on that recommends selling your gold for bonds. 🤣

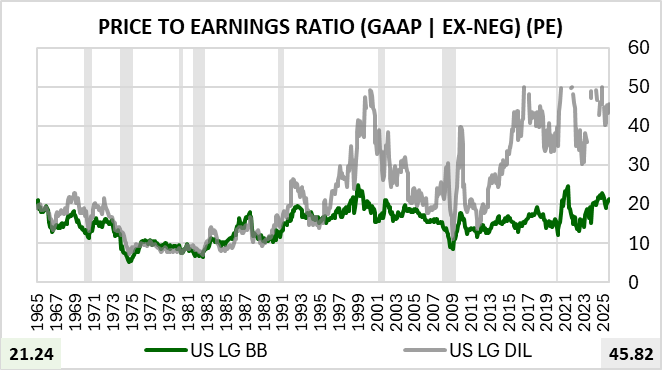

While accurate and agreed that US equities are expensive, the structure of the market is very different and much healthier. US Large cap profit margins then ~9% vs nearly 15% now. (1st chart) In terms of capital allocation, there was massive share issuance (dilutive) and massive "investment" in the internet (read burning cash) -> Profligate Without Profit. 2nd chart. One could argue that now we are Profligate With Profit (3rd chart) h/t @Jesse_Livermore for the charts