Sabitlenmiş Tweet

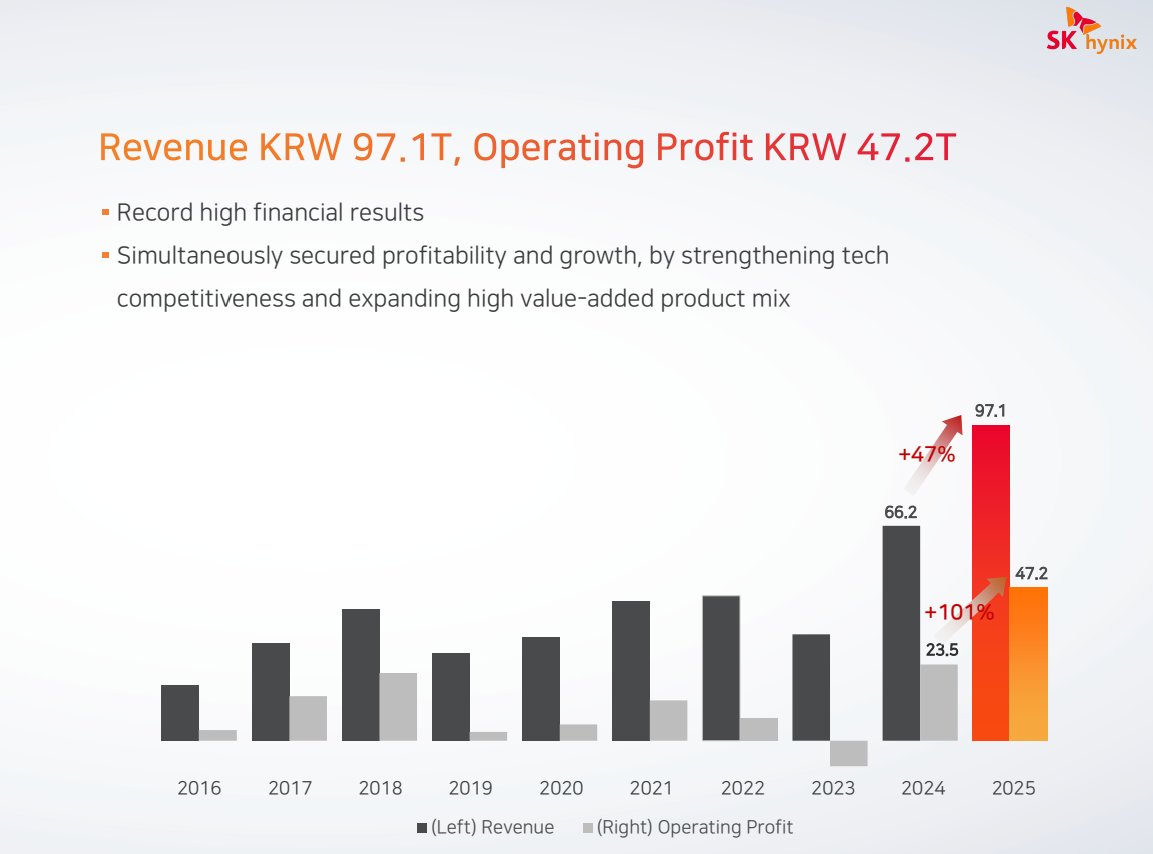

@SKhynix is probably the most interesting Company that I am currently owning. A stock I've been researching since 2024, when SK Hynix was the first to buy $ASML's High-NA EUV's, but only recently pulled the trigger.

Maybe a bit late, but better late then never. So far up +40% and counting on it but let me tell you why I actually like SK Hynix. $DRAM $EWY $KOSPI

When mapping the AI infrastructure buildout, I don't just look for the fastest chips. I look for the physical bottlenecks.

Right now, the absolute bottleneck in AI is memory. A $40,000 Nvidia GPU is useless if it is starving for data. Standard memory simply cannot feed data fast enough to keep up with the compute cores.

Enter HBM (High-Bandwidth Memory). HBM acts as a massive, vertically stacked data highway built directly next to the GPU.

SK Hynix completely dominates this space. They hold the monopoly on keeping Nvidia's chips fed. There are players like $MU or Samsung, but SKH managed to capture the biggest pie.

Now, the thesis just got a massive structural upgrade:

SKH just announced mass production of SOCAMM2 192GB for Nvidia’s next-gen Vera Rubin servers.

Why is this a game-changer?

1. AI data centers are physically running out of electricity. Memory traditionally consumes a massive percentage of a server's power budget.

What SK Hynix is doing with SOCAMM2 is taking LPDDR (Low-Power memory, historically only used in smartphones to save battery) and packaging it into a dense 192GB module for enterprise servers.

It delivers >2x the bandwidth while slashing power consumption by >75% compared to standard server memory (RDIMM).

Nvidia is effectively forced to use mobile-grade low-power architectures because standard server memory draws too much electricity.

2. Right now, SK Hynix dominates HBM, which sits directly next to the GPU. But an AI server also has a CPU (like Nvidia's Grace CPU), which requires primary system memory.

By securing the SOCAMM2 contract for the next-generation Vera Rubin chips, SK Hynix is proving they are not just winning the GPU memory war.

SK Hynix are successfully monopolizing the entire memory layer of the Nvidia AI server rack and lock Nvidia into their ecosystem years in advance (Rubin is the generation after Blackwell).

Despite this unbreakable supply chain dominance, the market still prices memory like a boom/bust commodity while they are transitioning into a custom-engineered silicon partner for $NVDA and others.

I strongly believe, this time it truly is different. What are your thoughts?

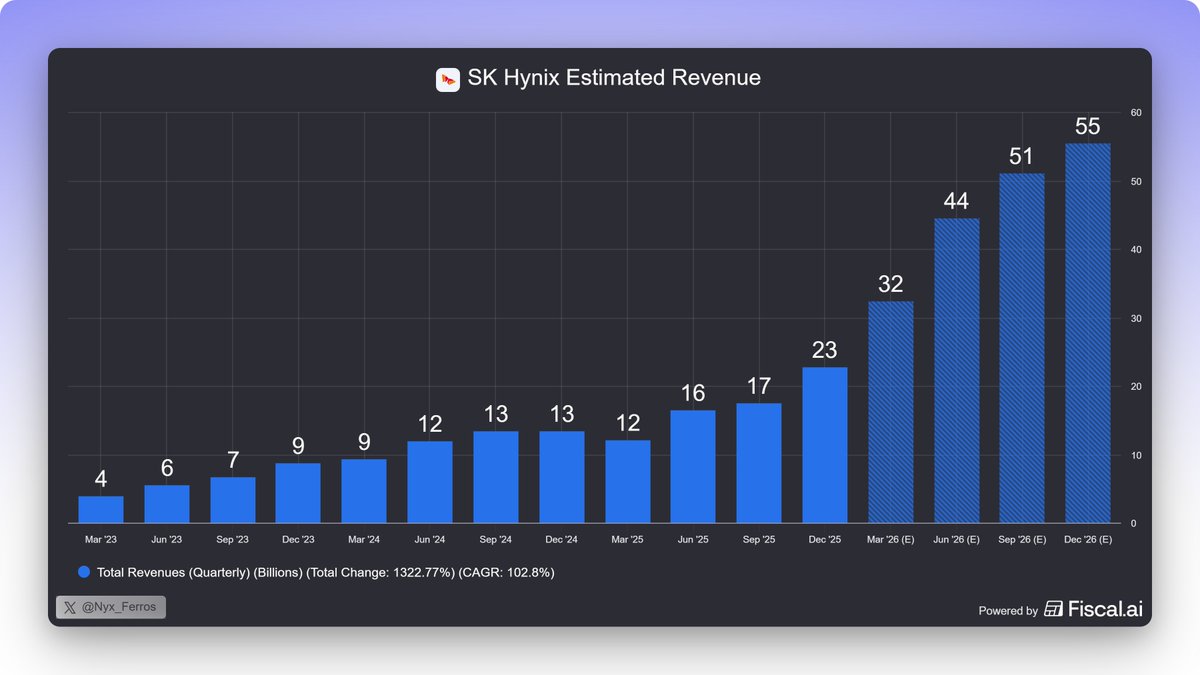

Data by @fiscal_ai

English