F

96 posts

开源钱包也不是绝对安全。Electrum 被恶意服务器偷了几千 BTC,Parity 开源合约直接丢几千万刀,还冻结几亿。开源能审计是好,但漏洞公开、维护断档、假版本横行一样会丢钱。安全从来不是‘开源/闭源’二元对立,而是实现质量 + 用户习惯。Ledger 闭源有风险,但开源项目翻车案例也不少,不用把开源当万能护身符。

要考虑的东西很多,企业品牌,用户量,硬件设备制造水平,芯片安全水平,最主要的是使用习惯。

中文

我可以分享下我的硬件钱包使用心得:

1, 多年以前,我觉得数据线是一个问题,因为要让我的钱包链接一个可能被攻击的笔记本电脑,看起来不是很安全?所以当你我首先选择的是蓝牙传输。

但其实,数据线链接远比蓝牙更安全!

理论上蓝牙是存在额外的潜在风险(如蓝牙协议漏洞、信号拦截、配对劫持等),虽然 Ledger 官方反复强调“私钥永远不会离开 Secure Element”,即使蓝牙被攻破也需要你在设备屏幕上物理确认。

2,硬件钱包的最大价值,就是让你即使在“不安全”的电脑上操作,也能安全。这也是为什么很多人用普通笔记本就行。

3.为什么 Ledger 能让“被黑的电脑”也安全?

私钥永远不离开 Ledger 设备:

我说一个极端情况:

【即使你把 Nano S Plus 用 USB 插到一台满是病毒的电脑上,私钥和种子词也不会被电脑读取或泄露。它们只存在于设备的 Secure Element 芯片里】。@Ledger

4.设备上验证是核心保护:

Ledger Live 里显示的交易地址/金额可能被恶意软件篡改,但设备屏幕上显示的才是真实、不可篡改的。

你只要对比一下就行,如果不一致,就直接拒绝签名就OK。

Ledger 官方明确说过:“即使电脑被恶意软件完全控制,也无法控制你的 Ledger 钱包”。

恶意软件最多只能骗你(比如改剪贴板地址),但骗不过你自己在设备上的手动确认

5,当然如果你实在是放心不下,就多花几千块买台mac os的笔记本,啥也不装,就装ledger钱包。

以上。

CryptoV|Global Markets@CryptoV_Alpha

又买了2个Ledger,送给家人来存储用。 记不清是第N次买这款钱包了,蓝牙X版已经用烂了2个,新出的大屏幕我还是不喜欢,最喜欢的仍然是他们家的Nano经典款。 @Ledger 我们圈内包括很多散户,动不动一单亏损几百几千几U,但是确舍不得花几十U给自己的大额资金配个钱包。 这对吗??

中文

最近Tether冻结了TRON生态里3.44亿USDT

各种猜测在我看来纯属降智

仔细看路透社的报道 依然是打击犯罪

无论Justin Sun或者TRON

都不存在被谁针对或者报复的情况

相反 TRON、Tether、TRM Labs联合成立了T3+

加密行业首个专注打击链上非法活动的合作

我只能说 又让水军和黑子失望了

@justinsuntron

中文

对 $HYPE “回购”的误解

针对 Hyperliquid 最激烈的批评之一是,它每天都会“回购”代币,一些人认为应该根据价格调整回购量。

Jeff 的回应直截了当地说:这个前提是错误的。

“主要问题是 Hyperliquid 没有自主回购计划”。

协议费用通过链上逻辑自动转换和销毁。没有任何人为因素或执行委员会干预市场时机。

这为什么如此重要?

“因为 Hyperliquid 不是一家公司”。

这是一个基于规则的协议。

指望随意回购token是对它设计的误解。它的愿景是像基础设施一样运作,更像是互联网而不是银行。

MR SHIFT 🦁@KevinWSHPod

Jeff Yan on Building the Internet for Money, and why Hyperliquid isn’t just a crypto company In this episode of When Shift Happens, I sit down with @chameleon_jeff, Founder of @HyperliquidX, to reflect on one of crypto’s most extraordinary moments: a $1 billion community airdrop that grew into $10 billion in value. But this conversation goes beyond wealth to focus on responsibility, decentralisation, integrity, and what it really means to “house all of finance” on chain. The $10 Billion Moment, and What It Meant When the HYPE token launched, roughly $1 billion was distributed to early users, and within months, that grew tenfold. Jeff describes it as something better than winning. “I think it’s rare that the people who are early to something can all participate in the upside and gain meaningful ownership over a network.” For him, the special part wasn’t the scale of wealth. It was the fairness of distribution. In a space often criticised for insider extraction, this felt like crypto working as it was originally intended. But the event didn’t fundamentally change how Hyperliquid operates. There was no hiring spree or culture change. The mission remained the same: build a neutral, high-performance financial protocol. Responsibility in Finance Isn’t Optional Jeff frames finance differently from consumer tech. “There’s inherently a lot of responsibility in building anything financial”. Users are trusting you with their capital, not just testing a product. That trust requires systems that are neutral, fair, and robust across market conditions. When you build financial infrastructure, scale isn’t what introduces responsibility. It was present from the beginning, and fundamentals like neutrality and transparency matter deeply when criticism comes. The “Buyback” Misunderstanding One of the loudest critiques aimed at Hyperliquid is that it “buys back” tokens daily and should adjust purchases based on price. Jeff’s response is blunt: the premise is wrong. “The main problem is that Hyperliquid does not have a discretionary buyback program”. Protocol fees are automatically converted and burned through on-chain logic. No human discretion or executive committee is timing the market. Why is that so important? “Because Hyperliquid is not a company”. It’s a rules-based protocol. Expecting discretionary buybacks misunderstands its design. The vision is to function like infrastructure, more like the internet than a bank. Small Team, High Integrity Perhaps the most surprising detail: Hyperliquid Labs operates with around 10–11 people. In an industry where protocols balloon into hundreds of contributors, Jeff prefers a concentrated group. “We select for people… who have this high integrity bar that we view as a non-negotiable”. Integrity is tested not through interviews alone but through working sessions where a full day is spent collaborating to see how someone actually operates. And hiring is consensus-driven. If someone has a strong objection, it’s usually a veto. The result is clear. Despite sudden wealth, no one has left. Jeff admits he expected some retirement, but instead, their motivation has intensified. The team didn’t particularly celebrate because the culture is built around creating value, not around financial extraction. Housing All of Finance Jeff often repeats the phrase “housing all of finance.” It doesn’t refer to becoming a mega-exchange. It means eliminating fragmentation. “The financial system should not be fragmented”. Today, your financial life is scattered across banks, brokerages, exchanges, and apps. Hyperliquid’s thesis is composability — one programmable, neutral layer where financial primitives plug into each other seamlessly. But the crypto twist is crucial: “The platform on which people do this should not be controlled by a central corporation”. Instead, multiple teams should build, everything should be composable, and no single entity controls access. HyperEVM, HIP-3, and Outcome Markets Much of Hyperliquid’s evolution revolves around primitives, which are core building blocks that shape how finance behaves onchain. HyperEVM is the first layer of that vision. It allows developers to deploy Ethereum-style smart contracts directly on Hyperliquid’s Layer 1. But more importantly, it lets those contracts tap into native liquidity and order book infrastructure, where execution, settlement, and liquidity are already integrated at the protocol level. HIP-3 pushes that philosophy further by allowing anyone to deploy permissionless perpetual futures. This creates a shift in the people who define market structure. The early traction in assets like silver — reaching meaningful global trading volume within months — demonstrates that specialised deployers, not just central exchanges, can drive price discovery when given the right primitives. HIP-4 introduces outcome markets: prediction markets, binary contracts, and bounded payoff structures. Fully collateralised and free from liquidation mechanics, they provide a cleaner way to express specific views without relying on leverage or funding mechanics. Across all three, the underlying principle remains consistent: keep the base layer minimal, neutral, and broadly useful. The protocol defines only what must be foundational. Everything else is built permissionlessly on top. Why Stay in Crypto? With AI attracting talent and capital, many question crypto’s future relevance. Jeff’s answer is simple: “If you don’t [bring finance on chain], then the financial system is going to fall behind the pace of technological development.” Legacy finance, he argues, cannot keep up with the speed of change, but programmable, decentralised infrastructure can. What Should Hyperliquid Be Remembered For? Jeff doesn’t want a legacy tied to a token event. “I hope Hyperliquid becomes the internet for money.” If Hyperliquid succeeds, users won’t think about it. They’ll simply use a financial system that is open, programmable, and neutral by default. 👉If you enjoyed reading the summary, head over to When Shift Happens on YouTube or your favorite podcast platform to access the full convo.

中文

@EvanWritesX @geekbb 这些1pass,bitwarden,proton pass等密码管理器都是开源项目经过多重审计,apple password,google密码管理,浏览器密码记录之流等于拱手送出密码和隐私,真敢用啊。

中文

知名密码管理工具 1Password 近日向用户发送邮件宣布,将于 2026年3月27日 起大幅上调其年度订阅费用,其中个人版计划的价格涨幅高达33%。

个人版 $35.88→$47.88 33%

家庭版 $59.88→$71.88 20%

听我的,赶紧在你的小鸡/NAS上部署体验一下 Vaultwarden,开启两步登录,你就知道之前的钱白花了!

github.com/dani-garcia/va…

中文

@Andrews39224778 @bboczeng 三、资本影响币价对交易员来说是好事,大涨大跌的大趋势赚钱更容易。而币24小时开市的特殊性,给短线选手更多的机会,消息消化更快,传统金融可能半年才有一次交易机会,币可能一个月就有了,况且玩美股每天休市总有跳空多难受。

中文

@Andrews39224778 @bboczeng 二、量子威胁从来不是虚拟货币的问题,是整个数字世界共同的问题,到时候银行的加密程度反而会先倒塌。加密世界也一直在为量子做准备,也有一种成果。

中文

再来说几句马后炮吧

币圈是真的没有任何价值了

以前,币圈之所以每隔4-5年能随着流动性炒作一波

确实是因为资金没地方去,得建一个赌场让散户们玩

而且交易所,也有以赌场为名囤积筹码的需要

所以币圈能以所谓ICO、铭文、NFT、DeFi为名,出现周期性繁荣,

但你回头看,这些所谓的“新技术”,有哪个落地的?有哪个有任何实际的价值?获得了任何实际的长期的用户?

就算有那么一点点人用,这些“新技术”的增长曲线,有人家ChatGPT创纪录的1年5亿的普及速度厉害?

币圈这些所谓去中心化的“技术”,比得上人家AI的一根D毛?

所以,如果说之前币圈每次死掉还有死而复活的希望的

AI时代,币会死的非常彻底

人类所有价值都会不断朝AI应用和硬件转移

连Solana稳定性都搞不定的币圈,就别来硬蹭了

好好的,安静的死去吧

希望这一次,能彻底一点

谢谢大家

中文

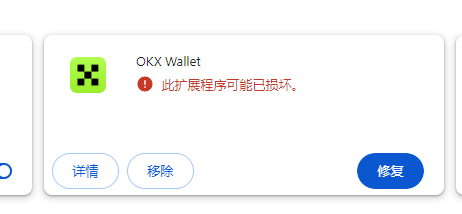

@love_doge123 @Mercy_okx @Haiteng_okx @mia_okx @Cryptosis9_OKX @Jiajia_OKX @Cayne_okx 11个助记词发给我,我帮你找回

中文

打开电脑第一天,懵逼了,OKX wallet 钱包损坏了,我现在害怕极了。这好好的怎么就坏了呢。

😂我有一个助记词单词记错了。提供11个能找回吗?

@Mercy_okx @Haiteng_okx @mia_okx @Cryptosis9_OKX @Jiajia_OKX @Cayne_okx

s开头的字母助记词有几个啊啊啊啊啊,我大概需要试多少次。应该是sp

中文

@Andrews39224778 @bboczeng 别人我都懒得回,但你说的我就回一下吧。我们两个说的不是同一个东西,我说的是中本聪设想的货币,不受政府管控是没法被人收走的意思,你也不要说打两棍就什么都交出来了,那属于是自己太高调找死。你说的币价受影响,这纯属人尽皆知的废话。有波动才好,一个稳定不动的货币根本没有生命力。

中文

这是我在币安、欧易、Bitget三家交易所的亲身经历,永远不要相信任何一家交易所,天下乌鸦一般黑,综合来说,币安稍微人性化一点,至少还能给你解决问题,其他交易所就不一定给你解决了。

也许你现在还没有经历过这些,等当你经历过了,你就知道你有多绝望了,叫天天不应,叫地地不灵。

老铁 Bro@LaoTieBro

真的建议所有人不要把资产放在交易所,风险太大了,你把币放在交易所,也许哪一天交易所就把你的账号封控了或者冻结你的资产,到时候后悔莫及,我说一下我在币安、欧易和Bitget三家交易所的经历。 2024年,欧易交易所突然把我账号封控了,禁止提现,我很少用欧易交易所交易,我实在不明白我哪里违规了,去问客服,客服也不说原因,直接让我提供各种资料,我一看这么麻烦,幸亏交易所里没放资金,一气之下,直接把欧易交易所注销了。 2025年,币安交易所突然封控我的账号,不能交易,但是可以提现资金,这点比欧易好,欧易是直接禁止提现,我去问币安客服什么原因,客服说是因为开VPN的原因导致的封控,然后给我解除封控了,这点效率挺快的。 还有Bitget交易所,2024年,我是BWB的大户,因为他们交易所要合并BGB和BWB,他们更过份,没有征求我的意见,直接冻结了我在交易所内部的BWB资产,不能交易,不能转账,很多人损失惨重,从此之后,我再也没有用过Bitget交易所了。

中文

真的建议所有人不要把资产放在交易所,风险太大了,你把币放在交易所,也许哪一天交易所就把你的账号封控了或者冻结你的资产,到时候后悔莫及,我说一下我在币安、欧易和Bitget三家交易所的经历。

2024年,欧易交易所突然把我账号封控了,禁止提现,我很少用欧易交易所交易,我实在不明白我哪里违规了,去问客服,客服也不说原因,直接让我提供各种资料,我一看这么麻烦,幸亏交易所里没放资金,一气之下,直接把欧易交易所注销了。

2025年,币安交易所突然封控我的账号,不能交易,但是可以提现资金,这点比欧易好,欧易是直接禁止提现,我去问币安客服什么原因,客服说是因为开VPN的原因导致的封控,然后给我解除封控了,这点效率挺快的。

还有Bitget交易所,2024年,我是BWB的大户,因为他们交易所要合并BGB和BWB,他们更过份,没有征求我的意见,直接冻结了我在交易所内部的BWB资产,不能交易,不能转账,很多人损失惨重,从此之后,我再也没有用过Bitget交易所了。

中文

火币甄选站全部解决了,不需要这么麻烦哦!

🏅0冻结+百分百赔付🏅时刻保护你的出入金安全💗

加密扶摇🔶 BNB@BTCfuyao

在“出金越来越难”的阶段,我找到了一条相对稳的 USDT 回国路径 在 𝕏 输出过不少教程,我最大的感受只有一句话: 真正困扰大家的,不是赚钱,而是钱怎么安全、合规地回到自己名下。 尤其是最近这段时间,临近春节,不少朋友私信我: “不走 C2C,还有没有别的办法?” “港卡拿不到,怎么处理加密资产?” 因为我比较特殊,身边很多朋友跑去棉被做诈诈,去境外的手续很难办,就一直搁置了,自己也属于无港卡、无离岸身份的状态,所以这段时间把能测试的路径都尝试跑了一遍。 最终结论是:LemFi 这条线,至少在当前阶段,值得单独拎出来讲一次。 为什么我会关注到 LemFi? 简单说一句背景结论: 👉 它不是“野路子”,而是正经跨境汇款公司。 成立时间:2020 年 覆盖国家:30+ 月交易规模:15 亿美元级 用户量:200 万+ 更关键的是: 它能和我们常用的一些“中转型金融账户”打通,最终落到支付宝 / 微信 / 银联。 从我自己的实测结果看: 1、汇损在同类平台里算低 2、中文区支持友好 3、出问题能在 App 里直接找到人工(这点很重要) 先说清楚一个前提:LemFi 对“环境一致性”要求非常高 如果你只看教程、不管环境,99% 会翻车。 所以这部分我放在最前面。 一、物理环境(这是硬条件) 必须满足三点: 1️⃣ IP 必须干净 禁用 VPN/机场 /纯净度低的代理节点 2️⃣ 推荐方案 英国实体 SIM 卡(如 giffgaff) 开启漫游流量 成本不高,但成功率极高 3️⃣ 手机号要求 只能用 +44 的英国号 ❌ Google Voice ❌ 接码平台 👉 一句话总结: IP、手机号、地址逻辑必须“像一个真实生活在英国的人”。 二、身份材料准备(不复杂,但要对) 证件:有效期内的中国护照 地址:不要求水电账单 但需要一个真实存在的英国住宅地址,且逻辑与 IP 匹配(可以生成) ⚠️ 地址不确定? Google Maps + 英国居民区即可,别乱编。 三、注册顺序很重要(影响权重 & 奖励) Step 1:下载 & 自检 关闭 Wi-Fi 使用英国 SIM 漫游流量 通过App Store / Google Play 安全渠道下载 LemFi 地区选择 United Kingdom Step 2:注册并锁定权益 输入英国手机号 设置强密码 邀请码填写:fuyao 权益包括: 首笔汇款 10% 返现(上限 £50),汇率点差优化,首笔免手续费 Step 3:KYC 邮箱验证 信息填写(与护照一致) 上传护照 + 人脸识别 ⏱️ 实测审核:几分钟级别 四、资金链路怎么走?分两类人 场景 A|已有法币,只做跨境 直接绑定银行卡 Apple Pay / Google Pay 成功率最高 风控极低 场景 B|USDT → 合规回国(重点) 这是我目前最认可的一条“非 C2C”路径: 交易所 → Kraken → iFAST → LemFi → 国内账户 1️⃣ USDT → 英镑 提现 USDT 到 Kraken 交易对:USDT / GBP 2️⃣ Kraken → iFAST 英镑转入 iFAST 这是你名下的正规银行账户 用来“切断交易所直接关系” 3️⃣ iFAST → LemFi LemFi 会给你一个同名的英国账户 底层银行:ClearBank 通过 FPS 同名转账 秒到、0 手续费、合规 100% ⚠️ 注意: 一定要 从 iFAST 主动转账,不要反向绑定扣款。 五、钱怎么回国内? 可选通道对比: 支付宝 / 微信(推荐) 到账:3–5 分钟 年度额度:约 50 万 RMB(视账户等级) 需提前开通对应功能 银联卡: 到账:10–30 分钟 受外汇额度限制 但风控最低,适合大额 六、一个真实存在的“负成本”案例 新人返现机制不是摆设,我实测过。 汇款金额:£500 交易成本:≈ £1 LemFi 手续费:£0 次日返现:£50 👉 实际结果: 完成一次出金 + 反而净赚 £49 七、几个高频问题直接说结论 Q:为什么不能用 VPN? A:ClearBank 风控极严,数据中心 IP 直接判死刑,住宅家宽可以豁免这种风险 Q:邀请码忘填了怎么办? A:基本补不了,只能注销重来,注册时务必填 fuyao Q:额度问题? LemFi:单笔 £10,000 / 月 £40,000 国内端:按外汇政策执行 最后一句实话 这条路径也许并非永远有效, 但在当前阶段,它是我实测下来相对稳定、逻辑清晰、合规性最高的一条。 如果你正好有: USDT 需要变现 不想碰 C2C 又拿不到港卡 那至少,值得你认真看一遍、低额实测一次。 #海外收款 #LemFi

中文