Asad Khan retweetledi

Asad Khan

3.1K posts

@FinTech_Khan

Advisor @ Wu Tang Financial. I've worked in DeFi and Central Banking and I have no respect for any of you. #keeppounding

Iran has more than 40 million men fit for military service, all of whom have been conscripted, trained and served in the armed services for 21 months. Some 1.4 million men reach military age per annum. For reference, Vietnam had no more than 10 million men of military age in 1965. US commitment of ground forces peaked at a half a million men. US armed strength was 1.88 million, 3X larger than 0.62 million today. Even if the US could field enough divisions in Iran, which it assuredly cannot (see rt), there is just no possibility of winning a counterinsurgency war in Iran. None. Zero. Nada. Not only is defeat certain if the US commits ground forces to occupy Iran, it will chew up the American army. It’s going to make Vietnam look like a cake walk. Can’t remember the name of the Substack author who wrote that any serious war will consume the American military and basically put it out of business for a decade. If the US commits large-scale ground forces to Iran, that wager becomes a near certainty.

Here is why the Kharg idea cannot work, @yarotrof. Suppose you land a marine division on the island. They will come under immediate and sustained fire; not just with missiles and drones but even artillery. The casualties will mount rapidly and the force will have to be evacuated in days. Suppose that somehow the marines manage through heavy missile defense and air defense and fire suppression to stay put. That still does not reopen Hormuz at all. Kharg is very far from Hormuz. So, even if it works, which is highly unlikely, it is a nonsolution to the problem of neutralizing the Hormuz weapon. There is only one possible military solution, and that is to win the interdiction war and degrade Iran’s ability to launch missiles and drones, and mine Hormuz. The problem is that the interdiction war is almost certainly unwinnable in any tolerable timeframe. See also x.com/policytensor/s….

DUNE PART THREE

Sorry to be the downer because this is an impressive story in some senses. But it is ~trivially easy to make a single mRNA vaccine. It's not hard. I cure mice of various cancers with various therapeutics all the time. I've made mice lose more weight in a month than tirzepatide does in a year. What is hard and expensive is proving its BOTH safe AND effective **in a randomized and controlled study in humans** while ALSO manufacturing it at clinical scale and grade. I am happy for this man and his dog. It is impressive. But y'all are overhyping it.

@lilrocketnasa When this dude comes back to Charlotte angry we'll all feel it. He looks better on tape than in the statbook but he had some good games too

The #Bucs are signing former #Panthers standout DL A'Shawn Robinson to a 1-year, $10M fully guaranteed deal, per The Insiders. A raise after he was due to make $8.5M with Carolina. Robinson's deal was done by agents Sean Kiernan and Travis Allen of @AthletesFirst.

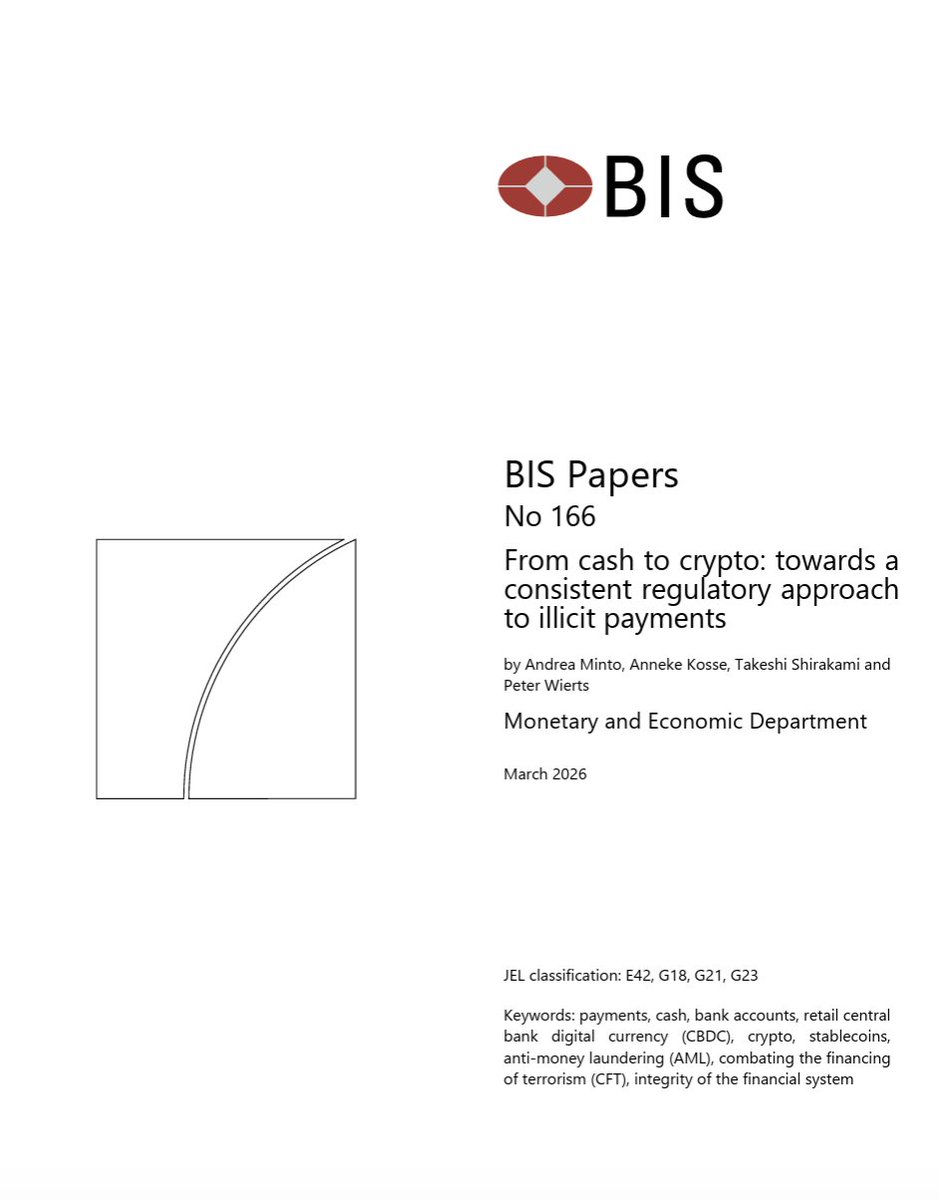

🔴The Bank of International Settlements (BIS) has published a new research paper on illicit finance in "self-hosted" cryptocurrencies. The researchers find that "self-hosted" cryptocurrencies may be used by illicit actors, arguing for both holistic and targeted frameworks to combat illicit finance in peer-to-peer transactions. Notably, the researchers appear to base their call for increased regulation on hypotheticals rather than factual data, such as the ease of transactions in peer-to-peer cryptocurrency transactions vs. cash.

man i hope they build around “bryce” instead of getting an edge and a LB 😂

ESPN sources: former Buccaneers six-time Pro-Bowl WR Mike Evans is expected to sign a three-year deal with the San Francisco 49ers.

A community bank isn't just a smaller version of a big bank. It's the lender who knew your grandfather, who called you back within a day, who made a judgment call when your financials weren't perfect but your character was. Preserving that model isn't nostalgia — it's smart policy.