Gavin retweetledi

Gavin

81 posts

Gavin

@GavinPHC21

Yadon lover (photo credit: Currymochimochi)

Katılım Ağustos 2020

83 Takip Edilen5 Takipçiler

Gavin retweetledi

処方薬として出されるヤドンやぁ~ん‼️

薬剤師「疲れから来ているのでしょう。ヤドンを観てゆっくり休んで下さい。」AI作

日本語

Gavin retweetledi

Gavin retweetledi

ヤドン電車が話題になった頃

お題にもたくさん来てたので

頑張ったのですけど

内装がもう大変すぎて

ギブアップしてしまった😂

拾いものの画像に描き加えてみました。

日本語

Gavin retweetledi

Gavin retweetledi

Gavin retweetledi

Gavin retweetledi

Gavin retweetledi

Gavin retweetledi

Gavin retweetledi

㊗️ポケモン30周年おめでとう㊗️

ポケモン30周年お祝いして、ちまっとしたポケモン×30のイラスト描いてみたよ🎨

#ポケモン30周年 #ポケモンデー

👇🏻リプ欄に単体イラストも載せときます👇🏻

日本語

Gavin retweetledi

Gavin retweetledi

Gavin retweetledi

SOCAMM戰線擴大:NVIDIA領頭,Qualcomm與AMD跟進

被譽為「第二個HBM」的SOCAMM(Small Outline Compression Attached Memory Module)正快速成為AI伺服器記憶體新趨勢。全球半導體龍頭NVIDIA率先將SOCAMM第二代(SOCAMM 2)搭載於自家伺服器CPU「Vera」旁邊,打破傳統板載DRAM的限制。

SOCAMM的核心優勢在於將4顆LPDDR DRAM晶片模組化,底部增加基板以擴大資料傳輸通道,提升速度;同時支援可拆卸設計,延長伺服器壽命,兼顧效能與維護性,被視為AI時代關鍵記憶體形態。

繼NVIDIA之後,Qualcomm正檢視SOCAMM供應鏈,計畫用於即將推出的AI伺服器晶片AI200與AI250,正式向NVIDIA發起挑戰。AMD也已與三星等記憶體廠商交換試作品,積極評估導入。值得注意的是,Qualcomm與AMD傾向採用「正方形」配置(DRAM兩列排列),有望在基板上整合電源管理晶片(PMIC),與NVIDIA的長方形單列設計有所差異。

目前SOCAMM尚未由JEDEC訂定明確標準,若Qualcomm與AMD陣營推動自家形狀的標準化,未來產業可能出現分歧局面。

隨著採用廠商增加,SOCAMM原料LPDDR DRAM供應壓力劇增。三星電子已接下NVIDIA今年200億Gb SOCAMM 2訂單中的一半,並同步擴大1b製程產能以因應需求。SK海力士與Micron同樣面臨產能調配挑戰。LPDDR供不應求已導致行動裝置領域缺貨、價格急漲,部分IT廠商甚至考慮降規或移除零件。

SOCAMM的崛起不僅加速AI伺服器記憶體革新,也讓LPDDR從手機主戰場延伸至資料中心,供應鏈緊繃態勢短期難解,預料將進一步推升相關晶片與終端產品成本。

포시포시@harukaze5719

Qualcomm and AMD also plan to adopt SOCAMM2. Qualcomm is reviewing the SOCAMM supply chain. AMD is receiving and reviewing SOCAMM prototypes. hankyung.com/article/202601…

中文

記憶體市場進入賣方主導階段,AI需求推動上漲周期

1. 市場概況與周期階段

- AI引發的需求浪潮重塑全球記憶體(DRAM與NAND快閃記憶體)市場,目前處於強勁上漲周期的早期至中期階段。

- 儘管股價已創歷史新高,但報告認為漲勢最佳階段尚未到來,投資人勿因「高峰恐慌」(peak fears)過早離場。新高通常帶來更高高點,且有足夠獲利支撐,「留在市場」比「擇時」更重要。

2. 供需失衡與賣方市場轉變

- 受美國雲端服務客戶訂單激增影響,記憶體晶片廠商對2025年第4季DRAM與NAND報價上漲高達25%,市場快速轉向賣方主導。

- 供應短缺惡化:DRAM供應商庫存急劇降至不到2週;NAND快閃記憶體庫存回落到長期平均水準以下。

- 新產能需4-6季才能追上需求,供應延遲持續,客戶傾向囤積緩衝庫存,進一步強化賣方結構。

- 報告預期:2026年第1季季節性需求疲軟不會影響記憶體價格。

3. 價格上漲潛力

- NAND快閃記憶體:AI需求強勁,價格預計從當前水準翻倍,回升至2022年第2季高峰的0.13美元/GB。

-DRAM記憶體:伺服器模組價格目前為5.4美元/GB,過去高峰為2018年第1季的10美元/GB。考慮AI記憶體總可及市場(TAM)預計2027年超越傳統DRAM市場,本周期高峰有基礎超越以往。

4. 股價驅動因素:獲利動能而非AI敘事

- 「高峰恐慌」為典型認知偏差。股價上漲依賴獲利預測上修,而非僅AI概念。

- 範例:

· SK海力士(SK Hynix):過去12個月股價漲140%,獲利預測上修62%。

· 三星電子(Samsung Electronics):股價漲64%,獲利預測上修僅14%。

- 歷史周期顯示,上漲期中「市場時間」(time in the market)比擇時更關鍵。

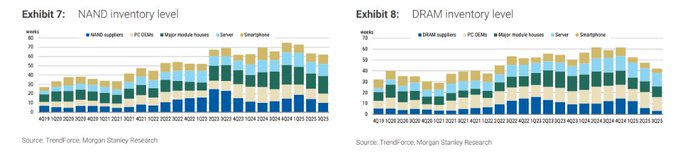

5. 圖表分析(Exhibit 7 & 8:庫存水準,單位:週)

- Exhibit 7:NAND庫存水準

趨勢:2019Q4至2025Q2,庫存波動劇烈,早年高達70週以上,近期(2024Q2起)急降至20週以下,供應商與模組廠庫存最低,顯示短缺加劇。

- Exhibit 8:DRAM庫存水準

趨勢:類似NAND,早年高峰近70週,2024年起崩跌,供應商庫存降至10週內,伺服器與模組廠亦低於20週,確認賣方市場形成。

Jukan@jukan05

Surging demand, depleted inventories, memory is already a “seller’s market”… Morgan Stanley: investors shouldn’t exit on “peak fears” The demand wave triggered by AI is reshaping the global memory market. On October 19, Morgan Stanley noted in its latest report that the memory (storage) sector is in the early to middle stages of a strong up-cycle, and that even though related share prices have hit record highs, the “best” part of the rally may still lie ahead—so investors should not leave the market too early due to “peak fears.” Worsening supply shortage, shifting to a seller’s market Through channel checks, Morgan Stanley found that, aided by a surge in orders from U.S. cloud service customers, memory chip makers are quoting price hikes of up to 25% for DRAM and NAND flash for the fourth quarter of 2025. This shows the market is rapidly tilting toward the seller and that the momentum for price increases is strong. The report emphasized that the supply-demand imbalance in commodity memory is more severe than expected. DRAM vendors’ inventories have fallen sharply to less than two weeks, and NAND flash inventories have also returned to below their long-term average levels. The firm expects it will still take 4–6 quarters for new capacity to catch up with demand, and that supply delays will persist. Such an environment typically prompts customers to build buffer inventory, further solidifying the seller’s-market structure. “We believe the current rally is still in the early to middle stages… A return of prices to historical peaks would imply ‘double’ the potential from here. We have seen no evidence that seasonal demand softness will affect memory pricing for the first quarter of 2026… Such conditions typically lead customers to build buffer inventories, thereby strengthening the seller’s market.” How much further can prices rise? Morgan Stanley: still a “long way” from the peak Morgan Stanley believes current prices still have considerable upside before reaching historical highs. NAND flash: Given strong AI-led demand, prices are expected to “double” from current levels and return to the peak of about $0.13/GB seen in the second quarter of 2022. DRAM memory: Server memory module prices peaked at $10/GB in the first quarter of 2018, while current negotiated prices are about $5.4/GB. Considering that the potential total addressable market (TAM) for AI memory is expected to surpass that of the traditional commodity DRAM market by 2027, the report sees “sufficient grounds” for the price peak in this cycle to exceed the past. Move beyond “peak fears,” the key is “earnings momentum” Regarding the widely prevalent “peak fears” among investors, Morgan Stanley asserts this is a classic cognitive bias. “New highs usually call for higher highs, and this time there are sufficient earnings to support them; ‘staying in the market’ is more important than timing the market. The best phase of this rally is likely still ahead.” The report stresses that what drives stock prices is not merely the AI narrative but “earnings momentum.” Taking SK hynix and Samsung Electronics as examples, SK hynix’s share price has risen about 140% over the past 12 months, underpinned by a 62% upward revision in earnings forecasts; by contrast, Samsung Electronics’ share price rose only about 64%, with earnings forecasts raised by just 14%. This difference clearly shows that “stronger earnings upgrades deliver stronger share-price returns.” Analysts Shawn Kim and Duan Liu wrote in the report that it is almost impossible to time the market precisely, and that historical cycles show that during upswings, “time in the market” matters more than “timing the market.”

中文

@QQ_Timmy 參考的是技嘉有提到部分產品能夠透過在擴充插槽安裝DPU,額外支援更多的SSD。

gigabyte.com/tw/Article/how…

不過NV的DPU一直停留在BF3,遲遲不出BF4,不知道會不會也影響到採用意願。🤔

中文

1. 報告大意:AI 來了,NAND 要起飛NAND 是什麼? NAND 是手機、電腦、雲端伺服器用的儲存晶片,像硬碟但更快、更省電。

AI 怎麼幫 NAND? AI 需要超多資料儲存,尤其是「推理」(AI 思考答案)階段。傳統硬碟(HDD)太慢,NAND 做的固態硬碟(SSD)最適合。

市場預測: 到 2029 年,AI 相關 NAND 市場會多出 290 億美元,佔整個 NAND 市場的 34%。這就像 AI 給 NAND 打了一針強心劑。

短缺來了: 從 2026 年下半年,NAND 可能供給短缺 2%(基本預測)。如果 SSD 取代更多 HDD,短缺可能達 8%(樂觀預測)。原因是雲端公司(如 Google、Amazon)大買 NAND 給 AI 伺服器。

2. 為什麼現在起飛?3 個簡單原因需求爆發: AI 訓練和推理需要隨機存取資料,QLC 型 NAND SSD 最快、最適合。雲端公司已在談 2026 年大訂單。

創新產品: 近線 SSD(NL SSD):新款 SSD 成本低,2025 年底推出,可能取代 HDD(硬碟),讓 NAND 用量大增。

高頻寬閃存(HBF):像 SanDisk 的新技術,能取代部分記憶體(DRAM),解決 AI 記憶體瓶頸,2027 年上市。

週期變好: NAND 從 2022 年過剩(太多貨),現在庫存清光,2026 年轉平衡。消費者需求弱(手機、PC 賣不好),但 AI 補上, downturn(衰退)不會太深。

3. 投資建議:NAND 供應商: SanDisk(美國,最頂級推薦)、KIOXIA(日本)、Samsung Electronics(韓國)。他們直接做晶片,最賺。

模組廠: 群聯Phison、Longsys(中國)。NAND 漲價時,他們跟著賺。

元件廠: 慧榮SIMO、信驊Aspeed。AI 伺服器需要他們的控制器(大腦零件)。

設備廠: Advantest、Disco(日本)。幫做高階 NAND。

硬碟相關: WDC(Western Digital,頂級推薦)、STX(Seagate)。AI 資料多,HDD 和 SSD 都受益。

小心點的(Equal-Weight 或 Underweight):Micron、SK hynix(HBM 利潤問題)、Pure Storage(等 Meta 訂單)、Lam Research(中國管制影響)。

為什麼這些好? 大摩預測 2026 年這些公司的 EPS(每股獲利)比市場平均高 26%,市場還沒發現 AI NAND 的潛力。HDD 股票今年已漲很多。

4. 風險與樂觀樂觀情境: AI 部署快 + SSD 取代 HDD = NAND 大短缺,價格漲。

悲觀情境: 沒 AI 需求 = 供給過剩 10%,價格跌。

估值低: SanDisk 等股票現在便宜(1 倍本益比),有上漲空間。

HDD vs SSD: HDD 成本低 6-8 倍,短期還穩,但 AI 資料多,兩者都贏。

5. 市場圖表: 報告有圖示 NAND 短缺、收益修訂、風險回報。HDD 今年表現最好。

中文