Philipp Gilg

11 posts

Forrester: 🧐

"Wir gehen davon aus, dass die Hälfte der auf KI zurückgeführten Entlassungen stillschweigend rückgängig gemacht wird, wobei diese Stellen ins Ausland verlagert oder zu niedrigeren Löhnen zurückkehren.

Das AI-Washing und die Fata Morgana einer zukünftigen KI kollidieren mit der betrieblichen Realität. Viele Unternehmen erkennen derzeit, dass das Ersetzen von Menschen durch Maschinen nicht immer billiger oder klüger ist, es sei denn, man verfolgt einen ganzheitlichen Ansatz, der die Menschen berücksichtigt, von denen jeder KI-Erfolg letztlich abhängt."

Forrester Research ist eines der weltweit einflussreichsten Marktforschungs- und Beratungsunternehmen im Technologiebereich, neben Gartner und IDC.

Ahja und alle drei sind sich quasi einig, dass KI im Kern als Werkzeug und nicht als autonomer Ersatz für das gesamte Unternehmen betrachtet werden sollte.

forrester.com/blogs/future-o…

Deutsch

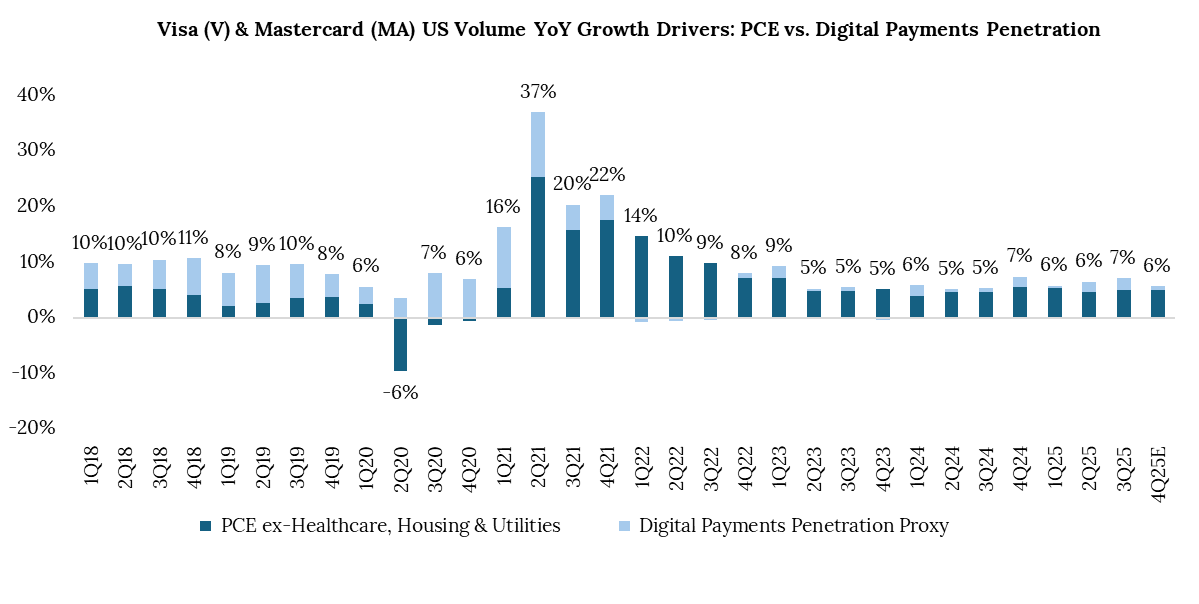

If you think about $V and $MA long-term volume growth drivers, it’s been a combination of personal consumption expenditures (PCE) — or the amount consumers are spending on goods and services regardless of what payment instrument they’re using — and digital payments penetration increasing — or the increasing number of consumers using digital/card payments versus cash or check (or a cardholder who already has a card using it for a higher percentage of their purchases over time).

For a long time, $V / $MA volume growth was more evenly split between end market / PCE growth and increasing digital penetration. This allowed them to sustain higher than industry growth (ie PCE) — typically ~2x that rate — and allowed both to maintain a certain level of growth in cyclical downturns (PCE falls but digital penetration gains carry more weight so they still grow) but given growth has converged more to PCE growth and digital penetration is going to be less of a driver moving forward, $V / $MA volume growth will more closely reflect PCE, which means it’ll be more heavily tied to macro economic up/down cycles — and generally, will grow slower going forward assuming PCE remains ~stable.

I hope this helps.

English

Interesting to decompose $V & $MA US volume growth into PCE growth and digital payments penetration gains (calculated by subtracting adj. PCE growth from $V & $MA growth). I adjusted PCE to exclude healthcare, housing & utilities since these are mostly non-addressable for typical consumer card payments.

In the few years leading up to Covid, digital payments penetration accounted for ~57% of $V & $MA's US growth. Since 2022, it's <10%.

At $V's Feb 2025 investor day, it stated US penetration was 60%+ (my rough math puts it 75%+). This demonstrates that $V & $MA US growth is mostly a PCE proxy now.

English

Has Claude dig into 5 years’ worth of acquisitions for $CSU.TO , $TOI.V , $LMN.V to assess AI disruption impact across $8Bn of acquisitions

English

Chris Hohn on why Aerospace sits firmly in his investable universe:

“Aerospace is a sector we’ve come to understand where the barriers to entry are multiple… hard assets, contracts, network effects… intellectual property, contracts, installed base, regulatory switching costs.”

___

𝐓𝐡𝐞 𝐥𝐞𝐬𝐬𝐨𝐧:

𝙏𝙝𝙚 𝙢𝙤𝙨𝙩 𝙙𝙪𝙧𝙖𝙗𝙡𝙚 𝙗𝙪𝙨𝙞𝙣𝙚𝙨𝙨𝙚𝙨 𝙙𝙤𝙣’𝙩 𝙧𝙚𝙡𝙮 𝙤𝙣 𝙤𝙣𝙚 𝙢𝙤𝙖𝙩 — 𝙩𝙝𝙚𝙮 𝙨𝙩𝙖𝙘𝙠 𝙢𝙪𝙡𝙩𝙞𝙥𝙡𝙚 𝙗𝙖𝙧𝙧𝙞𝙚𝙧𝙨 𝙩𝙤 𝙚𝙣𝙩𝙧𝙮. 𝙀𝙖𝙘𝙝 𝙡𝙖𝙮𝙚𝙧 𝙢𝙖𝙠𝙚𝙨 𝙙𝙞𝙨𝙧𝙪𝙥𝙩𝙞𝙤𝙣 𝙝𝙖𝙧𝙙𝙚𝙧; 𝙩𝙤𝙜𝙚𝙩𝙝𝙚𝙧, 𝙩𝙝𝙚𝙮 𝙘𝙧𝙚𝙖𝙩𝙚 𝙣𝙚𝙖𝙧-𝙞𝙢𝙢𝙪𝙣𝙞𝙩𝙮.

___

Why multiple barriers matter:

𝐇𝐚𝐫𝐝 𝐚𝐬𝐬𝐞𝐭𝐬 → capital intensity discourages new entrants

𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐬 → long-dated agreements with OEMs & airlines

𝐍𝐞𝐭𝐰𝐨𝐫𝐤 𝐞𝐟𝐟𝐞𝐜𝐭𝐬 → scale advantages in service, parts, and support

𝐈𝐧𝐭𝐞𝐥𝐥𝐞𝐜𝐭𝐮𝐚𝐥 𝐩𝐫𝐨𝐩𝐞𝐫𝐭𝐲 → decades of engineering know-how that can’t be replicated quickly

𝐈𝐧𝐬𝐭𝐚𝐥𝐥𝐞𝐝 𝐛𝐚𝐬𝐞 → once equipment is flying, customers can’t easily switch

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐢𝐨𝐧 & 𝐜𝐞𝐫𝐭𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧 → enormous time, cost, and risk to gain approval

𝐒𝐰𝐢𝐭𝐜𝐡𝐢𝐧𝐠 𝐜𝐨𝐬𝐭𝐬 → safety, reliability, and downtime risks deter change

𝐄𝐚𝐜𝐡 𝐥𝐚𝐲𝐞𝐫 𝐦𝐚𝐤𝐞𝐬 𝐝𝐢𝐬𝐫𝐮𝐩𝐭𝐢𝐨𝐧 𝐡𝐚𝐫𝐝𝐞𝐫.

___

5 High-Quality Aerospace businesses worth adding to your watchlist:

1. $GE GE Aerospace

3-Year CAGR: +58%

2. $HWM Howmet Aerospace

3-Year CAGR: +76%

3. $TDG TransDigm Group

3-Year CAGR: +20%

4. $HEI Heico

3-Year CAGR: +23%

5. $RTX RTX Corporation

3-Year CAGR: +27%

When investors talk about “disruption risk,” sectors with layered moats like aerospace are often underestimated. Patience — and respect for barriers — tends to be rewarded.

___

Video: Norges Bank Investment Mangement | Investment Conference 2025 (07/23/2025)

English

Jensen Huang: Market is wrong about software stocks

"The notion that AI is somehow going to replace software companies is the most illogical thing in the world and time will prove itself"

Interview date: 3 February 2026

English

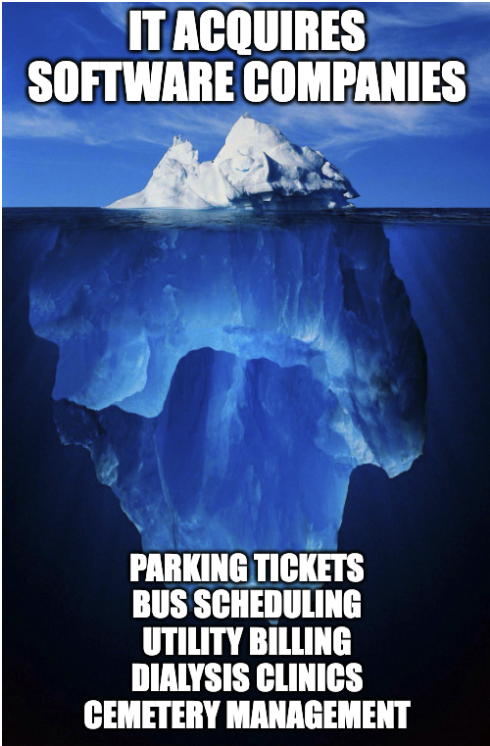

Mark Leonard didn't stumble into boring. He chose it.

Every business Constellation Software owns has three characteristics:

(1)Too small for big tech to care

(2)Too complex for startups to figure out

(3)Too embedded for customers to switch

Here's what $CSU actually owns

1) GOVERNMENT & PUBLIC SECTOR

Harris Local Government serves 5,500+ municipalities across the US with fund accounting, payroll, permitting, and tax software.

SirsiDynix provides library management systems to thousands of libraries worldwide.

AI Risk: Very Low

Government procurement takes years. They're still running software from 2008.

2/ HEALTHCARE

Constellation Kidney Group provides dialysis clinic software globally, celebrating 50 years of nephrology technology innovation in 2025.

Switching costs are massive

-Years of patient records

-Lab equipment integrations

-Staff trained on the system

-CMS compliance validation

-Billing codes mapped

Computrition handles hospital foodservice management: tracking every patient meal, dietary restriction, and nutrition requirement.

AI Risk: Low

HIPAA. FDA. CMS. No one experiments with patient data.

3/ PUBLIC TRANSIT

Trapeze Group powers 250,000 scheduled trips per day across North America, supporting 1.7 million registered riders using 14,000+ vehicles.

They handle bus scheduling, route planning and the real time arrival info on your phone.

AI Risk: Low

ADA compliance is law. Union contracts are encoded in the software.

4/ HOSPITALITY & CLUBS

Jonas Club Software serves 2,300+ golf, country, and yacht clubs across 20 countries.

Springer-Miller Systems provides property management for luxury hotels and resorts, clients include Pebble Beach.

AI Risk: Medium

A bit more fragmented with already multiple players in the spaces. This could be at higher risk but still has change management and switching costs

5/ UTILITIES

Harris Utilities provides billing systems for water, electric, and gas companies.

Rate structures are insanely complex time-of-use, tiered, seasonal, demand charges, all integrated with physical meters.

AI Risk: Very Low

No utility executive risks a billing disaster for "innovation."

6/ NICHE INDUSTRIAL

Vela Software focuses on oil & gas, manufacturing, and industrial verticals.

Marina management. Steel inventory by grade and gauge. Grain elevator operations.

AI Risk: Low

What am I missing?

English

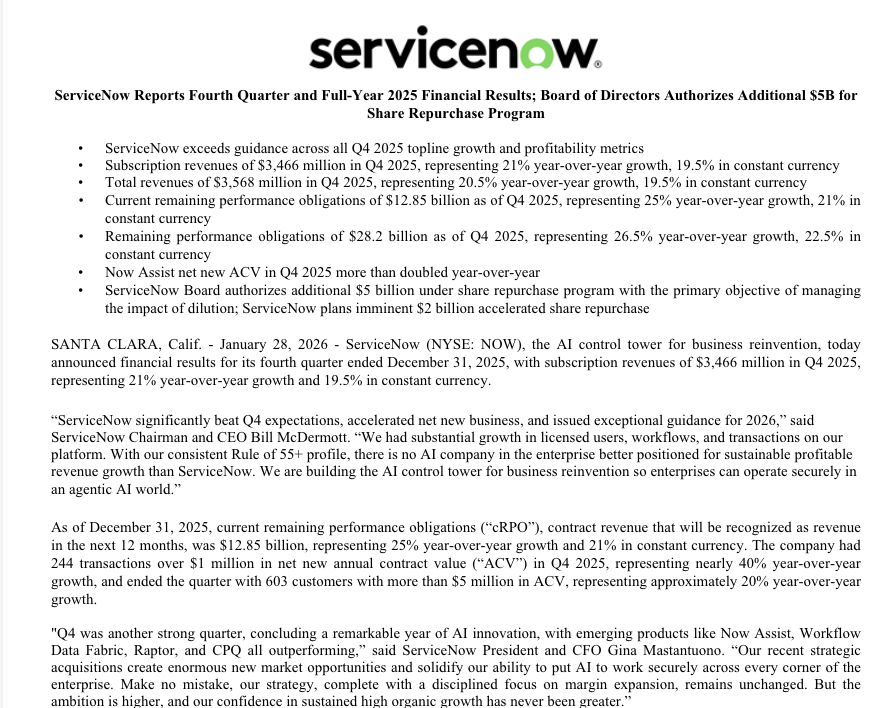

ServiceNow CEO: "ServiceNow significantly beat Q4 expectations, accelerated net new business, and issued exceptional guidance for 2026. We had substantial growth in licensed users, workflows, and transactions on our platform."

$NOW: -5% AH

English