Sabitlenmiş Tweet

@hodloncomrades @boomer_btc @PrestonPysh I'm thinking #Podcats is a cool name for premier podcast hosts like @PrestonPysh #SortOfLikeHoldAndHodl

English

Give A Little Bit(coin)

7K posts

@GiveALittleBit3

A little Bit of this, a little Bit of that #BTC npub1ej68v9kkzzrckeu4c839fey2zsmmv2axfe0hfypsqqmumv2h6ueqf96yzv

As I fly out of another trip to Canada, this time Toronto, I just feel compelled to say how shocking it is that so many people have to recognize that Canada is likely already beyond repair on so many issues. They see the train running towards a cliff, and there are no brakes.

BOMBSHELL EXPOSÉ: BLACK LIVES MATTER “Executive Director” Tashella Sheri Amore Dickerson was CHARGED for EMBEZZLING $3.15 MILLION into her PERSONAL ACCOUNT. She used them to buy six properties, a car, for shopping, and $50,000 in food deliveries.

La vidéo de la presse chinoise montrant l’explosion du meeting privé présidé par @netanyahu qui indique sa probable mort à d’abord été interdit du @X aux États Unis et vient d’être interdit sur @XFrance et Europe ! Jusqu’à Quand nos dirigeants vont continuer à nous mentir?

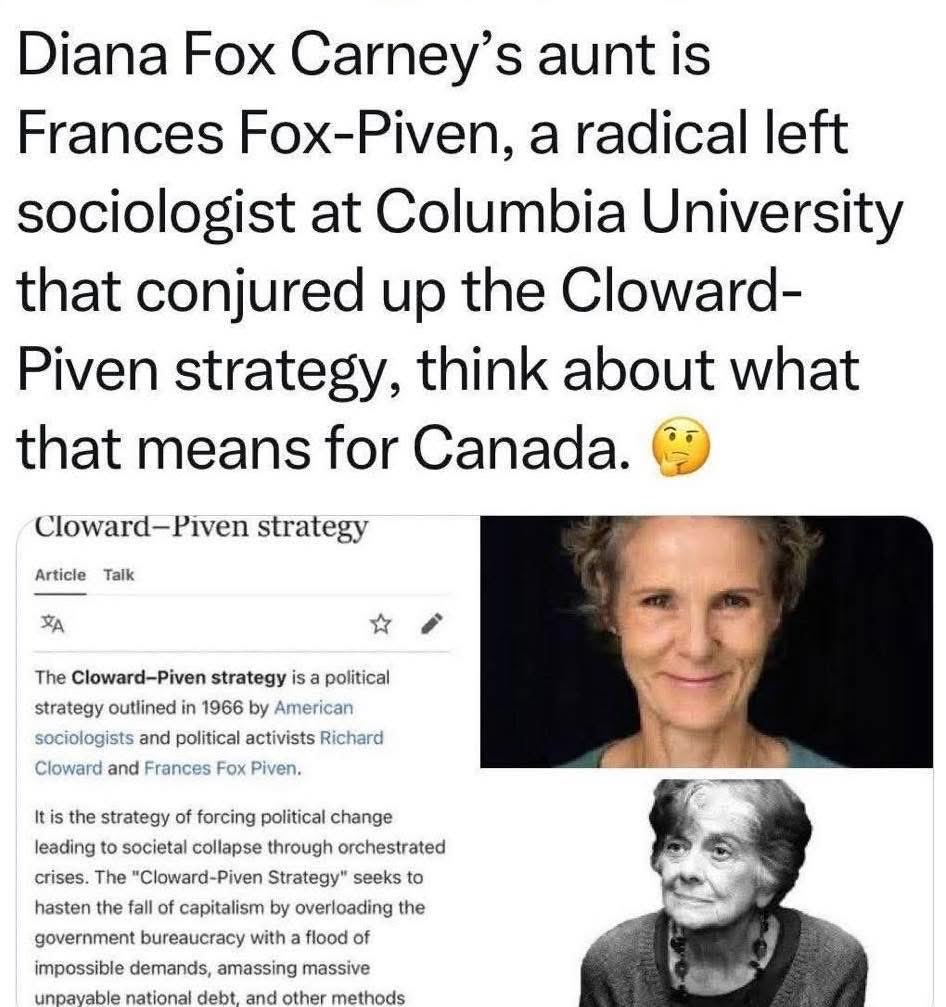

I don't think we have any idea how intertwined Brookfield is within the Government of Canada In one accounting book alone they received over $500 million from the Liberal Govt I have three more accounting books to go through

I discuss $BTC price action, the rise of Digital Money and Digital Credit like $STRC, debunk the latest quantum FUD, and explain why companies like $MSTR are accelerating global Bitcoin adoption with @NatBrunell.

In August, President Trump signed an executive order titled "Democratizing Access to Alternative Assets for 401(k) Investors." The order directs regulators to make it easier for your retirement savings to flow into private credit, private equity, and other "alternative" assets. The Department of Labor quickly rescinded Biden-era guidance that had discouraged these investments in retirement plans. Apollo. Blackstone. Goldman Sachs. State Street. They're all racing to launch private credit products for your 401(k). But here's the problem: Private credit is showing cracks at the exact moment they want to open it up to retail investors. Just this week, BlackRock TCP Capital - one of the largest publicly traded private credit funds - plunged 17% after disclosing a 19% writedown on its net asset value. The biggest drop in almost six years. This is BlackRock. The world's largest asset manager. $14T in assets. If they're taking hits like this, what chance does your 401k have? Let me walk you through what's actually happening in this market... Private credit has ballooned to over $2T in assets. For years, it was the domain of sophisticated institutional investors - pension funds, endowments, insurance companies. These investors have teams of analysts, lawyers, and risk managers to evaluate complex deals. Your average 401k participant doesn't have any of that. And the timing couldn't be worse. The IMF's 2025 Financial Stability Report found that 40% of private credit borrowers now have NEGATIVE free cash flow. That's up from 25% in 2021. Goldman Sachs data shows 15% of borrowers can no longer generate enough cash to fully cover their interest payments. UBS forecasts that private credit defaults could climb by 3 percentage points in 2026 - outpacing leveraged loans and high-yield bonds. Meanwhile, payment-in-kind loans - where struggling borrowers defer interest by adding it to their debt balance - have surged from 7.4% in 2021 to over 11% today. When a company can't pay interest in cash, that's not a sign of health. It's a sign of stress being disguised. Then came September's wake-up call: Auto parts maker First Brands collapsed with $8B in off-balance-sheet financing that wasn't properly disclosed to lenders. Subprime auto lender Tricolor imploded amid allegations it pledged the same loans as collateral to multiple creditors. Both received clean audits shortly before they cratered. First Brands' term loans went from 90 cents on the dollar to under 15 cents in weeks. JPMorgan's Jamie Dimon put it bluntly: "When you see one cockroach, there are probably more." Here's what makes this dangerous: Private credit is lightly regulated, less transparent, and difficult to value accurately. The managers making the loans are often the same ones valuing them. They have every incentive to delay recognizing problems. The DOJ has already issued warnings about "creative" marks and questionable valuation practices. Banks aren't insulated either. They've lent over $2.2T to non-bank financial institutions. When problems surface in private credit, banks feel it too. And now they want to put this in YOUR retirement account. The pitch is that private credit offers "higher returns" and "diversification." But the data doesn't support the sales pitch: Recent research shows pension funds increasing exposure to private markets have actually seen depressed returns compared to simple stock and bond portfolios. The 50 largest US pension funds averaged just 7.4% returns over the past decade. A basic 60/40 portfolio beat many of them. The real beneficiaries are fund managers charging 2% fees on assets that can't be easily valued or sold. My view really hasn't changed: AVOID PRIVATE CREDIT When sophisticated institutional investors start pulling back - and they are - the last thing you want to do is rush in. Stay in liquid, transparent, low-cost investments for your retirement. Don't be the exit liquidity.

“This will keep Canadians safe…” -Minister Lena Diab Canada launches a new ‘Immigration Category’ for the Armed Forces to allow ‘Recruits’ from the Chinese Communist Party and other foreign adversaries to merge with Canada’s Military. THIS IS TREASON. WE ARE UNDER ATTACK.