@shortsqueeznews do you always rip off the day's newspaper stories without attribution?

English

buddy garrity search fund

867 posts

@Goulderbilt

I'll buy as many shitcos as has you have, right now, at 3x. Sell me all you want.

Goldman Sachs hired this 16-year-old trader and gave him $10M to manage in his first week - then he then took his strategy to JP Morgan and Lehman Brothers, before retiring and going to space (really) 11-min workshop from a tier-1 trader with the story of his strategy it's the most honest trader interview about the truth of Wall Street you'll ever find

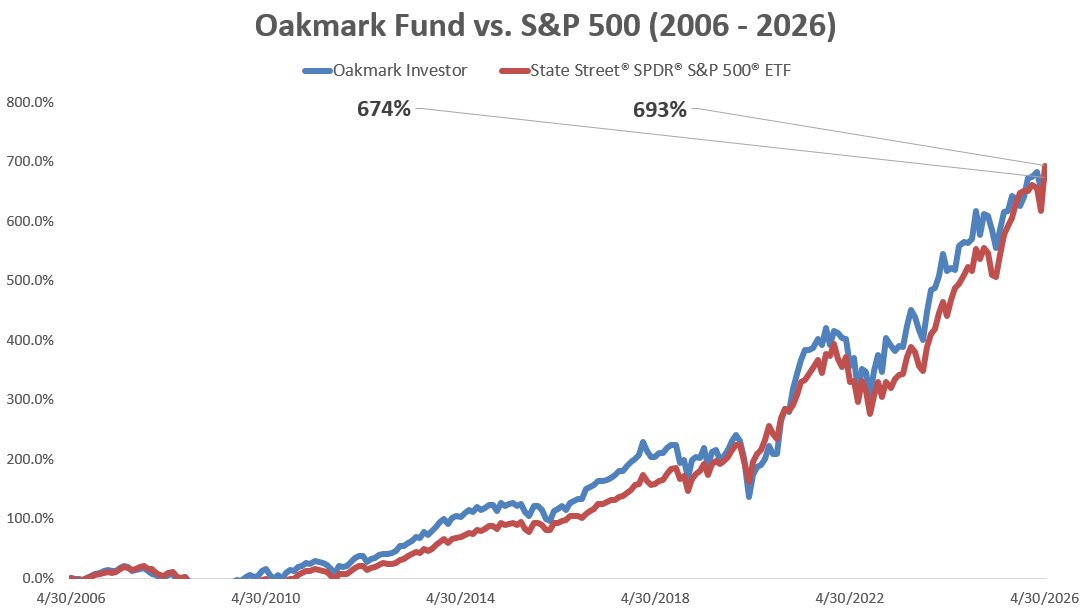

Bill Nygren quarterly letter: “Why didn’t we do better when value outperformed?” Nobody has excuses like the active mgmt. fund complex: Past 10 years: we need more dispersion! Last quarter: we need less dispersion than we got! Full letter: oakmark.com/news-insights/…

Akre Capital selling V MA and MCO to buy ROP FICO CRM and NOW. Dunno man…

The “prestige” professions of finance, tech, law etc are only available in high cost metros where you barely keep up with neighbors. The real arb is being a doctor or SMB owner in a random suburb where you can be the richest guy in the Costco parking lot