Sabitlenmiş Tweet

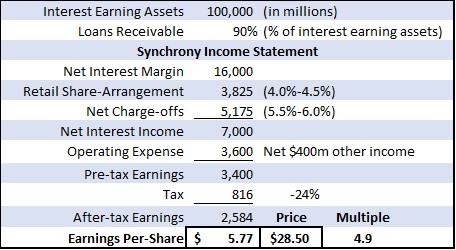

$SYF Quick pitch: bank that trades at 1.25x tangible book, has de minimis deposit flight risk, & targets (earns) a 28% return on tangible equity. While perennially discounted in relation to business quality, SYF is now exceptionally cheap (less than 5x earnings).

English