Sabitlenmiş Tweet

This is a must watch video by Ray Dalio on the rise and fall of empires and where we probably are as a nation. It’s excellent!

youtu.be/xguam0TKMw8

YouTube

English

Hankinator 🇺🇲

12.5K posts

@HD7658

Engineer, trader, investor. Opinions only- not advice. There is no amount of success that can legitimize you to the ignorant.

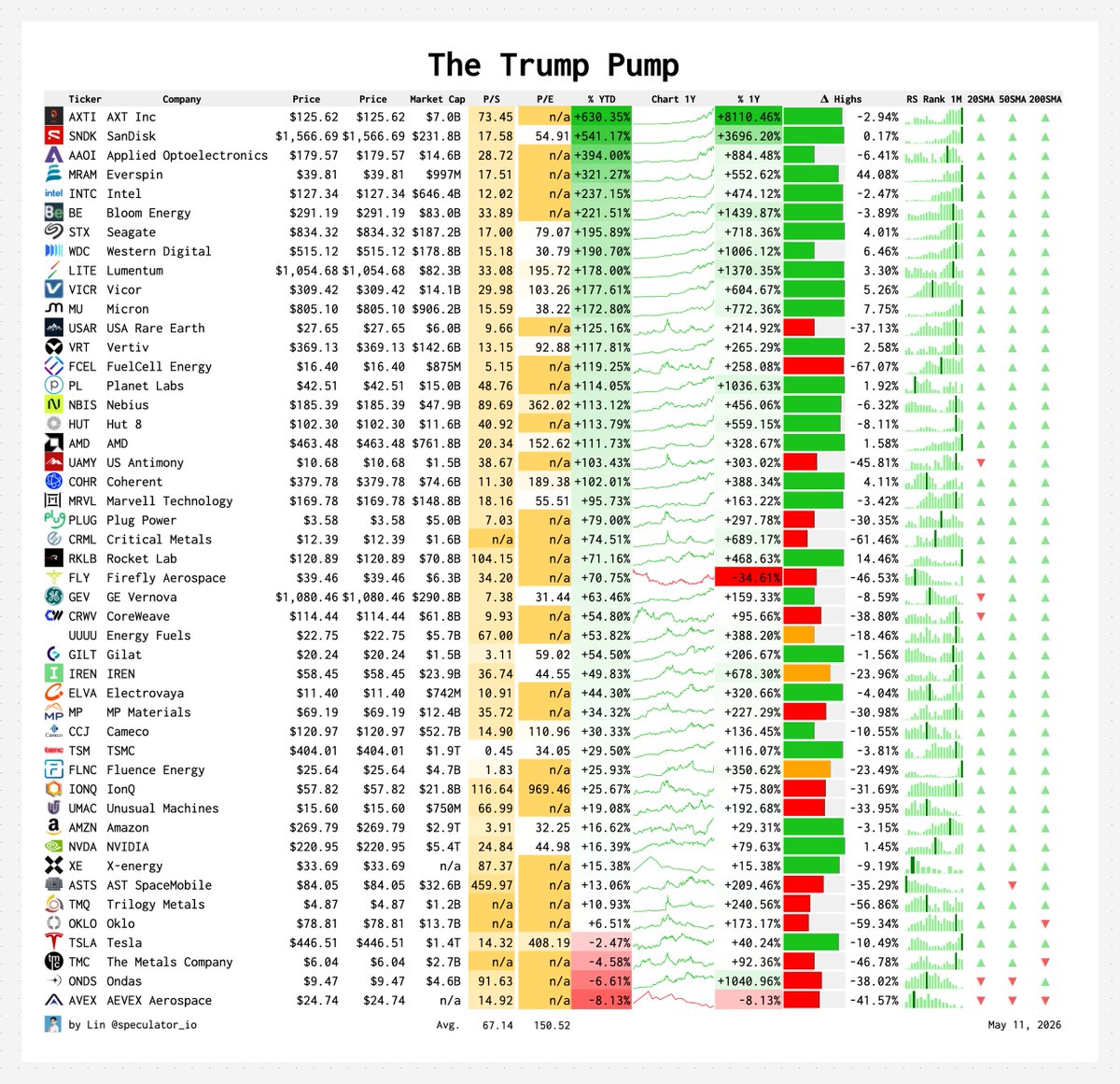

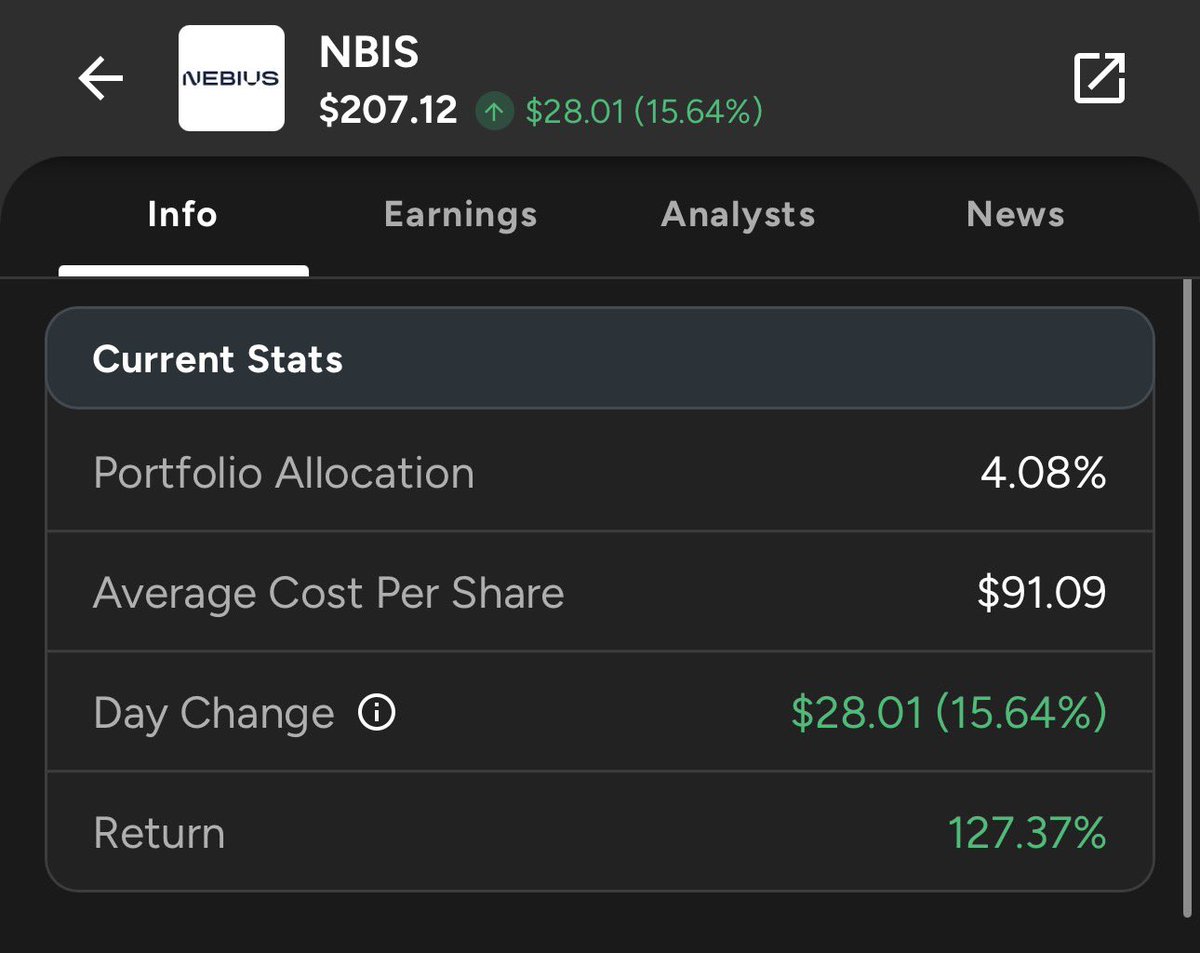

The neocloud category may be the most misunderstood corner of the AI trade because the market still treats these names as one uniform GPU-hours bet when they are actually very different business models: 1. $NBIS (Cloud Utility for the Agentic AI Age) $NVDA just chose Nebius as an architecture partner for the agentic AI era by co-designing AI factories with them, and the Rubin GPU access that comes with this partnership means Nebius gets the next-generation inference stack before almost anyone else in the market. At a $28B market cap, a 5GW power target and Nvidia’s engineering team embedded in the stack.. this is my favorite name in the neocloud category. 2. $IREN (Energy-to-Compute Engine of the AI Era) The dilution fear is real but the market is misreading it. IREN is not diluting to survive but diluting to scale into a $3.7B ARR target and the $9.3B in funding already secured through customer prepayments and GPU financing means the $6B ATM is optionality capital. The real bottleneck in AI infrastructure right now is power and IREN controls ~4.5GW of secured capacity while needing only ~500MW to support its ARR target by year-end. That 10x ratio of power capacity to near-term need is something no competitor can replicate quickly. 3. $CIFR (Landlord of the AI Utility Era) Cipher is not a pure neocloud but is a hyperscale infrastructure landlord signing decade-long leases to $AMZN AWS and $GOOGL while they fill the shells with compute. The AWS lease alone is expected to generate ~$700M in average annualized NOI for the next decade at nearly 100% NOI margins. Power-rich land is the scarcest resource in AI infrastructure and Cipher controls it with 600MW fully contracted, both facilities fully funded through non-recourse fixed-rate project debt and a 3.4GW development pipeline. 4. $CRWV (The Fragile Giant) CoreWeave’s demand backlog and revenue growth are very real but none of that matters if the capital markets close for even one quarter. Interest expense hit $388M in Q4 and management guided Q1 2026 interest expense to ~$550M which implies an annualized run rate above $2B before a single new data center comes online. The bull case requires capital markets to stay open, rates to cooperate, hyperscalers to honor take-or-pay contracts in full and construction to stay on time. That is a lot of dependencies in a macro environment where oil is approaching $100 and private credit is already showing signs of stress.