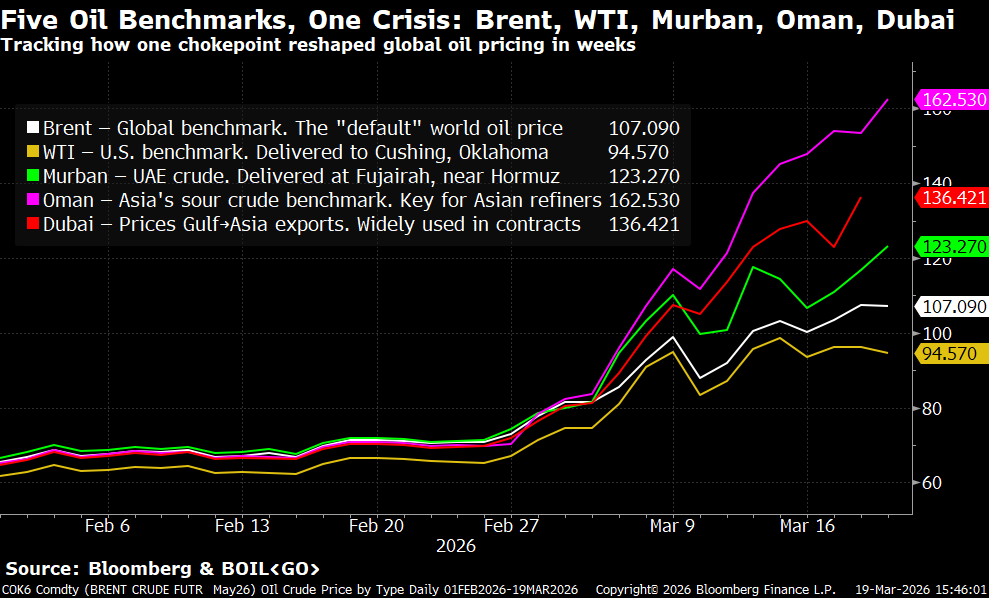

Michael McDonough@M_McDonough

🛢️There's a lot being said about oil prices right now, so I put this chart together to help explain the major crude benchmarks and why they're all behaving differently.

⚪Brent (white) — The world's "default" oil price. Most global trade is priced off this. When the news says "oil is at $108," they mean Brent.

🟡WTI (yellow) — The U.S. benchmark, based on crude delivered to Oklahoma. It's the lowest line on the chart because American oil doesn't need to transit the Strait of Hormuz.

🟢Murban (green) — Crude from Abu Dhabi, delivered at Fujairah port, which sits just outside the Strait. Even though it technically doesn't have to pass through the chokepoint, drone strikes have hit Fujairah and nearby ports, pushing insurance and shipping costs up.

🟣Oman (purple) — The key benchmark for heavier crude sold into Asia. Many refineries in China, Japan, and South Korea are built specifically to process this grade. It's the highest line on the chart because Asian buyers are competing fiercely for a shrinking pool of cargoes.

🔴Dubai (red) — Used to price most long-term Gulf→Asia export contracts. It tracks alongside Oman as a measure of how hard Asian markets are being squeezed.

The story isn't any single price — it's the gap between them. In late February these five lines were within $6 of each other. Now the spread between WTI and Oman is over $50.

Since the U.S.-Israeli strikes on Iran began Feb 28, the Strait of Hormuz has effectively been closed. Daily transits have fallen from a historical average of ~138 ships to fewer than 5. The IEA has called it the largest disruption to global energy supply in history. Iran's IRGC has warned that not "a litre of oil" will pass for U.S. allies, while selectively allowing some Iranian, Indian, and Pakistani tankers through.

Saudi Arabia is rerouting oil to its Red Sea port at Yanbu, and the UAE is using a pipeline to Fujairah — but combined pipeline capacity is only 3.5–5.5 million barrels/day vs the 20 million that normally flows through the Strait. Meanwhile, the 400 million barrel emergency reserve release by IEA members covers roughly 4 days of global consumption.

Japan's refiners get ~95% of their crude from the Gulf. China receives 45% of its oil via Hormuz. South Korea, India, Thailand, Pakistan, and Bangladesh are all severely exposed. The wider the spread between the Asian benchmarks and Western ones on this chart, the more you're seeing that pain in real time.